POSCO DX Q1 2026: Operating Profit Collapses 84% as Parent Group's Capex Pullback Deepens

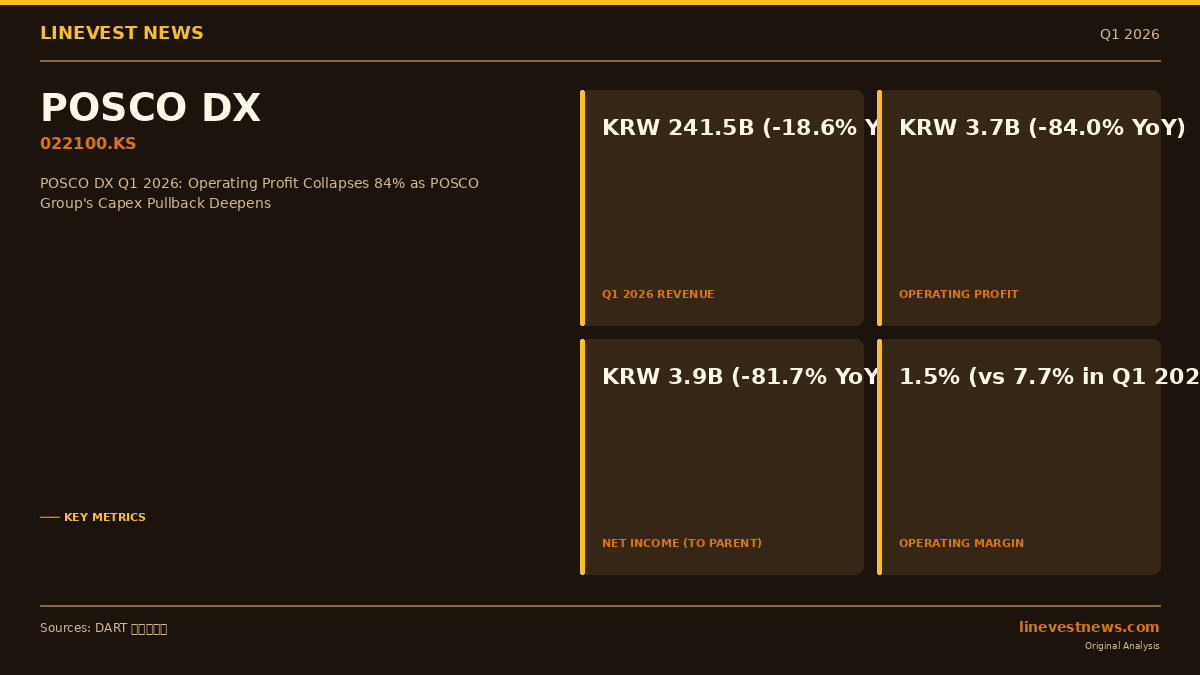

POSCO DX (KRX: 022100), the digital transformation and automation arm of South Korea's POSCO Group, reported a sharp deterioration in first-quarter 2026 results as reduced capital expenditure across its parent group weighed heavily on both revenue and profitability. Consolidated revenue for the January–March 2026 period came in at KRW 241.5 billion (approximately USD 175 million), down 18.6% year-on-year, while operating profit plunged 84.0% to KRW 3.7 billion — compressing the operating margin from 7.7% in Q1 2025 to just 1.5%.

Part A — Key Financials at a Glance

Net income attributable to the parent fell 81.7% to KRW 3.9 billion, against KRW 21.5 billion in the prior-year quarter. A notable cushion came from financial income, which rose 51.5% to KRW 3.2 billion, helping lift pre-tax profit to KRW 5.8 billion and keep the bottom line in the black despite the operating profit slump.

The company's balance sheet remained sound: total equity stood at KRW 560.4 billion at end-March 2026, and total assets edged down to KRW 808.4 billion from KRW 834.4 billion at the end of FY2025, driven by lower trade receivables as project volumes declined.

Part B — Segment Detail and Business Context

Automation vs IT Services: Both Divisions Compressed

POSCO DX operates two primary segments: Automation (factory control and robotics) and IT Services (enterprise IT, cloud, AI platforms). In Q1 2026, the Automation segment generated KRW 111.5 billion in revenue (46% of total), contributing KRW 2.0 billion in operating profit at a margin of 1.8%. The IT Services segment, accounting for 54% of revenue (KRW 131.2 billion), added approximately KRW 1.7 billion in operating profit at a margin of roughly 1.3%.

Both margins represent a dramatic compression compared with the FY2024 blended margin of 7.4%, reflecting lower project volumes and an unfavourable revenue mix as smaller, lower-margin maintenance contracts replaced larger system integration (SI) deployments.

POSCO Group Dependency: The Core Structural Risk

The single most significant factor behind the earnings deterioration is POSCO DX's heavy reliance on its parent group. POSCO Holdings has been navigating headwinds on two fronts since 2024: a cyclical downturn in the global steel market driven by Chinese oversupply, and a correction in battery-material prices — lithium and cathode materials — that has slowed capex across the group's secondary-battery value chain. With fewer large steel-plant upgrades and battery-factory buildouts to execute, POSCO DX's project pipeline thinned materially.

The severity of the decline is visible in the multi-year trend: FY2024 annual revenue of KRW 1,473.3 billion fell to KRW 1,075.2 billion in FY2025 (a 27.0% drop), and Q1 2026's annualised run rate of roughly KRW 966 billion suggests further contraction is possible if group capex does not recover.

Order Backlog Provides Near-Term Visibility

One mitigating factor is the order backlog, which stood at KRW 960.2 billion as of 31 March 2026. IT Services accounts for KRW 336.9 billion of the pipeline and Automation for KRW 623.3 billion, suggesting the automation segment still has contracted work to deliver over coming quarters. Against the annualised revenue run-rate of roughly KRW 966 billion, the backlog represents approximately one year of revenue cover — a modest but meaningful buffer.

AI and Physical Intelligence Investment Accelerates

Despite near-term financial pressure, POSCO DX is accelerating its strategic pivot toward artificial intelligence and advanced automation. R&D expenditure as a share of revenue rose to 1.75% in Q1 2026, up from 0.98% for the full year FY2025 and just 0.60% in FY2024, signalling a deliberate ramp-up in technology investment even as margins remain thin.

The company's AI roadmap centres on three pillars: P-GPT, a proprietary large-language-model platform tailored for POSCO Group's internal workflows; Physical AI developed in partnership with Nvidia's Omniverse platform, designed to embed AI-driven perception and control into real-world industrial environments such as steel plants; and a private 5G network business built on the company's Eum 5G wireless designation obtained in September 2023. POSCO DX is also pursuing robotics system integration (SI) for industrial settings, pairing process expertise with third-party hardware from domestic and international robot manufacturers.

Outlook: Recovery Hinged on POSCO Group Capex Cycle

Recovery in POSCO DX's results is likely contingent on a resumption of POSCO Group capital spending, which in turn depends on a stabilisation of steel prices and a rebound in battery-material demand — both of which remain uncertain in the near term. The company's effort to diversify beyond its parent into third-party industrial clients and government-related infrastructure projects (airports, highways, smart buildings) is a longer-term de-risking measure unlikely to offset the parent-group headwind in the immediate future.

Investors should monitor: (1) POSCO Holdings' updated capex guidance for FY2026; (2) progress on external contract wins in Physical AI and 5G automation; and (3) whether the order backlog holds above KRW 900 billion through mid-year, which would signal stabilisation of new project intake.

Sources: DART Quarterly Report (분기보고서), Q1 2026, POSCO DX (주식회사 포스코디엑스), filed 15 May 2026 (DART receipt no. 20260515000401).