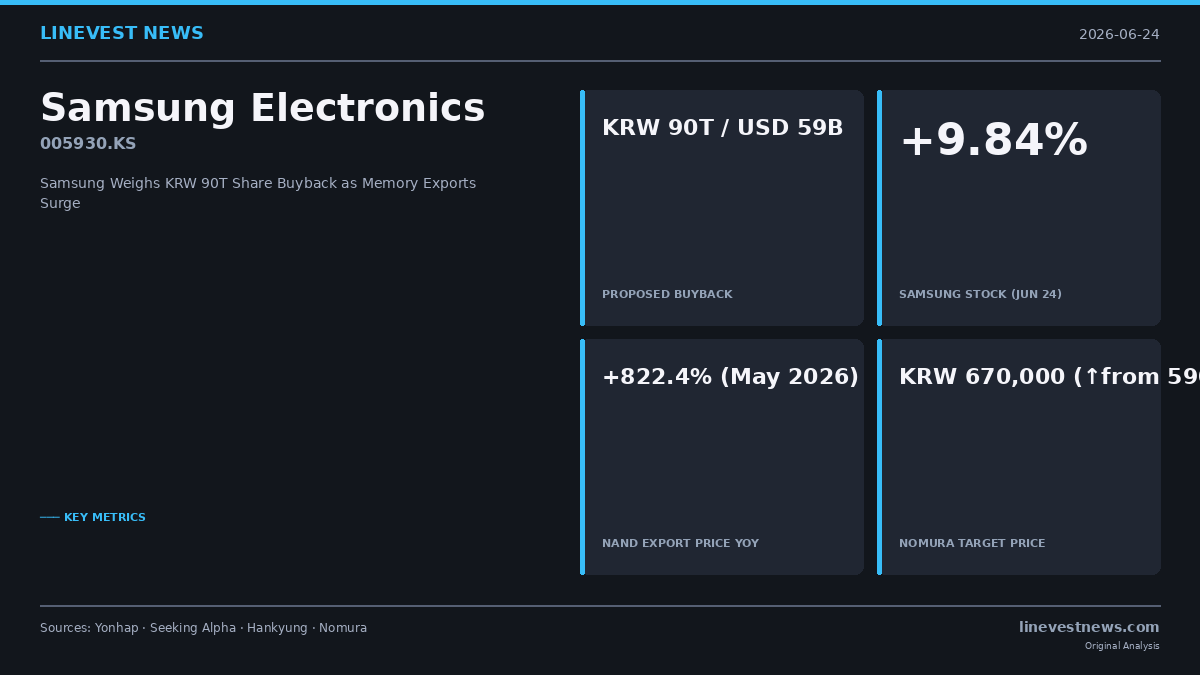

Samsung Electronics Co. (005930.KS) surged 9.84% on Wednesday after Yonhap News Agency reported the chipmaker is considering a buyback of up to KRW 90 trillion (USD 59 billion) in treasury shares — a scale that would dwarf any previous Korean corporate capital-return initiative and make it one of the largest buyback programmes in global semiconductor history.

The announcement restored Samsung to South Korea's No. 1 common-share market-capitalisation ranking, which it had briefly ceded to AI-memory rival SK Hynix. SK Hynix rose a comparatively modest 0.98% on the same day. Samsung's management tempered expectations, stating the company was "considering" the plan but that "no details including timing or size of the buyback had been decided."

Buyback Mechanics: Employee Equity Compensation at the Core

According to people familiar with the proposal, the repurchased treasury shares would primarily fund Samsung's stock-based employee-compensation plans introduced in October 2025. These include a Performance Stock Unit (PSU) programme and a chip-division bonus scheme calibrated at approximately 10.5% of annual operating profit. Under the proposed vesting structure, employees could sell one-third of awarded shares immediately upon receipt, with the remaining tranches unlocking after one and two-year holding periods.

The architecture mirrors Western big-tech equity practices and addresses a long-standing internal tension: unlike U.S. semiconductor peers such as Qualcomm or Broadcom, Samsung has historically concentrated bonus payments in cash, limiting employee alignment with long-run equity value.

Memory Cycle Provides the Earnings Firepower

The buyback deliberations come against an extraordinary memory-pricing backdrop. South Korea's May 2026 NAND flash export unit price surged 822.4% year-on-year to USD 153,384 per kilogram. Combined April–May memory semiconductor exports reached USD 34.91 billion (+342.3% YoY), with DRAM alone accounting for USD 22.1 billion (+380.6%) and NAND contributing USD 2.34 billion (+352.1%).

Analysts at Nomura raised their Samsung Electronics 12-month target price to KRW 670,000 from KRW 590,000, citing stronger-than-expected Q2 Device Solutions margins and noting that the bonus-cost impact on full-year earnings would be "lower than the market fears." The brokerage also highlighted a 96.2% historical correlation between chip-plant export data and Samsung's Device Solutions revenue, suggesting Q2 2026 results are on track to beat the Street consensus.

Shareholder-Value Catalyst in Focus

If confirmed at the reported scale, the buyback would represent a fundamental shift in Samsung's capital-allocation doctrine. The company currently holds roughly KRW 95 trillion in net cash — one of the largest corporate cash hoards in Asia — and has faced recurring criticism from both activist shareholders and institutional investors over its reluctance to return capital.

Samsung has not disclosed a board-meeting timeline for a formal decision. Continued clarity on the programme's scale and cadence is expected to remain a key near-term catalyst for Korea's largest company by market capitalisation.

Sources: Yonhap News Agency, Seeking Alpha, Hankyung, MK Economy, Nomura Research