Western Beauty Giants Confront Costly Lesson in Korean Brand Management

The global beauty M&A wave that saw Unilever, Estée Lauder, and L'Oréal pour billions of dollars into Korean cosmetics brands between 2017 and 2021 is now exposing its fault lines. A decade after the first marquee deals closed, all three multinationals are grappling with declining performance at their Korean acquisitions — and domestic operators are beginning to circle the assets at steep discounts.

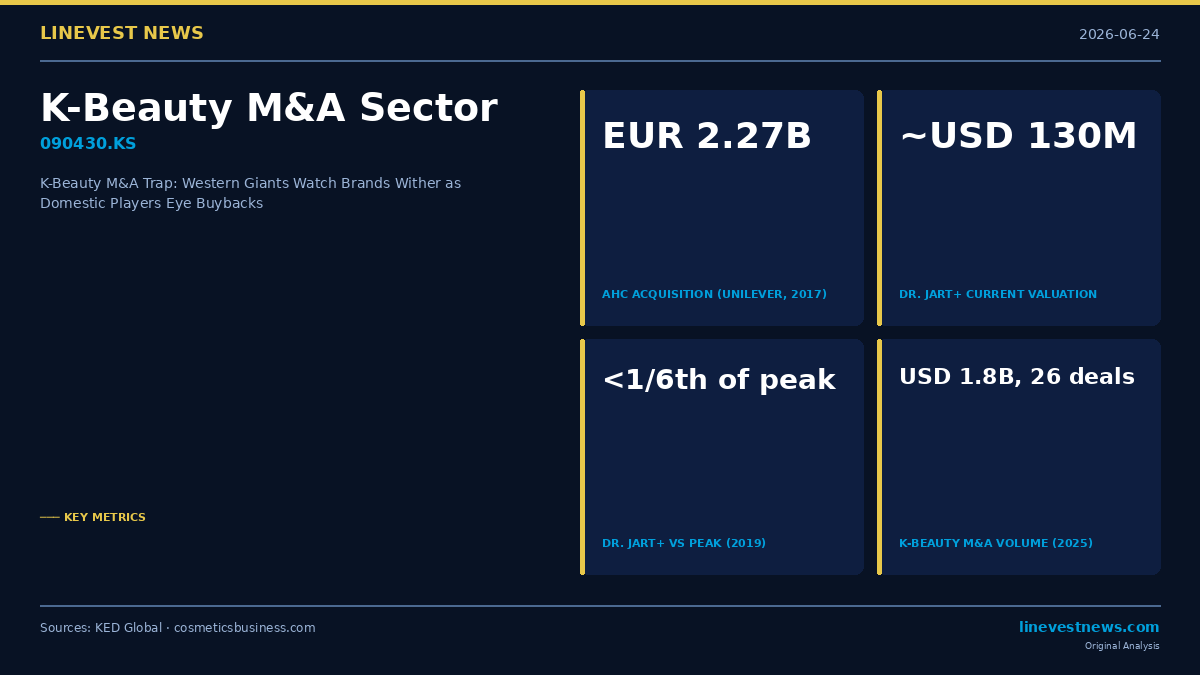

The most striking illustration is Estée Lauder's Dr. Jart+. The dermatology-inspired skincare brand, which the New York-based beauty group gradually acquired between 2015 and 2021, is now being discussed in the market at approximately USD 130 million — less than one-sixth of its 2019 peak valuation, according to people familiar with the matter. The Founders Inc., the Seoul-based beauty incubator behind the fast-growing Anua brand, is reportedly exploring an acquisition, KED Global reported on June 23.

The story echoes across multiple brands. Unilever paid €2.27 billion (approximately USD 2.7 billion) for Carver Korea — owner of the AHC skincare franchise — in 2017, betting on the brand's strong following among Asian millennials. L'Oréal acquired Stylenanda, the Korean lifestyle company behind the 3CE makeup brand, in 2018. AHC, Dr. Jart+, Dr.G, and 3CE have all since seen earnings decline, according to industry sources cited by KED Global, squeezed between weakening demand from China and what insiders describe as multinational conglomerates' rigid corporate practices.

Why the K-Beauty Formula Breaks Down Under Western Ownership

The failure pattern runs deeper than any individual brand misstep. K-beauty's competitive edge depends on short innovation cycles — brands typically launch new SKUs every four to eight weeks — hyper-responsive product development tied to real-time social media signals, and a direct feedback loop with Korean retailers and content creators. When those brands transfer to the umbrella of large Western corporations, with their multi-tier approval chains, centralised R&D governance, and globally standardised marketing playbooks, that agility erodes.

All three major acquisitions also coincided with a period of peak Chinese cross-border e-commerce demand for Korean beauty products. As China's domestic economy cooled and the novelty premium attached to K-beauty faded in that market, the revenue trajectories underpinning those deal valuations were exposed. For brands under Western ownership, the ability to rapidly pivot — launching China-specific formulations, leaning into live-commerce platforms, or partnering with domestic Chinese daigou networks — was constrained by headquarters approval requirements that Korean-run operators do not face.

Domestic Operators Circle Back

The calculus is now reversing. The Founders' potential bid for Dr. Jart+ represents part of a broader thesis in Korean investment circles: domestic operators, running leaner structures and retaining cultural proximity to both the brands and their target consumers, may be better positioned to revive faded properties than the Western groups that originally acquired them.

K-beauty M&A activity reached a post-COVID record in 2025, with 26 deals totalling USD 1.8 billion according to industry data. But the character of that activity is shifting: from foreign buyers paying peak-cycle premiums to domestic operators selectively acquiring distressed assets that still carry genuine brand equity and name recognition.

For investors tracking the Korean cosmetics sector on KOSPI, the reversal has broader implications. Amorepacific Corp. (090430.KS) and LG H&H Co. (051900.KS) — both of which pursued largely organic brand-building strategies and retained ownership of their key franchises rather than selling to multinationals — may emerge as structural beneficiaries as the K-beauty brand ecosystem realigns around domestic ownership models. Their refusal to sell at peak valuations, once criticised by some investors as forgoing liquidity events, now looks prescient.

Sources

- K-beauty M&A trap: Unilever, Estée Lauder, L'Oréal struggle after Korean brand acquisitions — KED Global, June 24 2026

- K-beauty firm The Founders eyes acquisition of Dr. Jart+ from Estée Lauder — KED Global, June 23 2026

- Is K-beauty incubator The Founders looking to acquire Dr. Jart+? — cosmeticsbusiness.com