KCC Corporation Q1 2026: Net Income Surges 393% to KRW 217B as Investment Gains Overshadow Flat Revenue and Declining Operating Profit

Korea's largest materials group posts divergent results — silicone and paints revenue barely budge while a KRW 562 billion financial income windfall from investment securities drives earnings to a multi-year high.

Part A — The Big Picture

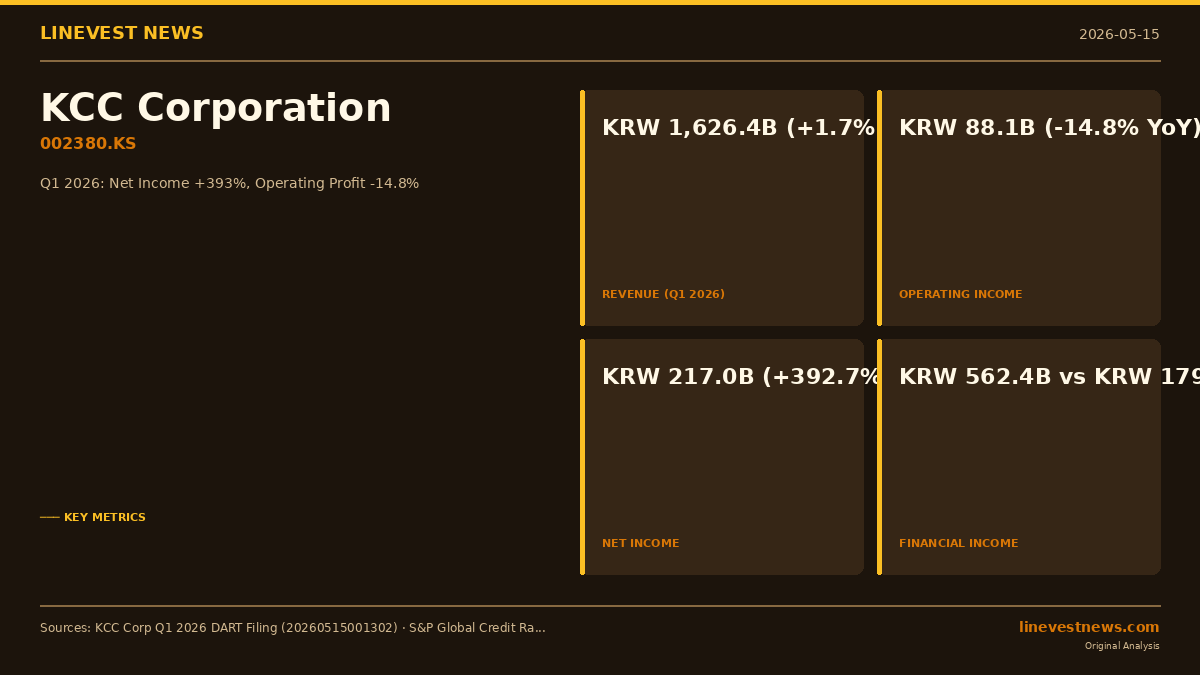

KCC Corporation (002380.KS), South Korea's leading building materials and specialty chemicals conglomerate, reported a dramatic divergence between operational and bottom-line performance in the first quarter of 2026, with consolidated net income surging 392.7% year-on-year to KRW 216.96 billion (approximately USD 157 million) even as operating profit fell 14.8% to KRW 88.1 billion.

The gap between the two metrics — the widest seen in recent quarterly history — was driven by a fourfold increase in financial income, which totalled KRW 562.4 billion in Q1 2026, up from KRW 179.4 billion a year earlier. Net financial income swung from a loss of KRW 50.7 billion in Q1 2025 to a gain of KRW 201.3 billion this quarter, adding roughly KRW 252 billion to pre-tax earnings and lifting consolidated pre-tax profit to KRW 312.5 billion (+314.4% YoY).

The primary source of the financial income surge is KCC's long-term investment in MOM Holding Company, the vehicle through which the Korean firm holds a controlling stake in Momentive Global, formerly known as Hexion's Performance Silicones division. KCC acquired Momentive in 2019 for approximately USD 3.1 billion in a landmark deal — the largest overseas acquisition by a Korean manufacturer at the time — and carries the investment in its balance sheet under non-current financial assets, which stood at KRW 5.539 trillion as of March 31, 2026, nearly double the KRW 2.767 trillion recorded at the end of fiscal 2024.

Revenue and Operations: A Tale of Modest Gains and Rising Costs

On a top-line basis, KCC's Q1 2026 consolidated revenue reached KRW 1,626.4 billion (USD 1.18 billion), up just 1.7% from KRW 1,599.3 billion in Q1 2025. The silicone segment continued to dominate, contributing 49.56% of sales with revenue of approximately KRW 1,132.5 billion. The paints and coatings segment accounted for 28.97% (approximately KRW 467.7 billion), while building materials contributed 14.19% (approximately KRW 230.8 billion).

Despite the revenue growth, gross profit expansion of KRW 7.2 billion was entirely offset by a KRW 22.5 billion rise in selling, general and administrative expenses. SG&A climbed to KRW 314.0 billion from KRW 291.5 billion a year ago — a 7.7% increase — suggesting that the company is investing in distribution capacity and personnel even as demand remains subdued in its domestic construction-linked businesses.

The building materials segment is navigating a particularly difficult environment. Korea's residential construction market remains in a prolonged slump following the 2022–2023 interest rate shock, with housing starts down sharply from peak levels. KCC's PVC and gypsum board products — sold to construction companies such as Hyundai E&C and Lotte E&C — face demand headwinds that are expected to persist through at least the first half of 2026.

In contrast, the paints and coatings business — which supplies marine and automotive coatings to Hyundai Motor (005380.KS) and HD Korea Shipbuilding & Offshore Engineering (009540.KS) — benefits from the current shipbuilding supercycle. Korean shipyards are operating at near-full capacity through 2028 under a record backlog, providing a structural tailwind for KCC's marine paint volumes.

Part B — Numbers, Context, and What Comes Next

Key Financials: Q1 2026 vs Q1 2025

| Metric | Q1 2026 | Q1 2025 | Change |

| Revenue | KRW 1,626.4B (USD 1.18B) | KRW 1,599.3B | +1.7% |

| Gross Profit | KRW 402.1B | KRW 394.9B | +1.8% |

| Operating Income | KRW 88.1B | KRW 103.4B | -14.8% |

| Financial Income | KRW 562.4B | KRW 179.4B | +213.4% |

| Financial Costs | KRW 361.1B | KRW 230.1B | +56.9% |

| Pre-tax Income | KRW 312.5B | KRW 75.4B | +314.4% |

| Net Income | KRW 217.0B (USD 157M) | KRW 44.1B | +392.7% |

| EPS (basic) | KRW 29,501 | KRW 5,991* | +392.5% |

*Q1 2025 EPS estimated from net income ÷ 7.352M shares outstanding

| Balance Sheet Item | Q1 2026 | FY 2025 | Change |

| Total Assets | KRW 17.62T | KRW 16.80T | +4.9% |

| Cash & Equivalents | KRW 1.469T | KRW 1.194T | +23.1% |

| Non-current Financial Assets | KRW 5.539T | KRW 5.459T | +1.5% |

| Total Equity | KRW 8.10T | KRW 7.82T | +3.5% |

| Total Debt | KRW 9.52T | KRW 8.98T | +6.1% |

The Momentive Factor

KCC's stake in Momentive Global represents the single most important variable in the company's financial results. Momentive — rebranded from the legacy GE Advanced Materials / Hexion silicone business — is one of the world's largest producers of silicone fluids, sealants, elastomers, and coatings, with manufacturing facilities across the United States, Germany, China, South Korea, and India.

The investment is classified as a non-current financial asset measured at fair value through other comprehensive income (FVOCI), meaning that changes in Momentive's valuation do not pass through the income statement on a mark-to-market basis in normal circumstances. However, dividends, interest, and certain realized components of the investment do flow to the income statement under the financial income line. The exact composition of the KRW 562.4 billion financial income — whether driven by dividends, intercompany transfers, or realization events — is expected to be detailed in the full-year disclosure.

S&P Global maintained KCC's international credit rating at BB+ (stable) as of March 8, 2026, unchanged from the prior year. Domestic ratings agencies — Korea Credit Rating (한국신용평가), Korea Ratings (한국기업평가), and NICE Credit Evaluation (NICE신용평가) — all maintained an AA- (stable) rating as of late April 2026, reflecting the company's solid domestic franchise and conservative financial management.

Segment and Cash Highlights

KCC ended Q1 2026 with cash and cash equivalents of KRW 1.469 trillion, up 23.1% from the KRW 1.194 trillion reported at end-2025. Total assets reached KRW 17.62 trillion, of which KRW 4.412 trillion is in property, plant and equipment and KRW 1.038 trillion in investment real estate.

The group consolidated 60 subsidiaries plus the parent as of March 31, 2026 — unchanged from end-2025. Key overseas subsidiaries include KCK, KCG, and KCTJ (China), KCS (Singapore), KCV (Vietnam), and KCT (Turkey). The China operations primarily serve the domestic Chinese construction and industrial market, where KCC has built a leading position in silicone sealants.

Outlook

KCC has not provided formal forward guidance for 2026. However, the structural dynamics point toward continued pressure on operating margins in building materials and a potential moderation in financial income once the Momentive valuation effect normalizes.

For equity investors, the stock's trajectory is heavily influenced by three variables: the performance of Momentive's US and European operations (exposed to North American and European construction and consumer markets), the pace of recovery in Korean residential construction, and the shipbuilding-cycle-driven demand for marine coatings. With silicones representing half of group revenue and the largest growth engine, any sign of global destocking in the specialty chemicals channel would be a material risk to watch.

KCC shares closed at KRW 260,000 on June 20, 2026, giving the company a market capitalization of approximately KRW 1.91 trillion (USD 1.38 billion).

*KCC Corporation (002380.KS) is listed on the Korea Stock Exchange. This article is based on the company's Q1 2026 quarterly report (분기보고서) filed with the Financial Supervisory Service on May 15, 2026. All financial figures are consolidated (연결) unless stated otherwise. USD figures converted at approximately KRW 1,380 per dollar.*

*Sources: KCC Corporation Q1 2026 Quarterly Report (DART rcept_no 20260515001302); S&P Global Credit Ratings; Korea Credit Rating; NICE Credit Evaluation.*