Why Apple looks more like an investment fund than a manufacturer

Quick Recap

In Part 2 we walked through current assets — everything that turns into cash within 12 months. Today we look at the other side: non-current assets, the things a company holds for the long haul.

Apple's non-current assets total $211.3B — more than half of the entire balance sheet. The interesting question: in a "factoryless manufacturer" like Apple, what fills that $211B? The answer is unexpected.

1. The Composition of Non-Current Assets

Recall the breakdown from Part 1:

| Item | FY2025 ($B) | Share |

|---|---|---|

| Marketable securities (long-term) | 77.7 | 37% |

| Property, plant and equipment, net | 49.8 | 24% |

| Other non-current assets | 83.7 | 40% |

| Total non-current assets | 211.3 | 100% |

Apple non-current assets, FY2025

Notice anything strange? The single largest line is "Marketable Securities" — i.e., invested funds, essentially a giant bond portfolio. "Property, Plant and Equipment" — what you'd expect to dominate a manufacturer's books — is only second-largest. Apple's asset structure looks more like that of a hedge fund than a hardware company.

2. Long-Term Marketable Securities ($77.7B) — Apple's Second Treasury

Long-term marketable securities are bonds and other investments with maturities greater than one year. They're the long-dated cousins of the $18.8B short-term securities we met in Part 2.

Where does Apple put its enormous operating cash? Half goes to share repurchases, and the rest sits in safe fixed-income securities. Add up the cash and securities: $35.9B + $18.8B + $77.7B = $132.4B in cash, equivalents, and marketable securities total. That's the figure Apple itself calls out in the 10-K's Liquidity discussion as its "available liquidity."

Practical takeaway

When analyzing any company, don't define "true cash position" using just the "Cash" line. Add cash equivalents and marketable securities to get the actual liquidity buffer. Then subtract interest-bearing debt to get "Net Cash" — the real measure of financial flexibility. (For Apple, after subtracting debt, net cash is roughly $32B — we'll get there in Part 4.)

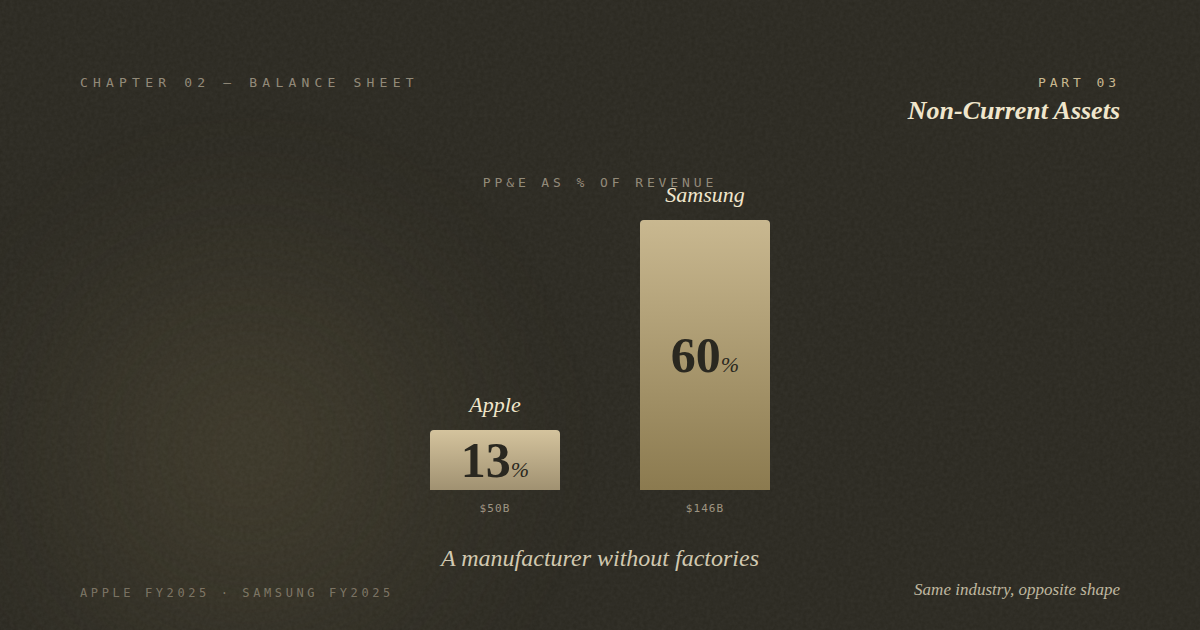

3. Property, Plant and Equipment ($49.8B) — Almost No Factories

Property, Plant and Equipment (PP&E) is the physical stuff a company owns: buildings, land, machinery, vehicles. Apple's 10-K Note 5 breaks PP&E down further:

| Category | FY2025 ($B) | FY2024 ($B) |

|---|---|---|

| Land and buildings | 27.3 | 24.7 |

| Machinery, equipment, and internal-use software | 83.4 | 80.2 |

| Leasehold improvements | 15.1 | 14.2 |

| Gross PP&E | 125.8 | 119.1 |

| Accumulated depreciation | (76.0) | (73.4) |

| Net PP&E | 49.8 | 45.7 |

Apple PP&E detail (FY2025, Note 5)

Two things this table tells us

First, the largest line is "Machinery, equipment, and internal-use software" at $83.4B. What is that? Apple's data centers, servers, chip-design equipment — and so on. Even though Apple outsources iPhone assembly, it runs its own cloud services (iCloud, Apple Music, Apple TV+) on Apple-owned infrastructure.

Second, accumulated depreciation is $76.0B — roughly 60% of historical cost. That means the asset base is, on average, well into its useful life. Not necessarily a concern, since data center and server gear refresh quickly, but worth noting.

4. Capital Expenditures (CapEx) — The Annual Reinvestment

CapEx is the total a company spends in a year acquiring new fixed assets. It's a cash flow statement number rather than a balance sheet line, but you can't fully read non-current assets without it. Apple's CapEx pattern looks like this:

| Fiscal Year | CapEx ($B) | Depreciation ($B) |

|---|---|---|

| FY2023 | 11.0 | 8.5 |

| FY2024 | 9.4 | 8.2 |

| FY2025 | 12.7 | 8.0 |

Apple CapEx vs. Depreciation (Source: 10-K Cash Flow Statement)

Recall from Chapter 1's bonus part: the CapEx vs. depreciation comparison reveals a company's growth phase.

- CapEx > Depreciation: company is expanding → this is Apple in FY2025 ($12.7B vs. $8.0B)

- CapEx ≈ Depreciation: maintaining current scale

- CapEx < Depreciation: contracting

Apple may not own iPhone factories, but it does invest steadily in data centers, Apple Park headquarters, AI chip design infrastructure, and similar facilities. The pace has accelerated as AI workloads demand more in-house compute capacity.

Apple's CapEx intensity vs. peers

CapEx as % of revenue:

- Apple FY2025: $12.7B / $391B = ~3.2%

- Samsung 2025: ~₩53T / ₩333T = ~16%

- TSMC 2024: ~$30B / $90B = ~33%

- Microsoft FY2024: ~$44B / $245B = ~18%

Apple has the lowest CapEx burden among the IT giants. Microsoft, Google, and Meta plow 15-20% of revenue back into data centers and AI infrastructure each year. Apple sits at 3%. That's the result of an outsourced production model and a device-centric (rather than cloud-centric) business.

The crucial implication

Low CapEx means high free cash flow. This is one of the structural reasons Apple can sustain its enormous buyback program. While Microsoft is sinking $44B annually into new data centers, Apple is using that money to buy back its own stock. Both are rational capital allocation choices — they just reflect very different philosophies.

5. Other Non-Current Assets ($83.7B) — A Diverse Bucket

The final big chunk, other non-current assets at $83.7B. "Other" is a deceptive label — there's a lot inside. Apple's Note 6 provides a partial breakdown:

| Component | FY2025 ($B) |

|---|---|

| Deferred tax assets | 20.8 |

| Other (goodwill, intangibles, lease assets, etc.) | 62.9 |

| Total other non-current assets | 83.7 |

Apple other non-current assets (Note 6)

① Deferred Tax Assets ($20.8B)

This is the deferred tax concept we met in Chapter 1, Part 4 — but now from the asset side. It represents the present value of future tax reductions the company is entitled to.

Companies with heavy R&D, like Apple, often have temporary differences between book and tax income. Those differences create future tax benefits, capitalized as deferred tax assets. Remember the principle: book income ≠ taxable income, and the gap creates an asset (or liability) on the balance sheet.

② Goodwill and Intangibles

Apple does small tuck-in acquisitions every year. The premium paid above net book value is recorded as goodwill. But unlike companies that grow through major M&A, Apple's goodwill stays small.

Goodwill can be a red flag. When acquired businesses fail to deliver expected value, goodwill must be written down — sometimes massively. In 2018, GE took a $23B goodwill impairment, sending the stock crashing. Apple's modest goodwill exposure means lower risk of such surprises. When analyzing acquisition-heavy companies, always watch the goodwill line.

③ Right-of-Use Assets

Apple Store rent is, you'd think, an expense. But under accounting rules adopted in 2019, the rights to lease physical retail and office space are capitalized as assets. Apple operates over 500 retail stores worldwide on leases — adding up to a substantial right-of-use asset balance.

6. What Apple's Non-Current Assets Reveal

Putting it all together, Apple's non-current asset structure tells us:

- The "factoryless manufacturer" claim is real — PP&E is just 13% of revenue

- Investment portfolio dwarfs PP&E — 37% of non-current assets are marketable securities

- Lowest CapEx intensity (3.2%) among IT giants — most capital-efficient

- $20.8B deferred tax assets — present value of future tax savings

- Small goodwill — limited M&A risk

In one sentence: Apple is a manufacturer that holds most of its capital in bonds rather than factories, makes small acquisitions, and reinvests modestly in physical assets. That's a very different shape from a typical "manufacturer."

Coming in Part 4

Now we cross to the other side of the balance sheet — liabilities. Part 4 takes on Apple's most famous paradox:

- Why does Apple, sitting on $132B in cash, carry $286B in liabilities?

- The maturity profile of Apple's $90B in term debt — how is it scheduled to be repaid?

- Accounts payable of $70B — is this really "debt"?

- Deferred revenue ($9B) — money already received, but a liability?

Frequently Asked Questions

What's the difference between marketable securities and cash equivalents?

Cash equivalents must mature in 90 days or less from purchase. Marketable securities have longer maturities. Both are liquid investments, but only cash equivalents combine with cash on the balance sheet's first line.

Why is Apple's CapEx so much lower than Microsoft's or Google's?

Apple's primary business is selling devices, with most manufacturing outsourced to contract manufacturers. Microsoft and Google generate huge revenue from cloud services that require massive owned data center investments. Apple's services business — while growing — is a smaller share of total revenue and uses Apple-owned infrastructure more selectively.

Is high goodwill always a bad sign?

Not always — but it warrants scrutiny. Goodwill represents the premium paid above book value in acquisitions. The risk: if acquired businesses underperform, goodwill must be impaired (written down), creating large non-cash losses. Companies like Apple, with modest acquisition activity, carry less of this risk than serial acquirers.

Why are deferred tax assets considered assets?

Because they represent legally recognized future tax benefits. When tax rules and accounting rules treat the same item differently (e.g., depreciating a piece of equipment over different timeframes), the resulting future tax savings are recognized today as an asset, valued at expected realization.

Next: Part 4 — Liabilities and the Cash-Rich Company's Debt Paradox.