Part A — Key Numbers

CJ CheilJedang Corp (097950.KS), South Korea's largest food-and-bio conglomerate, reported consolidated first-quarter 2026 results on 15 May that drew a sharp line between operating and bottom-line performance: operating profit fell nearly a third from a year earlier, yet net income more than doubled.

| Metric | Q1 2026 | Q1 2025 | Change |

|---|---|---|---|

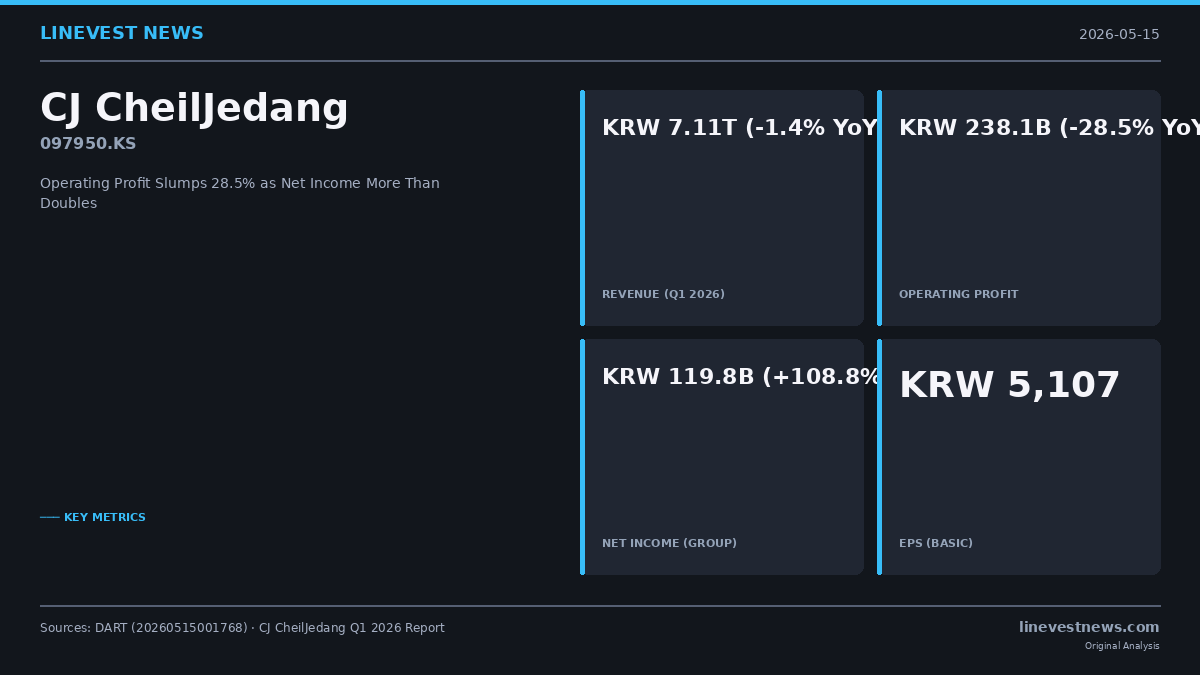

| Revenue | KRW 7.11T (USD 5.16B) | KRW 7.21T | -1.4% |

| Gross Profit | KRW 1.56T | KRW 1.59T | -1.7% |

| Operating Profit | KRW 238.1B | KRW 333.2B | -28.5% |

| Operating Margin | 3.3% | 4.6% | -130 bps |

| Pre-tax Income | KRW 169.6B | KRW 182.0B | -6.8% |

| Net Income (Group) | KRW 119.8B (USD 86.8M) | KRW 57.4B | +108.8% |

| Net Income (Parent Shareholders) | KRW 81.8B | KRW 17.6B | +363.8% |

| EPS (Basic, Common) | KRW 5,107 | — | — |

Source: DART filing 20260515001768, CFS basis. USD converted at approximately KRW 1,380.

Part B — Analysis

Operating Profit: A Two-Headed Story

The 28.5% decline in operating profit is the headline concern, and it traces to two distinct pressures. First, selling, general and administrative costs rose 5.4% year-on-year to KRW 1.32 trillion — widening faster than revenue could absorb. Second, consolidated gross profit declined KRW 27 billion, as revenue slid marginally across the food processing and BIO (amino acids, nucleotides) segments. Together, the two factors eroded KRW 95 billion from operating income.

At the standalone level the picture is starker: the parent entity posted an operating loss of KRW 8.6 billion and a net loss of KRW 89.6 billion on revenue of KRW 1.87 trillion, underlining that CJ CheilJedang's profitability currently rests on subsidiary performance rather than its own manufacturing operations.

Net Income Surge: Tax, Finance, and a Divestiture

Below the operating line, three tailwinds lifted net income to KRW 119.8 billion:

Tax normalisation. The effective tax rate fell sharply — from approximately 68% in Q1 2025 to 38% in Q1 2026. The prior-year quarter's unusually high tax charge had suppressed reported earnings, creating a low base that amplified the year-on-year comparison.

Improved net financial charges. Net finance costs narrowed by roughly KRW 41 billion year-on-year, as financial income rose 6.6% while financial costs fell 11%.

Discontinued-operations gain. CJ CheilJedang recorded KRW 15.1 billion from discontinued operations — a line absent in the prior-year quarter — reflecting partial proceeds or a mark-to-market on business disposals. Assets classified as held for sale on the balance sheet stood at KRW 1.29 trillion at year-end 2025 and collapsed to KRW 34 billion by 31 March 2026, confirming that a significant portfolio disposal closed during the quarter.

Balance Sheet: Solid Equity, Rising Leverage

Total assets rose to KRW 31.0 trillion from KRW 29.7 trillion at December 2025, driven by a KRW 381.7 billion positive foreign-currency translation adjustment — evidence of material overseas earnings streams benefiting from KRW depreciation. Total equity expanded to KRW 12.0 trillion (equity ratio ~38.8%). Short-term borrowings grew to KRW 3.10 trillion from KRW 2.76 trillion. Leverage remains manageable but warrants monitoring as SG&A trends higher.

Outlook

CJ CheilJedang continues to reshape its portfolio, with the BIO segment's commodity amino-acid operations under strategic review. Analysts will focus on whether the Q1 SG&A expansion is a one-off investment in global Bibigo brand growth or a structural cost creep. Management has not issued revised full-year guidance, and consensus estimates will likely be revisited following this quarter's operating shortfall.

Sources: DART Q1 2026 filing (rcept_no 20260515001768), CJ CheilJedang consolidated financial statements (K-IFRS).

"