Part A — Summary

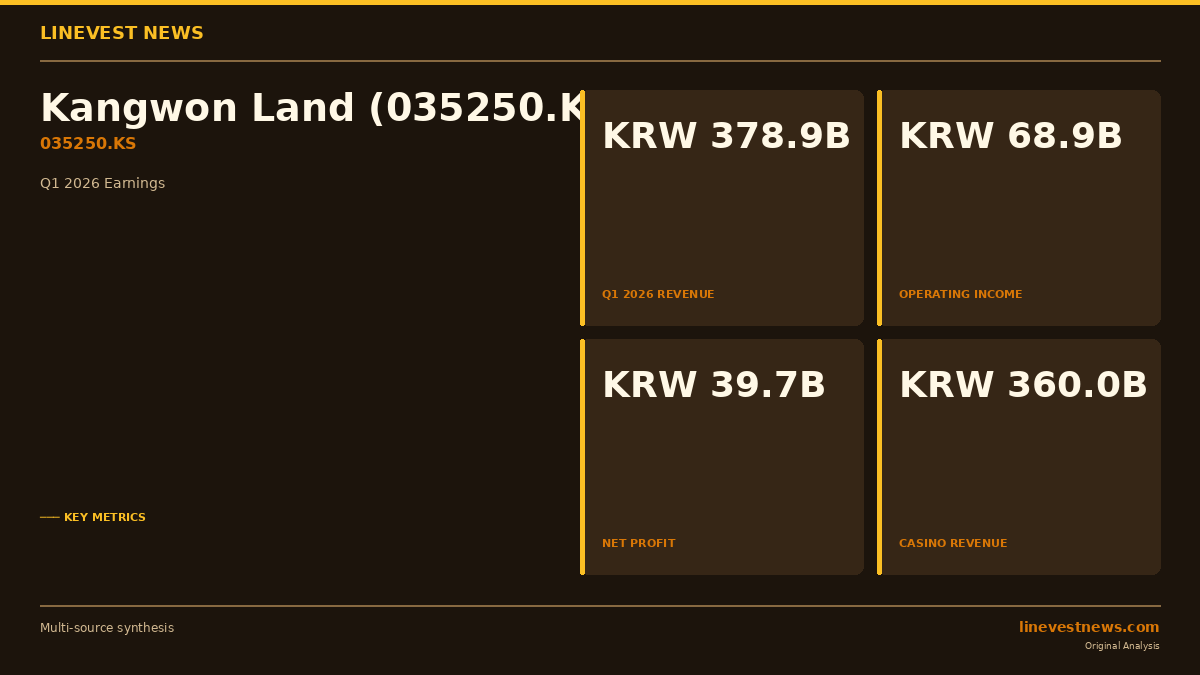

Kangwon Land (035250.KS), South Korea's only casino open to domestic visitors, reported first-quarter 2026 revenue of KRW 378.9 billion (approximately USD 274 million), a 3.4% year-over-year increase driven by steady growth in casino gaming volumes. However, operating income slipped 7.2% to KRW 68.9 billion and net profit collapsed 46.8% to KRW 39.7 billion, squeezed by a double blow of sharply higher selling, general and administrative expenses and a steep drop in financial investment income.

The results highlight the challenge facing the state-backed resort operator: while its monopoly casino business continues to grow, rising fixed costs and shrinking returns from its KRW 2.87 trillion investment portfolio are compressing bottom-line earnings at an accelerating pace.

Part B — Analysis

Casino Volume Holds Up; Costs Do Not

Casino gaming—which accounted for 89% of Kangwon Land's full-year 2025 revenue—continued to expand in Q1 2026. The company's regulatory gross casino revenue (the measure used to compute the statutory mining-area development fund contribution) rose 4.5% year-over-year to KRW 360.0 billion, compared with KRW 344.4 billion in Q1 2025. Total wagering volume from customers reached KRW 1,500.8 billion, up 3.2% from KRW 1,454.9 billion a year earlier, while total payouts to winners rose 2.7% to KRW 1,140.8 billion—implying a hold rate of roughly 24.0%, modestly improved from 23.7%.

Despite top-line momentum, gross profit was essentially flat at KRW 102.7 billion (margin: 27.1%) versus KRW 103.0 billion (28.1%) a year ago. The divergence between revenue growth and flat gross profit reflects higher cost of services, which climbed from KRW 263.3 billion to KRW 276.2 billion (+4.9% YoY)—outpacing revenue growth.

The bigger surprise was a 17.6% surge in SG&A expenses to KRW 33.8 billion from KRW 28.7 billion in Q1 2025, narrowing operating income to KRW 68.9 billion (operating margin: 18.2%) from KRW 74.3 billion (20.3%). The company did not provide a detailed breakdown of the SG&A increase in the report summary, but higher labour and administrative costs at its expanded Hi-One Resort complex are the probable drivers.

Financial Income Drag Turns Net Profit Negative Trend

The most significant earnings deterioration came from below the operating line. Financial income declined 30.4% to KRW 16.7 billion from KRW 24.0 billion in Q1 2025, reflecting lower interest returns on the company's enormous short-term investment portfolio. This portfolio—which encompasses mostly short-term financial instruments—totalled KRW 2,855.4 billion at 31 March 2026, down from KRW 3,009.2 billion at end-2025. While still a substantial liquidity buffer, declining yields on Korean money-market and fixed-income instruments weighed on non-operating income.

Pre-tax profit fell to KRW 53.9 billion from KRW 97.1 billion in Q1 2025, and after a KRW 13.7 billion tax charge, net profit attributable to shareholders came to KRW 39.7 billion—a 46.8% decline.

Balance Sheet: Low Leverage, Outsized Investment Reserves

Kangwon Land's balance sheet remains conservatively financed. Total assets stood at KRW 4,667.1 billion at quarter-end, with equity of KRW 3,781.3 billion supporting a modest debt-to-equity ratio. Current liabilities of KRW 813.3 billion include significant accruals for statutory levies—the company must pay 13% of annual casino revenue to the Closed Mine Region Development Fund, and 10% to the Tourism Promotion Development Fund, both payable the following year.

The company also maintains a KRW 224.97 billion legal dispute with Gangwon Province, which in 2020 retroactively assessed additional mining development fund contributions covering fiscal years 2014–2019. Following a partial win at the second court level in December 2023, the case is pending further appeal; the ultimate financial exposure remains uncertain.

Regulatory Monopoly Through 2045

Kangwon Land operates under a statutory exclusive licence granted by the Special Act on Support for Development of Closed Mining Areas (폐광지역법), which permits it to run the only casino in Korea accessible to domestic nationals. The legislation currently extends through 31 December 2045, providing a long-duration revenue floor. The company must, however, renew its casino operating permit from the Ministry of Culture, Sports and Tourism every three years.

The resort complex—operating under the Hi-One brand—encompasses a hotel (924 rooms, 18.9% market share in Gangwon Province's five-star segment), ski slopes, a golf course, a waterpark, and condominiums, in addition to the casino floor with 202 table games and 1,362 slot machines.

Outlook

Management has not issued formal quarterly earnings guidance. Analysts will watch whether the SG&A spike in Q1 persists through the year, and whether the ongoing rebalancing of the investment portfolio—visible in the reclassification of long-term financial assets to current assets during 2025—stabilises financial income. For the domestic casino operation itself, underlying volume trends appear resilient, but the regulatory cost structure (levies totalling roughly 27% of gross casino revenue, covering the development fund, tourism fund, excise tax and addiction-prevention levy) limits operating leverage.

Sources: DART Quarterly Report – Kangwon Land Q1 2026 · Korea Ministry of Culture, Sports and Tourism – Casino Industry Statistics · Kangwon Land 2026 Q1 Regulatory Filing (DART, 2026-05-15)