Hyundai Elevator Q1 2026: Revenue Falls 8.2% as Korea Construction Slump Deepens

Hyundai Elevator Co. (017800.KS), Korea's largest elevator manufacturer, posted weaker first-quarter results for 2026 as a domestic construction downturn continued to weigh on new-installation demand, while the company's recurring maintenance business provided a partial buffer.

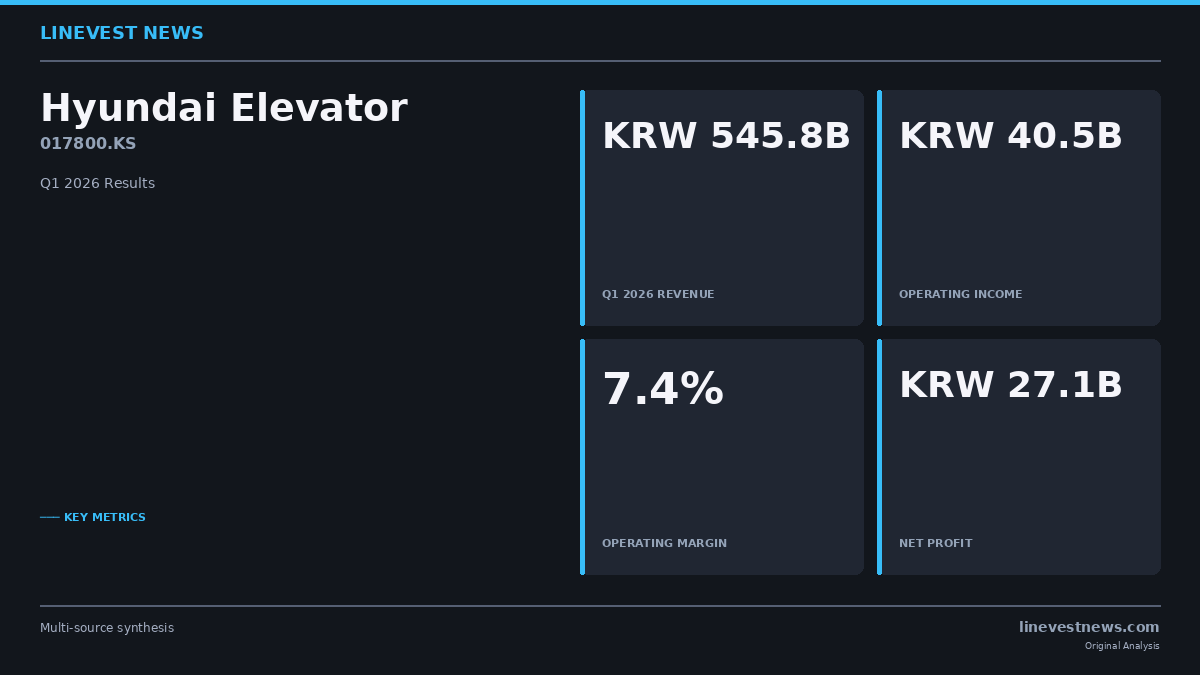

Q1 2026 Financial Highlights (Consolidated)

| Metric | Q1 2026 | Q1 2025 | YoY |

|---|---|---|---|

| Revenue | KRW 545.8B (USD ~393M) | KRW 594.4B | -8.2% |

| Gross Profit | KRW 134.4B | KRW 144.1B | -6.8% |

| Operating Income | KRW 40.5B | KRW 48.4B | -16.3% |

| Operating Margin | 7.4% | 8.1% | -70 bps |

| Net Income | KRW 27.1B | KRW 34.9B | -22.4% |

| EPS (Basic) | KRW 774 | — | — |

Revenue Mix: New Installation Under Pressure

On a standalone basis, Hyundai Elevator's Q1 2026 revenue breakdown reflects the pressure on its core elevator-manufacturing segment:

- Elevator manufacturing contributed KRW 264.7B, or 48.5% of consolidated segment revenue, as new unit sales tracked lower with fewer construction starts.

- Maintenance and repair services generated KRW 172.5B (31.6%), offering relative stability thanks to Korea's growing installed base of over 900,000 elevators nationwide.

- Logistics automation (Hyundai Movex), which includes automated warehouse systems and platform screen doors, added KRW 69.2B (12.7%), supporting the logistics and transit infrastructure sectors.

- Hotel, travel, and construction (Hyundai Asan, Abel Hyundai Hotels, Bloomvista) combined for approximately KRW 86.2B.

Korea's annual elevator installations fell sharply — 36,211 units in 2025 versus 48,884 in 2024, a decline of roughly 26% — reflecting a broad pullback in housing construction. As a downstream industry that lags construction cycles by one to two years, Hyundai Elevator expects continued near-term headwinds before conditions improve alongside a potential recovery in residential and commercial building activity.

Order Backlog Provides Revenue Visibility

Despite the top-line softness, the company maintained a robust order backlog as of March 31, 2026:

- Elevator and escalator segment: KRW 1.50T in unfulfilled orders

- Construction (Hyundai Asan): KRW 431.6B

- Logistics automation: KRW 308.8B

- Total backlog: KRW 2.24T

The backlog, which exceeds approximately four times the company's quarterly revenue run-rate, provides meaningful forward visibility, particularly as Hyundai Elevator positioned to capture demand from ongoing urban redevelopment projects (재개발·재건축) and expanding high-rise construction in Korea's major metropolitan areas.

Financial Position and Cash Generation

Hyundai Elevator maintained a strong liquidity position, with cash and cash equivalents of KRW 610.7B alongside KRW 226.1B in short-term financial instruments as of March 31, 2026, totaling approximately KRW 836.8B in near-liquid assets.

Financial income surged to KRW 11.5B in Q1 2026 (versus KRW 4.7B in Q1 2025), reflecting higher returns on deployed cash amid elevated interest rates. Financial costs also increased to KRW 19.4B (from KRW 15.3B), in part reflecting guarantees extended for overseas subsidiaries, including approximately KRW 48B in debt guarantees for Hyundai Elevator (China) Co., Ltd.

Innovation and Global Expansion

Hyundai Elevator became the world's first company to commercialize modular elevator installation for buildings of 20 or more stories with its ENOBLOC system, which allows up to 90% of components to be factory-pre-assembled before on-site connection. The technology reduces installation time by up to 80%, lowers on-site safety risks, and cuts construction costs — positioning the company favorably as labor safety regulations, including Korea's Serious Accidents Punishment Act, become more stringent.

On the global front, Hyundai Elevator (China) Co., Ltd. operates a smart factory in Shanghai capable of producing approximately 6,600 units annually (25 units/day on 59 working days in Q1). The company also has operations in Malaysia and is pursuing further expansion into North America and Europe with market-specific product lines.

Research and development expenditures reached KRW 10.9B in Q1 2026 (2.0% of revenue), covering advances in AI-based fault diagnostics, SiC-inverter drives, smart IoT building integration, and autonomous vehicle (AGV)-linked logistics automation.

ESG Recognition

In early 2026, Hyundai Elevator received inclusion in the S&P Global 2026 Sustainability Yearbook and earned an MSCI ESG Rating of 'A', the second-highest tier. The company also retained the top spot in the Korea Industrial Brand Power (K-BPI) elevator category for the 15th consecutive year, as ranked by the Korea Management Association Consulting.

Sources: Korea Financial Supervisory Service — DART Q1 2026 Filing (분기보고서) · Korea Elevator Safety Agency — Annual Installation Data