Kolon Industries (KRX: 120110) is in talks to sell its printed-circuit-board (PCB) epoxy-resin and OLED display-coating businesses as fourth-generation heir Vice Chairman Lee Kyu-ho accelerates a broad restructuring of the Kolon Group's portfolio, according to people familiar with the matter. The process draws domestic and overseas private-equity interest and weighs raising fresh capital against retaining assets that continue to generate stable profit.

Samjong KPMG, the sale adviser, received letters of intent ahead of a preliminary-bidding deadline that closed the week of June 22. Skylake Equity Partners, a Seoul-based private-equity manager, confirmed its interest by submitting an LOI; several other domestic and overseas funds are also reviewing bids. No preferred bidder has been named, and the deal structure and price remain open — terms could still be revised or the process shelved if offers fall short of Kolon's expectations.

What's On the Block

The PCB materials unit produces specialty epoxy resins that go into copper clad laminate (CCL), the multi-layered substrate at the core of printed circuit boards. Kolon's display-coating arm supplies overcoat films used for the planarization and pixel-protection layers of OLED panels — end markets that include Samsung Display and LG Display customers.

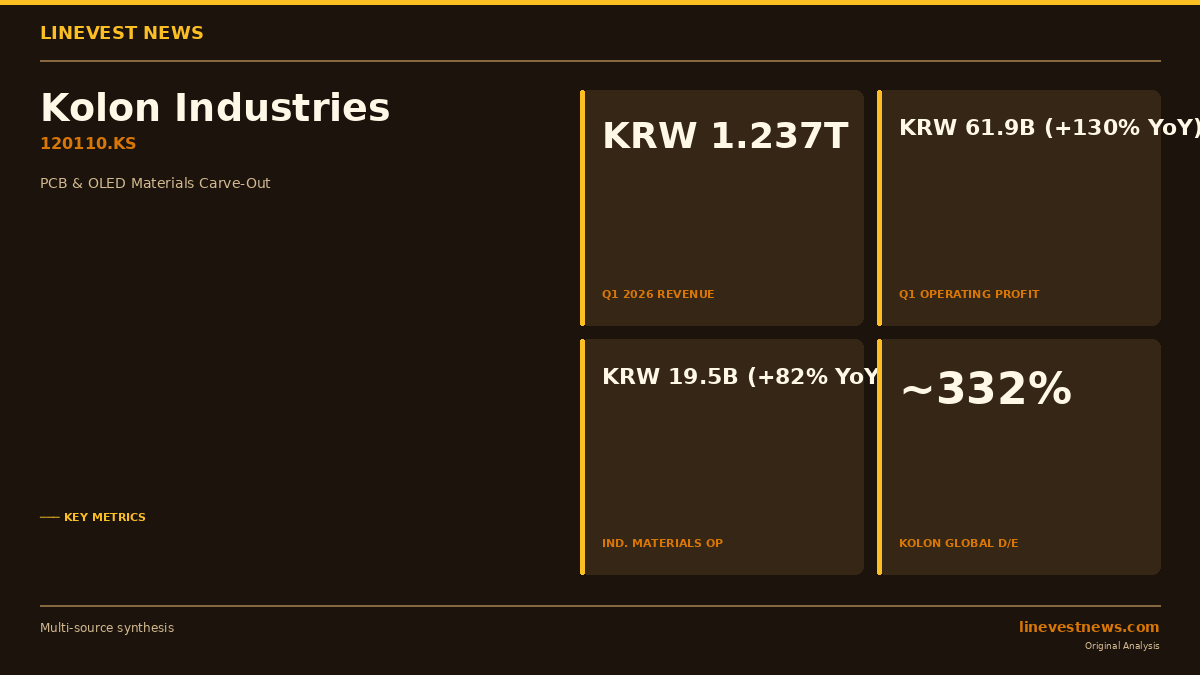

Both divisions carry stable earnings, industry analysts note, but Kolon Group has earmarked them for divestiture to unlock capital for segments with higher long-term growth and margin potential. Kolon Industries posted consolidated first-quarter 2026 revenue of KRW 1.237 trillion (+0.5% year on year) and operating profit of KRW 61.9 billion (+130% YoY). The industrial-materials segment — which houses the sale targets — contributed KRW 595 billion in revenue and KRW 19.5 billion in operating profit for the quarter, with operating income up 82% from a year earlier.

The AI Chip Material Kolon Is Keeping

Absent from the carve-out is Kolon's modified polyphenylene oxide (mPPO) business, which management has deliberately excluded from the sale perimeter. Industry sources describe mPPO — a high-performance polymer whose low dielectric loss suits AI server circuit boards — as one of Kolon's fastest-growing product lines. As AI-driven data-centre construction accelerates globally, demand for low-loss PCB dielectrics such as mPPO is expected to expand well into the decade.

By retaining mPPO and shedding the more commoditised CCL resin and OLED coating lines, Kolon Industries is aiming to sharpen its exposure to AI-adjacent, higher-multiple end markets while using the divestiture proceeds to fortify the group's balance sheet, materials sector analysts said.

Balance-Sheet Rationale

The asset sales sit inside a wider deleveraging push. Kolon Global — the Kolon Group entity that carries most of the conglomerate's construction and real-estate exposure — carried a debt-to-equity ratio of roughly 332% at the end of 2025, well above the 200% level that Korean credit analysts typically flag as a stress threshold. In parallel, the group is marketing several real-estate properties — including the Cappuccino Hotel in Gangnam, an HR development centre, and the Woojung Hills Country Club — with aggregate proceeds expected to reach approximately KRW 300 billion.

Vice Chairman Lee, who has taken inside-director seats across Kolon Corp., Kolon Global and Kolon Industries as part of a fourth-generation leadership consolidation, has signalled that capital freed by these disposals will be redirected toward bio-materials, hydrogen, and secondary-battery value-chain businesses — sectors where margins and growth visibility are substantially higher than in mature specialty chemicals.

Market Context

Korea's specialty-materials landscape is unusually active in mid-2026. The Kolon carve-out lands as IMM Private Equity closes its KRW 1.1 trillion acquisition of biosurgical-materials maker CGBio, and as battery-material producers accelerate portfolio moves of their own. Private-equity appetite for niche Korean industrial suppliers remains at a multi-year high, supported by the spread between conglomerate holding-company valuations and stand-alone asset prices for well-run mid-market businesses.

Kolon Industries (120110.KS) trades on the Korea Exchange.

Sources: Seoul Economic Daily – Skylake Joins Bidding for Kolon Industries' Materials Unit · Seoul Economic Daily – Kolon to Sell Display Coating and Semiconductor Substrate Businesses · Seoul Economic Daily – Kolon Industries Q1 Operating Profit Jumps 130%

"