Quick Recap

With assets covered, we cross to the right side of the balance sheet — liabilities. Things the company owes. And right away, Apple presents a puzzle:

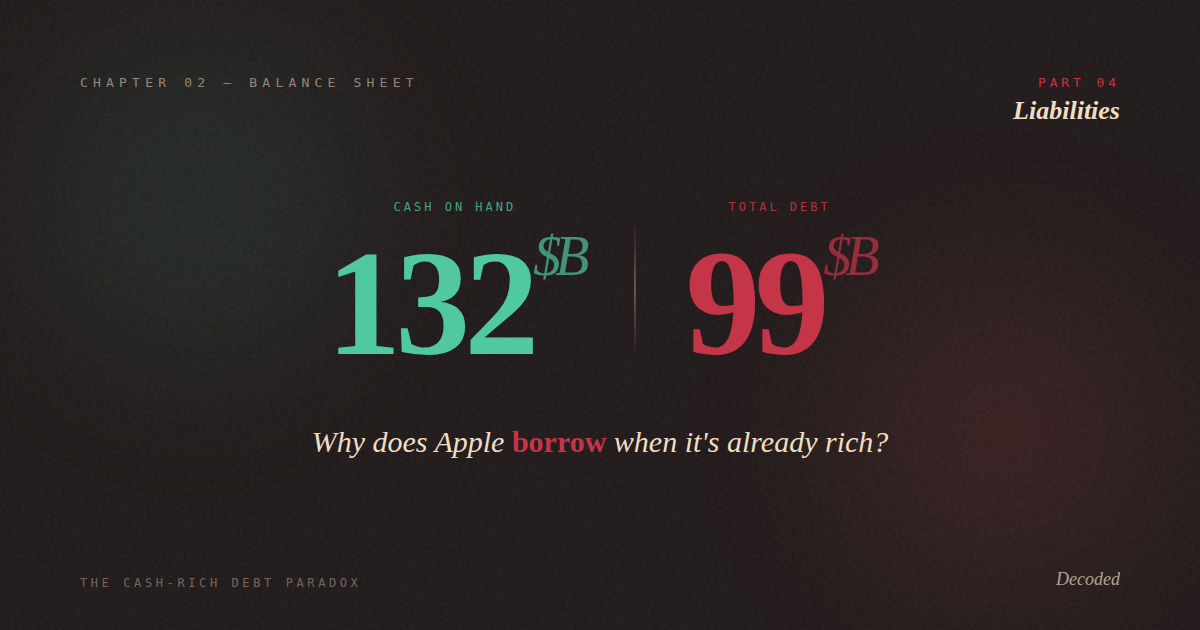

Apple holds $132B in cash, equivalents, and marketable securities, yet it has $285.5B in total liabilities. Debt more than double its cash. From a personal-finance perspective that's bizarre. "Why would someone with $1M in the bank deliberately borrow $2M?"

Today's mission: resolve the cash-rich debt paradox and decode what those $286B in liabilities really are.

1. Two Kinds of Liabilities — Operational vs Financial

Before dissecting Apple's liabilities, one critical distinction. Not all liabilities are "debt" in the financial sense.

Liabilities = Operational Liabilities + Financial Debt

Operational Liabilities: arise naturally from running the business. Accounts payable, accruals, deferred revenue. Don't bear interest.

Financial Debt: real "borrowed money." Bonds, loans, commercial paper. Bears interest.

Why does this matter? Operational liabilities aren't really "debt." When a company tells a supplier "we'll pay you in 60 days," that creates an account payable — but it's a normal part of operations, not a sign of financial stress.

Real "financial risk" comes from financial debt only. When people say "debt-to-equity ratio," they really should mean financial debt to equity, not all liabilities. Separating these two is the first step in any serious balance sheet analysis.

2. Apple's FY2025 Liabilities — Itemized

Apple's $285.5B in liabilities, broken out:

| Item | FY2025 ($B) | Type |

|---|---|---|

| Total current liabilities | 165.6 | |

| Accounts payable | 69.9 | Operational |

| Other current liabilities | 66.4 | Operational/Mixed |

| Deferred revenue | 9.1 | Operational |

| Commercial paper | 8.0 | Financial |

| Term debt (current) | 12.4 | Financial |

| Total non-current liabilities | 119.9 | |

| Term debt (long-term) | 78.3 | Financial |

| Other non-current liabilities | 41.5 | Mixed |

| Total liabilities | 285.5 |

Source: Apple 10-K FY2025

Separating financial from operational

If we split the liabilities by economic nature:

| Category | Amount ($B) |

|---|---|

| Financial Debt | |

| Commercial paper | 8.0 |

| Term debt (current) | 12.4 |

| Term debt (long-term) | 78.3 |

| Total financial debt | 98.7 |

| Operational liabilities (approx) | ~186 |

| Total liabilities | 285.5 |

Liabilities split by economic nature (approximate)

Apple's true "borrowed money" is about $99B — only one-third of total liabilities. The other $186B is the natural accumulation of running a global business — payables, accruals, deferred revenue, and so on.

3. Accounts Payable ($69.9B) — Suppliers Are Lending to Apple, Interest-Free

Apple's largest liability line is Accounts Payable at $69.9B. What is it?

Simply put: "components and services already received but not yet paid for." When Foxconn delivers iPhone components and Apple says "pay you in 60 days," the unsettled amount sits as accounts payable.

What "$70B in payables" really means

This is, economically, $70B that Apple's suppliers are lending Apple — interest-free. For 60 days, Apple gets to deploy capital that it would otherwise have to raise. To clear it all immediately would mean a $70B cash outflow.

Working-capital insight: Apple collects from customers fast + pays suppliers slowly + carries almost no inventory. That combination produces a famously "negative working-capital cycle" — operations themselves generate cash. It's a side effect of the outsourced manufacturing model and Apple's bargaining power.

Accounts payable is less "debt" than "interest-free credit Apple extracts from its suppliers." As long as the business runs normally, payables get paid down and immediately replenish — they roll forever. In effect, this is a permanent source of zero-cost financing.

4. Deferred Revenue ($9.1B) — Cash Received, Not Yet Earned

Deferred Revenue confuses a lot of first-time readers. "Money already collected, but not yet recognizable as revenue."

Example: you pay $99 for an annual Apple Music subscription. Apple collects the cash today. But it can only book $8.25 per month as revenue (1/12 of the year), not all $99 at once. The remaining "undelivered service" is a future obligation, and that's why it's a liability.

Growth in deferred revenue is often a positive signal — "future revenue is already locked in." It's one of the most important metrics in SaaS analysis. When this line grows quickly, it suggests stable, predictable revenue ahead.

Apple vs SaaS companies

Apple's $9.1B deferred revenue is about 2.3% of revenue — a small share. Why? Apple's business is still dominated by the "sell a device, recognize revenue immediately" model.

Microsoft, by contrast, has deferred revenue near 25% of revenue. The recurring subscription model dominates. The size of deferred revenue is one window into how far a company has shifted toward subscription economics.

5. Term Debt ($90.7B) — The Real Borrowed Money

Now to actual debt. Apple has issued $12.4B in current and $78.3B in long-term notes — about $90.7B in corporate bonds outstanding.

Why does Apple borrow at all?

This is where new readers get stuck. A company with $132B in cash chose to borrow $90B? Two main reasons:

① Avoiding repatriation taxes (historical)

Through the 2010s, the bulk of Apple's cash sat overseas (largely in Ireland). Bringing it back to the US triggered a 35% repatriation tax. Repatriating $100B meant losing $35B to taxes. Apple's calculation: borrowing fresh in US capital markets to fund buybacks was cheaper than paying repatriation tax to access the offshore cash. (The 2017 Tax Cuts and Jobs Act largely neutralized this incentive.)

② Capital structure optimization

How a company splits funding between debt and equity changes its Weighted Average Cost of Capital (WACC). Because interest is tax-deductible, debt is often cheaper than equity. A AA-rated company like Apple can issue bonds at 1–3% interest — much cheaper than its implicit cost of equity. So maintaining some debt is capital-efficient.

The takeaway: Apple's $90B in debt isn't "because they ran short of cash." It's deliberately held debt for tax efficiency and capital structure optimization. Like a wealthy person taking out a low-rate mortgage to free up capital for higher-return investments. That's the resolution to the "debt paradox."

Term debt maturity profile

Per Apple's 10-K Note 7, the term debt maturities span 2025 through 2062 — a wide ladder. Effective interest rates range from 0.03% to 5.75%. Bonds issued during the zero-rate era pay almost nothing; recent issuances run at 5%-plus. Apple has staggered the maturities to avoid concentration risk.

This is debt maturity management. $90B of debt due all at once next year would be dangerous. Spread across 30+ years, it's manageable.

6. Net Cash — Apple's True Financial Headroom

To see Apple's real financial position in one number, calculate Net Cash:

Net Cash = Cash & Equivalents − Financial Debt

Apple FY2025: $132.4B − $98.7B = ~$33.7B

Apple is a company that, after paying off every dollar of debt, would still have $33B left over. A few years ago, when buybacks were less aggressive, net cash was closer to $150B. Heavy share repurchases have brought the cushion down — but it's still solidly positive.

Net cash positive is a strong signal of financial soundness. Compare across industries:

| Company | Net Cash / (Net Debt) ($B) | Status |

|---|---|---|

| Apple | +$33.7 | Net cash |

| Microsoft | +~$50 | Net cash |

| Samsung Electronics | +~$60 (KRW equiv) | Net cash |

| Boeing (for context) | −$40+ | Net debt |

| AT&T (for context) | −$130+ | Net debt (high) |

Net cash / net debt comparison (approximate)

Tech giants like Apple, Microsoft, and Samsung tend to be net-cash companies. Capital-intensive industries (airlines, telecoms) typically run net debt. Different industries, different capital structures.

7. What We Found in Part 4

Key takeaways from this part:

- Liabilities ≠ debt — separate operational from financial obligations

- Apple's true debt is ~$99B — only about 35% of total liabilities is real borrowing

- Accounts payable of $70B is essentially interest-free supplier financing — Apple's negotiating power in numbers

- Deferred revenue of $9B reflects future earned revenue — much larger share for SaaS companies

- Apple borrows on purpose — for tax efficiency and optimal capital structure

- Net cash of +$33.7B — Apple's actual financial cushion

Coming in Part 5

The final part. Part 5: Equity and the Buyback Mystery unpacks:

- The composition of $73.7B in equity — common stock, retained earnings, AOCI

- "Accumulated deficit (-$14B)" — how is retained earnings negative? the most surprising line on Apple's balance sheet

- Apple's buyback pattern — $263B spent in three years repurchasing its own stock

- The EPS-boosting mechanism — how buybacks reward shareholders

The most fascinating story on Apple's balance sheet has been waiting for the end.

Frequently Asked Questions

Why is accounts payable considered a liability if no cash is leaving today?

Accounts payable represents an obligation to pay in the future for goods or services already received. Even though no cash leaves immediately, the company is legally bound to pay. By the matching principle of accounting, the obligation must be recognized when it's incurred, not just when paid.

How is deferred revenue different from accounts payable?

Deferred revenue is cash already received for services not yet delivered (the company owes service). Accounts payable is goods or services already received but not yet paid for (the company owes money). Both are liabilities but represent opposite sides of an exchange.

What's the optimal debt-to-equity ratio for a tech company?

It depends on cash flow stability. Mature tech companies like Apple, Microsoft, and Google can carry significant debt because their cash flows are reliable. Newer or unprofitable tech companies should generally avoid debt — they may need their cash for operations. Industry norms range widely.

Why does Apple disclose effective interest rates from 0.03% to 5.75%?

Apple has issued bonds across many years, each at the prevailing market rates of that time. Bonds issued during the 2020-2021 ultra-low-rate era pay near 0%. Recent issuances reflect higher current rates. The wide range simply reflects the historical capital-raising calendar.

Next: Part 5 — Equity and the Buyback Mystery: How Apple's Retained Earnings Went Negative.