LG Innotek Co., Ltd. (011070.KS) is set to deliver its best second quarter in four years as surging demand for AI chip substrates has reshaped the company's earnings trajectory — and Korea's second-largest brokerage now sees the outperformance extending well into the decade.

Q2 Operating Profit Set to Rise 18-Fold Year-Over-Year

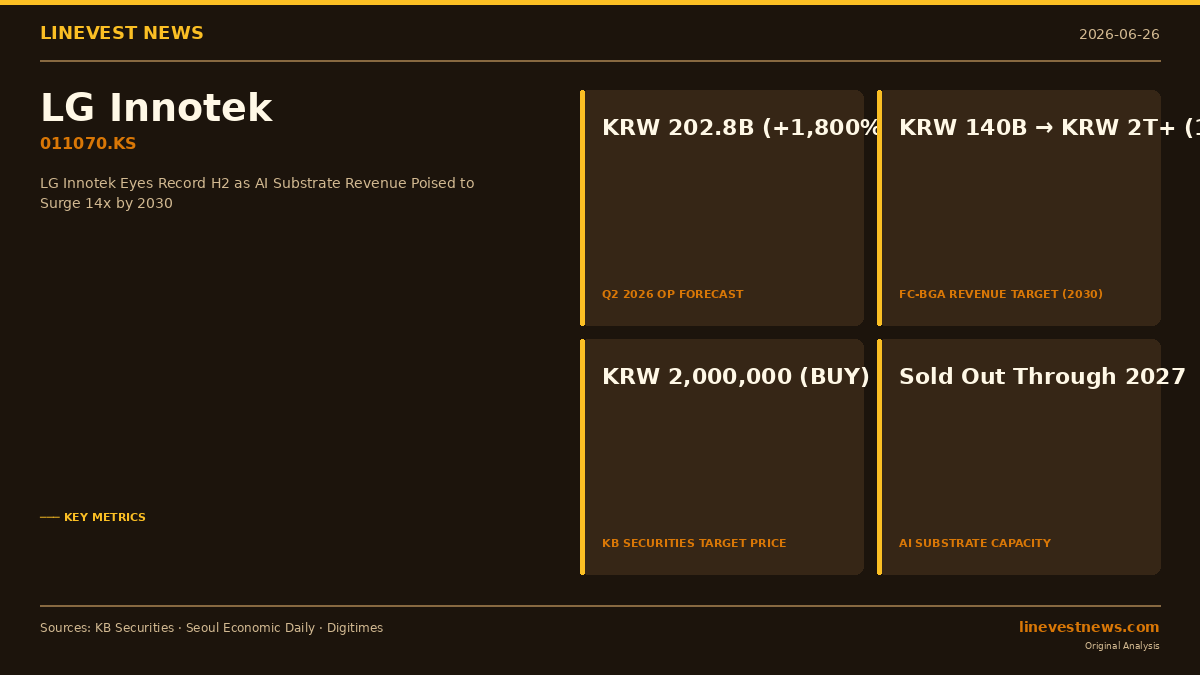

KB Securities raised its full-year 2026 operating profit estimate for LG Innotek to KRW 1.305 trillion, a 4.9% upward revision, and maintained a BUY rating with a target price of KRW 2 million — implying roughly 70% upside from the KRW 1.173 million level recorded on the day of the report.

For the second quarter of 2026 alone, KB Securities projects operating profit of KRW 202.8 billion (approximately USD 148 million), roughly 18 times the year-earlier figure and 39% above Bloomberg consensus of KRW 146 billion. That quarterly figure would mark only the second time in 15 years that LG Innotek has surpassed the KRW 200 billion threshold in a single second quarter, the prior instance being in 2022 — when the iPhone supercycle was at its peak.

Analyst Chang-min Lee of KB Securities characterized the Q2 outperformance as "not a mere one-off improvement, but a meaningful signal of earnings recovery for the first time in four years," pointing to a structural shift in the company's revenue mix toward AI-driven components.

FC-BGA Substrate: 14x Revenue Growth Targeted by 2030

At the center of the investment thesis is LG Innotek's FC-BGA (Flip-Chip Ball Grid Array) substrate business, which provides the high-density interconnect packages used in AI accelerator chips. KB Securities forecasts FC-BGA revenue to climb from approximately KRW 140 billion in 2026 to over KRW 2 trillion by 2030 — a more than 14-fold increase in four years.

LG Innotek's entire AI substrate allocation is expected to sell out completely in both 2026 and 2027, with supply shortages projected to persist through at least 2028. The tightness is drawing structural commitments from hyperscale cloud clients and chipmakers, who are now offering capital expenditure support and long-term supply contracts to secure priority access.

Digitimes reported in May 2026 that these supply terms "increasingly resemble long-term agreements used in the memory-chip sector," a reference to the multi-year take-or-pay contracts that characterize DRAM and NAND procurement. Customers include Intel and major U.S. cloud platform operators building out inference infrastructure.

Revenue Diversification Beyond Smartphones

The company is simultaneously managing a revenue transition: optical solutions (primarily camera modules for a major North American smartphone client) and package solutions together account for roughly 90% of total revenue. The package solutions segment — home to AI substrates — is set to take a growing share as FC-BGA capacity scales.

LG Innotek is targeting total package solutions segment revenue of KRW 3 trillion by 2030, and the sustained demand signals from hyperscale clients suggest that target is increasingly regarded as a floor rather than a ceiling.

Multi-Year Earnings Ramp

Beyond 2026, KB Securities forecasts operating profit of KRW 336.2 billion in 2027 (+80% year-over-year) and KRW 547.4 billion in 2028 (+45%), as newly committed substrate capacity comes fully online and AI server buildout continues to accelerate.

LG Innotek shares rose 13.22% on the day of the report, reflecting a reassessment of the company's positioning in the global AI hardware supply chain. The stock has been among the strongest performers on the KOSPI in 2026, supported by recurring analyst upgrades as consensus estimates have repeatedly lagged the pace of AI-driven demand.

Sources: KB Securities research report (June 2026), Seoul Economic Daily, Digitimes