SK Bioscience Q1 2026: CDMO Revenue Surges 75.8% of Mix as IDT Biologika Ramps Up, But R&D Spending Drives Deeper Operating Loss

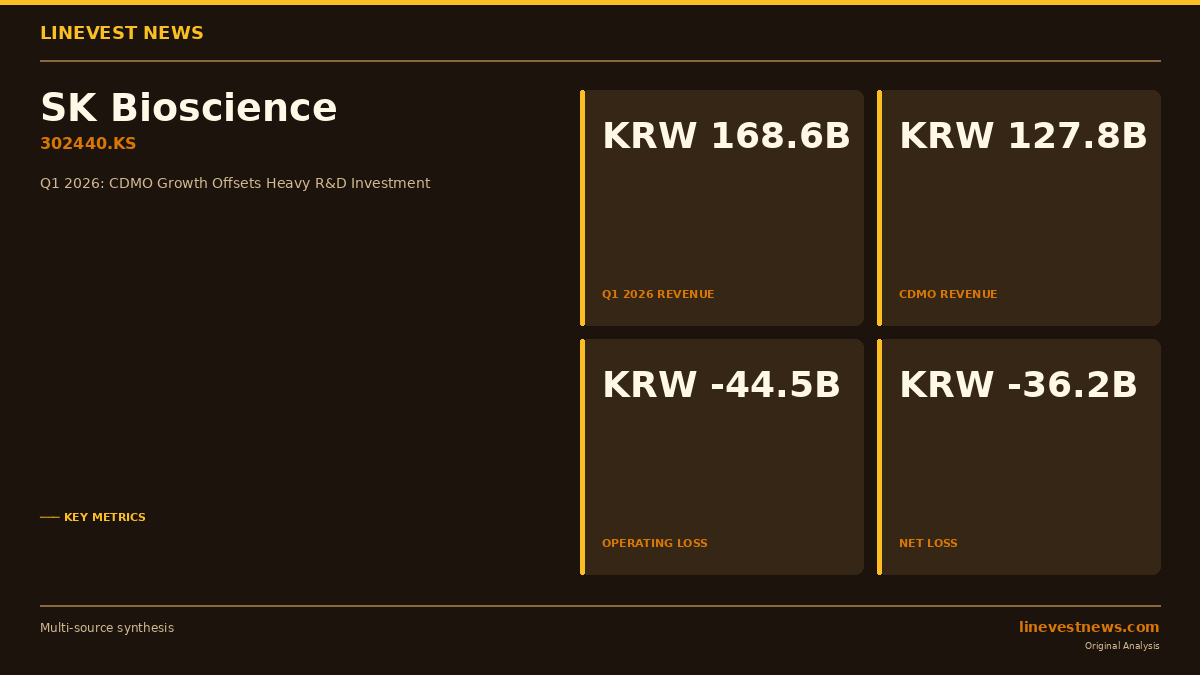

SK Bioscience Co., Ltd. (302440.KS) reported first-quarter 2026 consolidated revenue of KRW 168.6 billion (approximately USD 122 million), a 9.1% increase year-over-year from KRW 154.6 billion in Q1 2025, as its German subsidiary IDT Biologika continued to drive contract development and manufacturing (CDMO) growth. However, a sharp increase in research and development spending pushed the quarterly operating loss to KRW 44.5 billion, more than tripling the KRW 15.1 billion operating loss posted in the year-ago period.

Revenue Breakdown: CDMO Dominates

The company's CDMO segment — anchored by IDT Biologika, acquired in mid-2024 — generated KRW 127.8 billion in Q1 2026, accounting for 75.8% of total consolidated revenue. The Vaccine Development & Commercialization segment contributed the remaining 24.2% (KRW 40.8 billion), comprising KRW 20.8 billion in proprietary vaccine products (SKYCellflu, SKYZoster, and others), KRW 17.0 billion in distributed products (Beyfortus RSV antibody, Hexaxim combination vaccine), and KRW 3.0 billion in service revenue.

Geographically, overseas revenue accounted for 81.8% of total sales at KRW 137.9 billion, reflecting the CDMO business's inherently global client base. Domestic revenue stood at KRW 30.7 billion (18.2%).

The order backlog at March 31, 2026 totaled KRW 827.9 billion, providing meaningful revenue visibility: CDMO orders represented KRW 715.8 billion (converted at EUR/KRW 1,733.37) through contracts extending to 2029, while vaccine supply orders added KRW 112.1 billion through 2033.

Operating Loss Widens Amid R&D Surge

Despite the revenue increase, profitability deteriorated significantly. Gross profit fell to KRW 14.9 billion in Q1 2026 from KRW 26.1 billion in Q1 2025, as cost of goods sold rose to KRW 153.8 billion from KRW 128.4 billion — reflecting higher IDT Biologika production costs as utilization rates climbed. The gross margin contracted to 8.8% from 16.9%.

Selling, general and administrative expenses — which include a significant portion of research and development costs — surged to KRW 59.4 billion from KRW 41.3 billion, driven by expanded clinical trial activity. Total gross R&D expenditure in Q1 2026 reached KRW 59.6 billion (35.4% of revenue), though after deducting government and external support grants of KRW 8.8 billion, net R&D spending was KRW 50.8 billion.

Key ongoing R&D programs fueling this spend include:

- GBP410 (21-valent pneumococcal vaccine, Phase 3): Co-developed with Sanofi, global Phase 3 trial launched December 2024 across the U.S., Europe, and South Korea; targets the pediatric pneumococcal market projected to reach KRW 13 trillion globally by 2030. Total milestone potential: USD 45 million + EUR 350 million.

- GBP560 (Japanese encephalitis mRNA vaccine, Phase 1/2): Co-developed with CEPI (USD 140 million total program budget).

- GBP610 (RSV prevention antibody, Phase 1): Licensed in from Gates Medical Research Institute (USD 16.25 million) in February 2026, with Phase 1b clinical trial material production completed.

- Microneedle patch influenza vaccine (preclinical): New contract with HaDEA (European Health and Digital Executive Agency), EUR 12.9M through IDT Biologika, signed February 2026.

The operating loss of KRW 44.5 billion and net loss of KRW 36.2 billion (KRW -425 per share) compare to Q1 2025's operating loss of KRW 15.1 billion and net loss of KRW 4.1 billion. The Q1 2026 standalone (non-consolidated) entity — SK Bioscience Korea without IDT Biologika — posted revenue of KRW 40.8 billion and operating loss of KRW 35.8 billion.

IDT Biologika Ramping: Utilization Hits 59.4%

A key operational positive: IDT Biologika's production utilization rate improved to 59.4% in Q1 2026 (19 of 32 available batches) from 47.6% in full-year 2025 (70 of 147 batches) and 34.0% in FY2024. The Andong L HOUSE facility in South Korea ran at 37.4% capacity (64 of 171 batches), slightly above the 35.0% rate seen in FY2025.

Balance Sheet: War Chest Intact

Despite consecutive quarterly losses, SK Bioscience maintains a robust balance sheet. Total assets stood at KRW 2,991.9 billion as of March 31, 2026, with equity of KRW 2,023.6 billion. Liquid financial assets — including KRW 86.7 billion in cash and equivalents, KRW 803.4 billion in short-term financial instruments, and KRW 207.6 billion in long-term financial instruments — total approximately KRW 1.1 trillion (USD 797 million), providing ample runway for its R&D pipeline.

Long-term borrowings (primarily for the IDT Biologika acquisition) stood at KRW 534.2 billion.

Domestic Market Position

In South Korea, SK Bioscience held a 22% share of the influenza vaccine market in 2025 (down from 23% in 2024), a 42% share of the shingles vaccine market (up from 35%), and a 34% share of the varicella (chickenpox) vaccine market (down from 52%), based on IMS data and proprietary estimates. The shingles vaccine market share gain reflects the premium market growth of SKYZoster.

Part B: Analyst Commentary

What the numbers reveal: SK Bioscience is in a deliberate investment phase — trading near-term profitability for long-term competitive positioning. The 9.1% revenue growth on the back of IDT Biologika CDMO ramp-up is constructive, but the gross margin compression to 8.8% signals that CDMO scale economics have not yet offset high fixed production costs. The operating loss tripling to KRW 44.5 billion demands scrutiny.

The margin story: The gross margin squeeze reflects two dynamics: (1) IDT Biologika carries a higher cost structure per batch at current utilization rates, and (2) the company's vaccine commercialization segment is in a seasonal trough — flu vaccine revenue typically peaks in Q3/Q4. Margins are expected to improve as CDMO utilization continues to rise toward breakeven capacity (estimated at ~65–70% utilization).

Pipeline optionality: The GBP410 pneumococcal vaccine Phase 3 with Sanofi represents the highest-conviction catalyst. If Phase 3 reads out positively (likely 2027–2028), entry into the KRW 13 trillion pediatric pneumococcal market would fundamentally re-rate the vaccine segment. The RSV antibody (GBP610) license-in adds a near-term revenue stream with commercial precedent (Beyfortus has already been distributed domestically since 2025).

Liquidity is not the concern: The KRW 1.1 trillion in financial assets provides a 3–4 year operating runway even at the current quarterly burn rate, reassuring investors that pipeline development will not be constrained by capital.

Key risk: Continued operating losses through 2026–2027 while clinical data matures, with IDT Biologika's EBITDA contribution at risk if pharma customers delay CDMO contract starts amid macro uncertainty.

Sources: DART OpenDART (분기보고서, 2026.05.13, SK바이오사이언스 rcept_no 20260513000618) · Evaluate Pharma, Global Vaccine Market 2025 · Korea Bioindustry Association CDMO Report 2025

"