Samsung E&A Reports 20% Jump in Q1 Operating Profit as Middle East Drives Revenue Shift

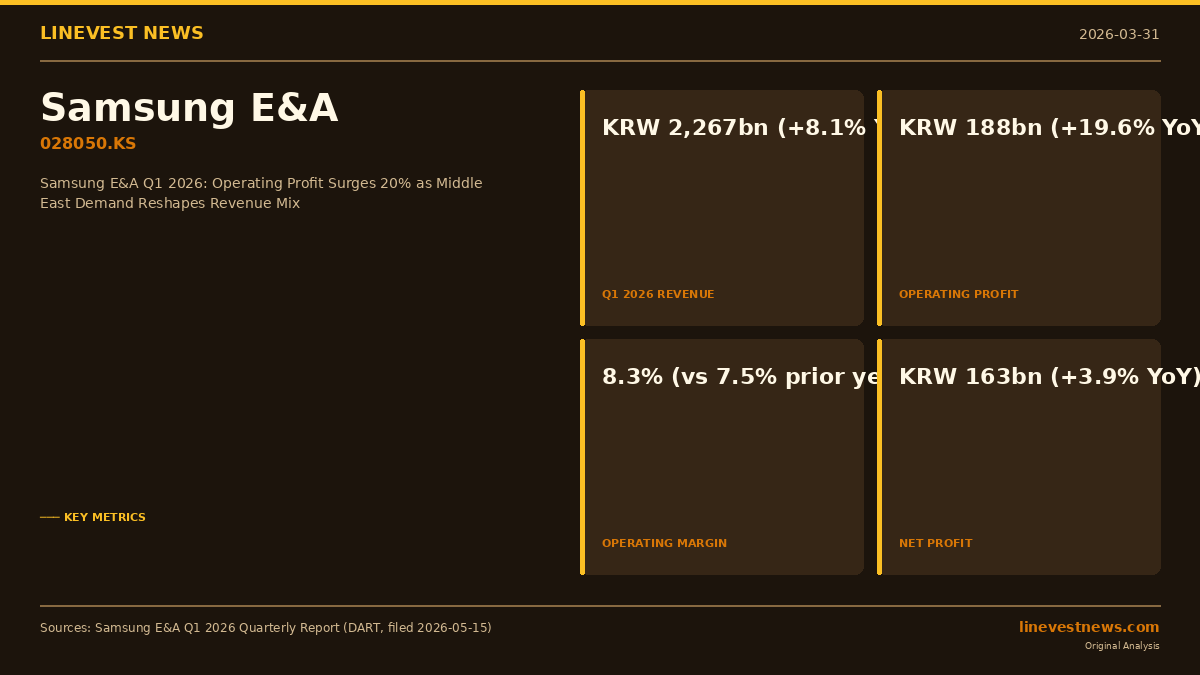

Samsung E&A Co., Ltd. (028050.KS), South Korea's leading plant engineering and construction (EPC) firm and a flagship subsidiary of the Samsung Group, posted a strong set of first-quarter 2026 results, with consolidated operating profit surging 19.6% year-over-year to KRW 188.2 billion (approximately USD 137 million) as overseas demand — particularly from the Middle East — continues to reshape the company's revenue profile.

Revenue for the three months ended March 31, 2026 rose 8.1% to KRW 2,267.4 billion (approximately USD 1.65 billion) from KRW 2,098.0 billion in Q1 2025, according to the quarterly report filed with Korea's Financial Supervisory Service on May 15, 2026. Net profit for the quarter came in at KRW 163.3 billion, up 3.9% from KRW 157.2 billion in the same period last year.

Operating Margin Expansion on Improved Project Mix

The company's operating margin improved to 8.3% in Q1 2026 from 7.5% in Q1 2025, reflecting a favorable project execution mix and improving cost efficiency. Gross profit climbed 16.9% to KRW 343.8 billion, with the gross margin widening to 15.2% from 14.0% a year earlier.

Samsung E&A's selling, general and administrative expenses rose to KRW 155.6 billion from KRW 136.7 billion, reflecting continued investment in talent and project management capabilities as the firm scales its overseas operations. Pre-tax income reached KRW 208.8 billion, roughly in line with Q1 2025's KRW 204.6 billion, as financing income partially offset higher operating expenditure.

Middle East Cement Samsung E&A's Global Pivot

The most striking feature of Q1 2026 results is the continuing geographic rebalancing. Revenue from the Middle East and other regions surged 33.2% year-over-year to KRW 1,321.5 billion, accounting for 58.3% of total Q1 revenue — up from 47.3% in Q1 2025. Key clients in the region include Saudi Aramco (Saudi Arabian Oil Company), ADNOC (Abu Dhabi National Oil Company), and Qatar Energy.

In contrast, domestic (South Korea) revenue fell 34.7% to KRW 556.7 billion, retreating from KRW 852.5 billion a year earlier, as the company deliberately focuses management resources and capital on higher-margin international projects. Americas revenue surged 55.9% to KRW 139.8 billion, while Asia revenue expanded 52.3% to KRW 249.4 billion.

"The global energy transition and Middle East infrastructure boom are structurally favorable for Samsung E&A's growth trajectory," management noted in the report's risk disclosure section, highlighting long-term contracts with state-owned energy companies in the Gulf Cooperation Council as the firm's primary growth driver.

Chemicals Lead, New Energy Gains Share

By business segment, the Chemicals division — covering oil and gas processing, refining, and petrochemicals — remained the largest contributor, accounting for 49.8% of Q1 2026 revenue at KRW 1,129.2 billion. The Advanced Industries segment, which encompasses semiconductor and display plant construction as well as biopharma facilities, contributed 25.3% (KRW 574.2 billion).

Notably, the New Energy segment — spanning LNG, clean energy (hydrogen, carbon capture), and ECO water and waste treatment — expanded its revenue share to 24.9% (KRW 564.0 billion) in Q1 2026, a sharp increase from 14.9% for the full year 2025. Management has previously signaled its intent to grow this segment as global decarbonization trends and LNG demand accelerate.

Backlog Provides Two-Year Revenue Visibility

As of March 31, 2026, Samsung E&A's consolidated construction contract backlog stood at KRW 17,768.2 billion (approximately USD 12.9 billion), equating to roughly two years of annual revenue at the company's FY2025 run rate. The overseas backlog is dominated by hydrocarbon and industrial plant projects in Saudi Arabia and the UAE, while the domestic segment's backlog includes semiconductor and industrial facility contracts with Samsung Electronics and other affiliates.

The main backlog table (principal projects only, base contract value above KRW 90.3 billion) shows: - Domestic private sector (including Samsung Electronics) backlog: KRW 3,598.1 billion - Overseas (Saudi Aramco and others) backlog: KRW 13,720.5 billion

Balance Sheet Remains Solid

Total assets as of March 31, 2026 were KRW 10,225.1 billion, up from KRW 10,039.6 billion at year-end 2025. The company holds KRW 1,529.0 billion in cash and cash equivalents, up sharply from KRW 861.8 billion at December 31, 2025 — a testament to strong Q1 operating cash generation. Short-term financial instruments add another KRW 2,032.4 billion, giving Samsung E&A liquidity of approximately KRW 3,561 billion (USD 2.6 billion).

Total equity attributable to controlling shareholders reached KRW 4,803.8 billion, while total debt-to-equity stood at 126.5%, down from a comparable period in prior years. The company carries no material bank borrowings, relying instead on advance payments and project milestones to fund construction activity.

Outlook: Global EPC Cycle Remains Favorable

Samsung E&A stock (028050.KS) closed at KRW 49,900 on June 22, 2026, giving the company a market capitalization of approximately KRW 9.78 trillion (USD 7.1 billion). Shares have recovered significantly from a 52-week low of KRW 21,750, though they remain below the 52-week high of KRW 67,300 reached during the 2025 EPC re-rating cycle.

The global EPC sector is broadly supported by sustained upstream energy investment in the Middle East, a resurgence in LNG facility construction, and continued semiconductor capex from Samsung Electronics and its peers — all of which underpin Samsung E&A's multi-year order pipeline. Key near-term execution risks include foreign-exchange volatility on USD-denominated overseas contracts and potential project cost overruns.

Source: Samsung E&A Q1 2026 Quarterly Report (분기보고서), filed May 15, 2026 via DART (Financial Supervisory Service of Korea). All figures in Korean Won (KRW) unless otherwise stated. USD conversions approximate at KRW 1,375/USD.

Sources: Samsung E&A Q1 2026 Quarterly Report (분기보고서), filed May 15, 2026 via DART (Financial Supervisory Service of Korea); yfinance (Samsung E&A stock price 028050.KS).