EcoPro Materials Swings to Profit in Q1 2026 as Indonesian Smelter Consolidation Drives 22% Revenue Jump

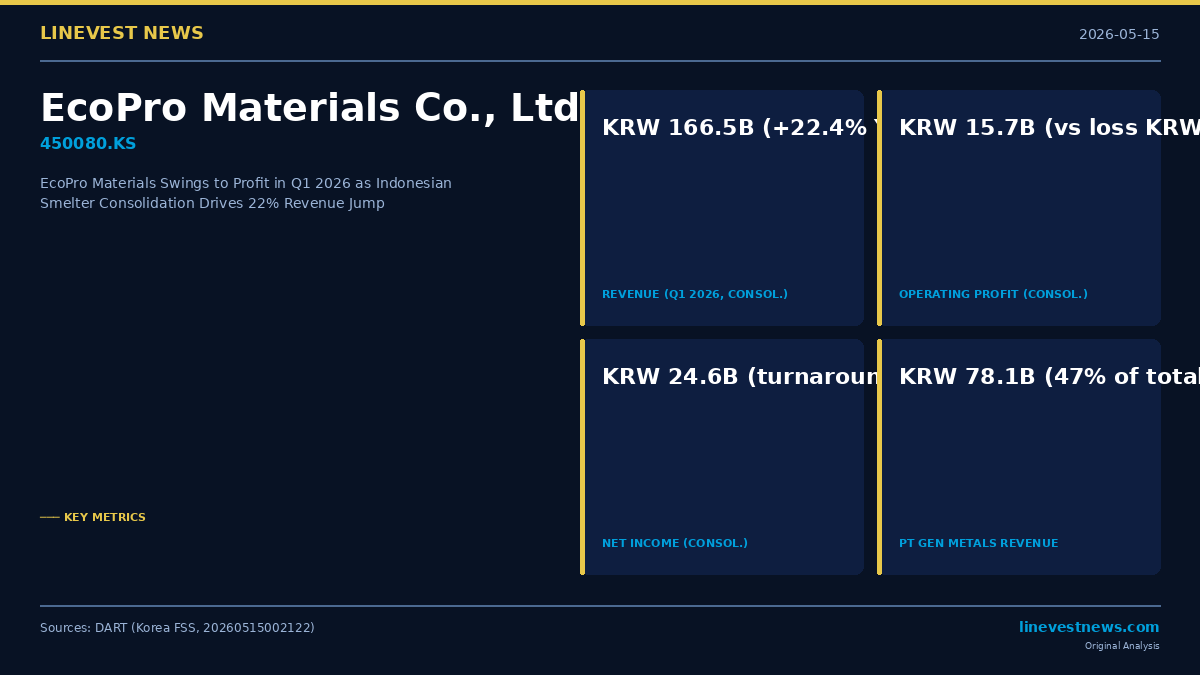

EcoPro Materials Co., Ltd. (450080.KS) posted its first profitable quarter in years during Q1 2026, as the Pohang-based cathode precursor maker reversed an operating loss of KRW 14.8 billion (USD 10.2 million) a year earlier to report a consolidated operating profit of KRW 15.7 billion (USD 10.8 million), according to its quarterly report filed with Korea's Financial Supervisory Service on May 15, 2026.

The turnaround coincided with the company's first-ever consolidated financial reporting period — a pivotal structural shift triggered by EcoPro Materials' completed acquisition of PT Green Eco Nickel (PT GEN), an Indonesian nickel smelter located at the Morowali Industrial Park (IMIP) in Sulawesi. The newly consolidated subsidiary contributed the majority of a newly added metals segment that accounted for nearly half of total revenues.

Key Financials at a Glance

On a consolidated basis — which reflects PT GEN for the first time — EcoPro Materials reported Q1 2026 revenues of KRW 166.5 billion (USD 114.8 million), up 22.4% from the KRW 136.1 billion that the standalone entity reported in Q1 2025. Gross profit swung from a loss of KRW 6.2 billion to a profit of KRW 36.4 billion, translating to a gross margin of 21.8% versus a negative 4.5% a year earlier.

Operating profit reached KRW 15.7 billion (USD 10.8 million), or a margin of 9.4%, against an operating loss of KRW 14.8 billion in Q1 2025. Finance income of KRW 15.2 billion — largely reflecting interest and foreign-exchange gains — helped push pre-tax income to KRW 26.5 billion, while net income attributable to controlling shareholders came in at KRW 24.6 billion (USD 17.0 million), reversing a net loss of KRW 7.3 billion. Basic earnings per share stood at KRW 198.

However, investors should note the accounting context: the Q1 2025 comparatives are drawn from standalone (non-consolidated) financials, as the company only began reporting on a consolidated basis from Q1 2026. A like-for-like comparison of standalone EcoPro Materials — excluding PT GEN — shows that the parent entity's own revenues declined 27.2% year-on-year to KRW 99.0 billion in Q1 2026, though the standalone entity also returned to operating profitability with a KRW 2.3 billion operating profit, compared to a loss of KRW 14.8 billion in Q1 2025.

PT Green Eco Nickel: The New Growth Engine

The headline revenue growth is almost entirely explained by the PT GEN consolidation. The metals segment — which encompasses nickel intermediates and cobalt byproducts processed at the Indonesian smelter — generated KRW 78.1 billion (USD 53.9 million), or 46.9% of total consolidated revenues, in Q1 2026. There was no comparable metals segment revenue in prior periods.

PT GEN is located at IMIP in Morowali, Central Sulawesi, Indonesia — the world's largest nickel-processing industrial park — and processes nickel ore into Mixed Hydroxide Precipitate (MHP) and Metal Composite Precipitate (MCP), which are intermediate feedstocks for EcoPro Materials' own precursor production as well as for external sales to cathode active material makers. The subsidiary added a nickel MHP production capacity of 20,000 tonnes per year (on a nickel-content basis) to EcoPro Materials' manufacturing footprint, alongside its existing Korean operations' 50,000-tonne annual cathode precursor capacity (two production lines: CPM1 at 24,000 tonnes/yr and CPM2 at 26,000 tonnes/yr).

The balance sheet consequences of the PT GEN acquisition are substantial. Total consolidated assets jumped 65.1% quarter-on-quarter — from KRW 1,729.1 billion at end-December 2025 to KRW 2,854.3 billion (USD 1.97 billion) at end-March 2026. Property, plant and equipment nearly tripled in Q1 2026, growing from KRW 400.0 billion to KRW 1,020.9 billion as PT GEN's production facilities were added to the consolidated balance sheet. A non-controlling interest of KRW 324.8 billion reflects minority shareholders' stake in PT GEN.

The leverage position also widened: total debt rose to KRW 1,367.8 billion, up from KRW 584.4 billion at year-end 2025. The debt-to-equity ratio stands at approximately 0.92x on the consolidated basis.

Precursor Operations and Customer Base

EcoPro Materials' original business — manufacturing nickel-manganese-cobalt (NCM) cathode precursors for lithium-ion batteries — generated KRW 68.2 billion (USD 47.1 million) in Q1 2026, accounting for 41.0% of total consolidated revenues. Commercial product sales (primarily raw materials trading) added a further KRW 20.2 billion (12.1%).

The company's primary customer for precursors is EcoPro BM, its sister subsidiary within the EcoPro Group that manufactures cathode active materials. EcoPro BM and affiliated cathode makers accounted for 41% of revenues. Metals sales from PT GEN flowed to both domestic cathode producers (KRW 48.3 billion) and overseas buyers (KRW 19.2 billion).

Separately, on a standalone basis, domestic precursor sales totalled KRW 100.1 billion while overseas precursor and metals exports came to KRW 46.2 billion, for a combined standalone total of KRW 146.4 billion in core product categories before commercial merchandise.

Raw Material Dynamics: Nickel and Cobalt in Flux

EcoPro Materials' cost structure is dominated by nickel, which accounted for 92.7% of raw material purchases in Q1 2026 (total raw material spend: KRW 108.6 billion). The company notes that international nickel prices fell approximately 30% over the three years through March 2026, driven by a supply glut from Indonesia — which now produces 52% of the world's refined nickel and saw output grow 24.7% year-on-year through mid-2025.

The prolonged price decline, while compressing per-unit margins on nickel intermediate sales from PT GEN, simultaneously reduced input costs for EcoPro Materials' precursor operations, helping restore positive gross margins on the standalone business. Fastmarkets forecast cited in the filing projects LME nickel spot prices recovering to an average USD 15,241/tonne in 2025, rising to USD 16,207/tonne in 2026 and USD 17,237/tonne in 2027, as supply cuts and tightening environmental regulations slow new production growth.

On cobalt — the other key input for NCM precursors — EcoPro Materials is positioned as a partial beneficiary of the current price surge. The DRC's export ban on cobalt, announced in February 2025, drove prices above USD 19/lb, a spike of more than 30%. While EV manufacturers have responded by accelerating the shift toward cobalt-free LFP chemistries or lower-cobalt mid-nickel battery formulations, the timeline for this demand substitution means near-term cobalt supply tightness persists. Crucially, PT GEN produces cobalt as a byproduct of its nickel smelting process, providing EcoPro Materials a degree of natural hedge and revenue upside as cobalt prices remain elevated.

Strategic Context and Vertical Integration

The acquisition of PT GEN represents the completion of EcoPro Materials' stated vertical integration strategy, announced in 2021, to extend its value chain "upstream" from cathode precursor synthesis toward primary raw material smelting. The company now controls a supply chain spanning from Indonesian nickel ore through intermediate MHP/MCP production at PT GEN in Sulawesi, to cathode precursor manufacturing at its Pohang plants (RMP 1/2 and CPM 1/2), and ultimately to EcoPro BM's cathode active materials sold to battery cell makers.

Management describes the strategic rationale in the filing as securing "stable nickel supply and additional cost competitiveness," particularly important in a global battery supply chain increasingly subject to origin requirements under the EU Battery Regulation, the US Inflation Reduction Act's critical mineral rules, and analogous de-China sourcing policies among major automakers.

EcoPro Materials was established in April 2017 as EcoPro GEM (renamed in March 2022) and listed on the KOSPI. Representative Director Lee Gyu-bong leads the company. The auditor for both standalone and consolidated Q1 2026 financials is Samjong KPMG.

Sources: DART (Korea FSS), EcoPro Materials Q1 2026 Quarterly Report (Acceptance No. 20260515002122, filed 2026-05-15). Financial figures in Korean won (KRW); USD conversions at approximately 1,450 KRW/USD.

Sources: DART (Korea FSS), EcoPro Materials Q1 2026 Quarterly Report (Acceptance No. 20260515002122, filed 2026-05-15).