Seoul Locks in Utility Rate Freeze for Second Half as Inflation Concerns Trump Energy Company Relief

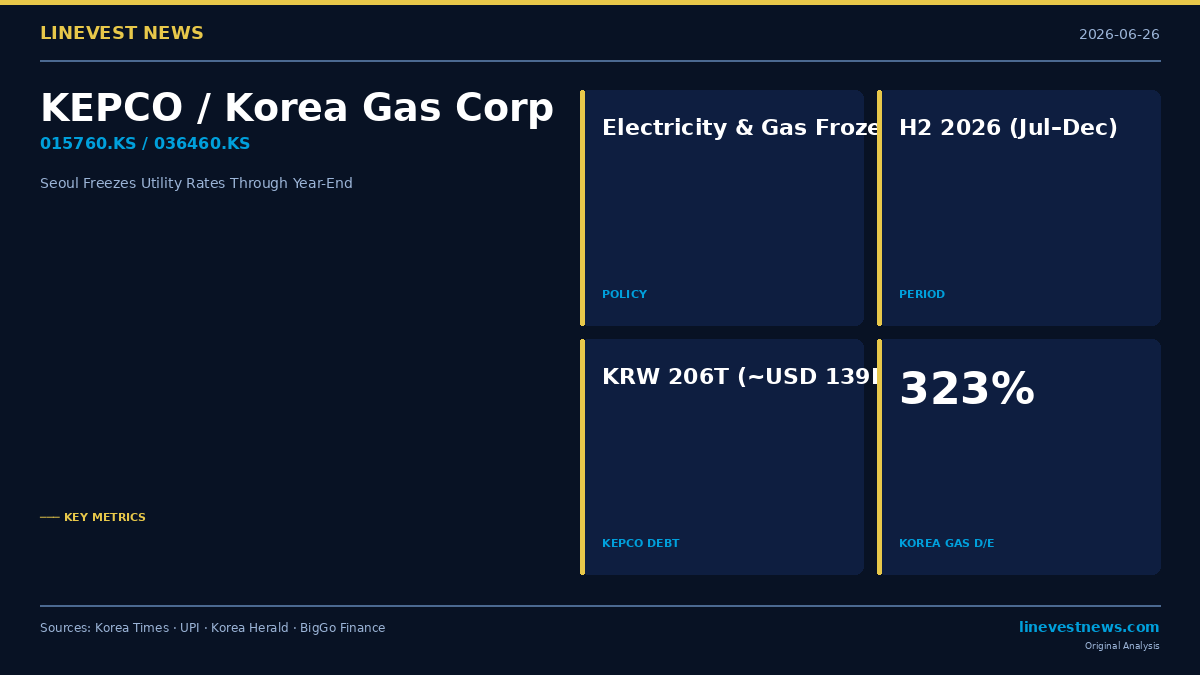

South Korea's government announced on June 26 that it will freeze electricity and gas rates through the end of 2026, extending a policy that has effectively blocked KEPCO (Korea Electric Power Corporation, 015760.KS) and Korea Gas Corporation (Kogas, 036460.KS) from passing rising costs on to consumers.

Finance Minister Koo Yun-cheol made the announcement during a government economic policy meeting, stating the administration will "freeze prices of major utilities, such as electricity and gas" while simultaneously lowering the fuel price cap introduced in mid-March. The government aims to keep consumer price inflation at around 3% in the second half of the year.

Part A: A Year-Long Squeeze on State-Run Utilities

Freeze That Never Thaws

KEPCO has now been operating under consecutive rate freezes through Q1, Q2, and into H2 2026. The adjusted fuel cost surcharge — capped at the maximum permissible KRW 5/kWh — remains unchanged for Q3. For investors, the pattern is consistent: the government treats electricity tariffs as an inflation management tool, not a cost-recovery mechanism.

The utility giant carries KRW 206.2 trillion (approximately USD 139.2 billion) in accumulated debt, a hole that deepened after the 2021-2023 global energy price surge forced the company to sell power below cost. With rates frozen again, that gap shows no near-term path to closure.

Bank of America has downgraded KEPCO to Neutral from Buy, citing limited near-term retail tariff adjustments and narrowed guidance for 2026 dividends. Management's cautious tone on upcoming Q3 government tariff negotiations disappointed analysts expecting a recovery signal.

Korea Gas Under Similar Pressure

Korea Gas Corporation (Kogas), the country's state-owned LNG importer and distributor, faces parallel stress. Kogas holds KRW 36.65 trillion in total debt, with a debt-to-equity ratio of 323%. Its trailing-12-month net profit margin stands at just 1% on revenue of KRW 34.8 trillion — margins that provide almost no buffer if LNG procurement costs rise.

City gas rates, which track LNG import prices, have been held below cost-recovery levels by government directive. With Middle East supply disruptions still a concern — the US-Iran memorandum of understanding has "gradually eased" external risks, per Minister Koo — Kogas faces the same bind: the government prefers a thin margin over any inflationary signal from a rate hike.

Part B: Policy Logic vs. Market Logic

Phased Adjustment — or Permanent Deferral?

Minister Koo framed the announcement as a phased unwinding: "The government will adjust the emergency measures currently in place in phases." But investors have heard this language before — from Q1 through Q2, each quarter's freeze was framed as temporary.

The fuel price cap, introduced in mid-March 2026 after Middle East-driven crude price spikes, will be lowered to reflect declining global crude oil benchmarks. This move benefits consumers at the pump, but does not resolve KEPCO or Kogas's accumulated cost deficits.

The government is also rolling out discount programs for agricultural and fishery products in July-August, alongside expanded imports of eggs and mackerel — a broad price stabilization package targeting the 3% inflation ceiling.

What It Means for Investors

For KEPCO (015760.KS) and Korea Gas (036460.KS), the rate freeze extends the timeline for any earnings recovery. Both companies operate as quasi-regulated utilities where political cycles effectively set pricing. With inflation still a priority and no election-driven political shift in sight, the earliest plausible window for rate normalization remains 2027 at best.

KEPCO's KRW 206T debt overhang means any further rate-freeze extension beyond H2 2026 would push the company closer to a potential government bailout or equity raise scenario — a tail risk not yet priced into the stock. Kogas's 323% debt-to-equity ratio leaves it similarly vulnerable to an LNG price spike or extended rate suppression.

Sector context: South Korea's KOSPI has rallied sharply this year on semiconductor momentum, but the energy and utility sector has lagged, with both KEPCO and Kogas trading well below book value. For yield-focused investors, the H2 dividend guidance reduction flagged by Bank of America adds another headwind.

Sources: Korea Times (June 26, 2026), Prokerala, UPI, BigGo Finance, Korea Herald, Bank of America.