Hyosung Corp Posts 15.6% Operating Profit Jump in Q1 2026 as IT and Pump Units Surge

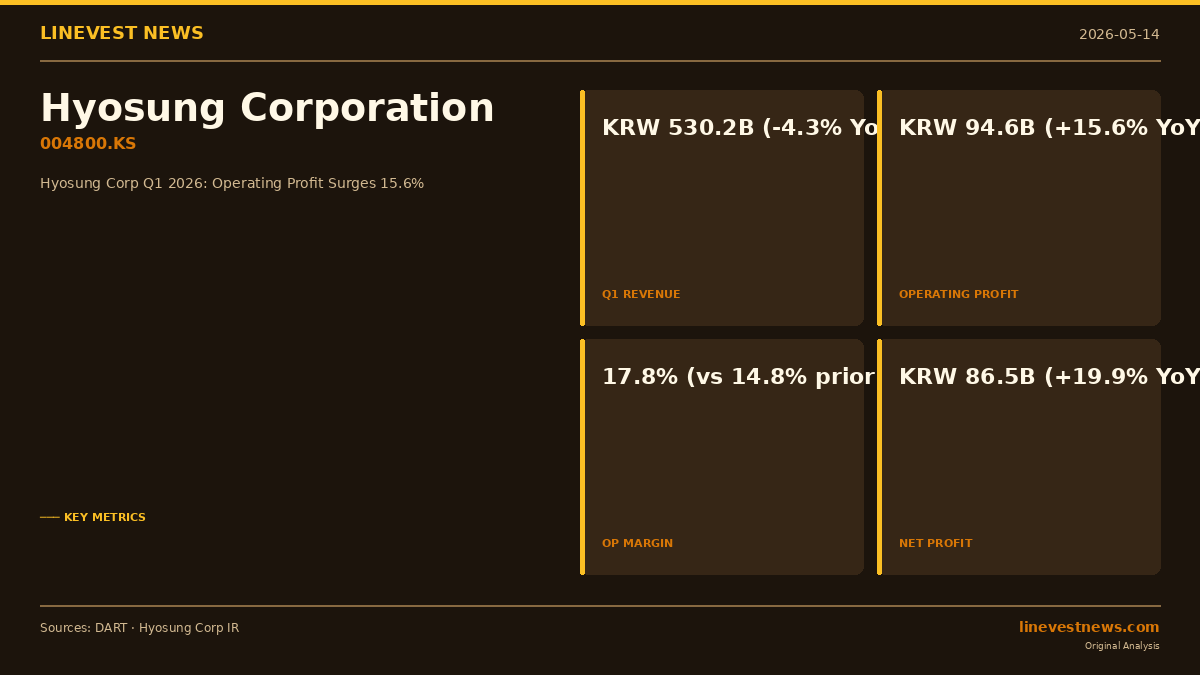

SEOUL, May 14, 2026 — Hyosung Corporation (004800.KS), the South Korean conglomerate holding company, reported a sharp improvement in profitability for the first quarter ended March 31, 2026, even as consolidated revenue declined modestly. Operating profit rose 15.6% year-on-year to KRW 94.6 billion (approximately USD 65.7 million), while revenue fell 4.3% to KRW 530.2 billion (USD 368.2 million), according to the company's quarterly report filed with DART on May 14.

Revenue Dip Masked by Margin Expansion

Hyosung Corp operates as a holding entity whose consolidated results include three directly operated business lines — financial automation equipment (IT/ATM), pump manufacturing, and a luxury automobile dealership — alongside equity income from its affiliates, including the separately listed Hyosung TNC (298020.KS), Hyosung Heavy Industries (298040.KS), Hyosung Chemical (298000.KS), and Hyosung Advanced Materials (298050.KS).

The top-line decline was concentrated in two segments. Revenue from the financial automation (IT/ATM) unit — operated by subsidiary Hyosung TNS, a maker of ATMs and cash-recycling machines sold globally — slipped 4.6% to KRW 298.3 billion, reflecting soft domestic ATM replacement demand as Korean banks continue to rationalize branch networks. More sharply, revenue from the luxury automobile dealership (FMK Co., Ltd., which holds dealership rights for Ferrari and Maserati in Korea) fell 33.7% to KRW 44.1 billion, weighed by lower deliveries of ultra-premium vehicles amid domestic consumer caution.

IT/ATM and Pump Units Drive Profitability Recovery

Despite the revenue headwinds, operating profit expanded decisively across the two core non-holding segments.

The IT/ATM unit's operating profit rose 58.4% to KRW 23.7 billion, lifting its operating margin to 7.9% from 4.8% a year earlier. Management attributed the improvement to a favorable shift in product mix toward higher-margin digital branch transformation solutions, which are being deployed at major U.S. banks including JPMorgan Chase as well as domestic Korean lenders.

The pump manufacturing segment — operated by Hyosung Goodsprings, Korea's leading industrial pump maker — posted an operating profit more than doubling to KRW 13.6 billion from KRW 6.7 billion, as revenue expanded 24.4% to KRW 63.8 billion. The surge reflected growing orders for nuclear-grade and seawater desalination pumps, where Hyosung Goodsprings holds the first KEPIC certification among domestic manufacturers. The unit's operating margin widened to 21.4% from 13.1%.

The luxury automobile dealership, by contrast, swung to an operating loss of KRW 0.7 billion from an operating profit of KRW 1.1 billion in Q1 2025, reflecting the sharp volume decline in Ferrari and Maserati deliveries and elevated fixed costs.

The holding segment itself — whose revenue encompasses equity-method income from the four listed Hyosung subsidiaries as well as royalties, leasing, and other recurring fees — was broadly stable, with operating profit of KRW 54.9 billion (+0.5% YoY).

Net Profit Rises 19.9%; Comprehensive Income Boosted by Equity Revaluation

Consolidated net profit rose 19.9% to KRW 86.5 billion. Net profit attributable to shareholders of Hyosung Corp reached KRW 73.3 billion (+12.7% YoY), translating to basic earnings per share of KRW 4,384, up from KRW 3,890 a year earlier.

Total comprehensive income more than doubled to KRW 144.4 billion from KRW 76.8 billion, primarily due to a KRW 50.8 billion unrealized gain on equity-method associates' revaluation — reflecting mark-to-market appreciation of Hyosung's stakes in its listed subsidiaries, which benefited from the broader KOSPI rally in early 2026.

Balance Sheet and Leverage

Total assets as of March 31, 2026 stood at KRW 5,641.5 billion, up 4.7% from KRW 5,387.1 billion at end-2025. Total liabilities were KRW 2,743.7 billion, with short-term debt rising to KRW 882.5 billion from KRW 622.0 billion at year-end, reflecting seasonal working-capital needs. Total equity reached KRW 2,897.8 billion, yielding a debt-to-equity ratio of approximately 94.7%.

Outlook

Hyosung Corp expects the IT/ATM unit to maintain margin improvement momentum as its "digital branch transformation" solutions gain traction in North America and Southeast Asia. The pump division is poised to benefit from South Korea's nuclear power plant expansion program — with ten new reactors planned through 2038 — and from growth in seawater desalination and hydrogen infrastructure projects. The luxury car segment's performance in upcoming quarters will depend on Ferrari's global model launch calendar and domestic consumer confidence.

Source: Hyosung Corporation Q1 2026 Quarterly Report (DART, filed May 14, 2026). Exchange rate: 1 USD = KRW 1,440 (approximate end-Q1 2026).

Hyosung Corporation (004800.KS) is a KOSPI-listed conglomerate holding company headquartered in Mapo-gu, Seoul. Its consolidated subsidiaries include Hyosung TNS (financial automation / ATM), Hyosung Goodsprings (industrial pumps), and FMK Co., Ltd. (Ferrari/Maserati dealership). Its four major separately listed subsidiaries — Hyosung TNC, Hyosung Heavy Industries, Hyosung Chemical, and Hyosung Advanced Materials — are not consolidated into this report.

Sources

- Hyosung Corporation Q1 2026 Quarterly Report — DART (rcept_no: 20260514001414)

- DART Financial Disclosure System (dart.fss.or.kr)