Executive Summary

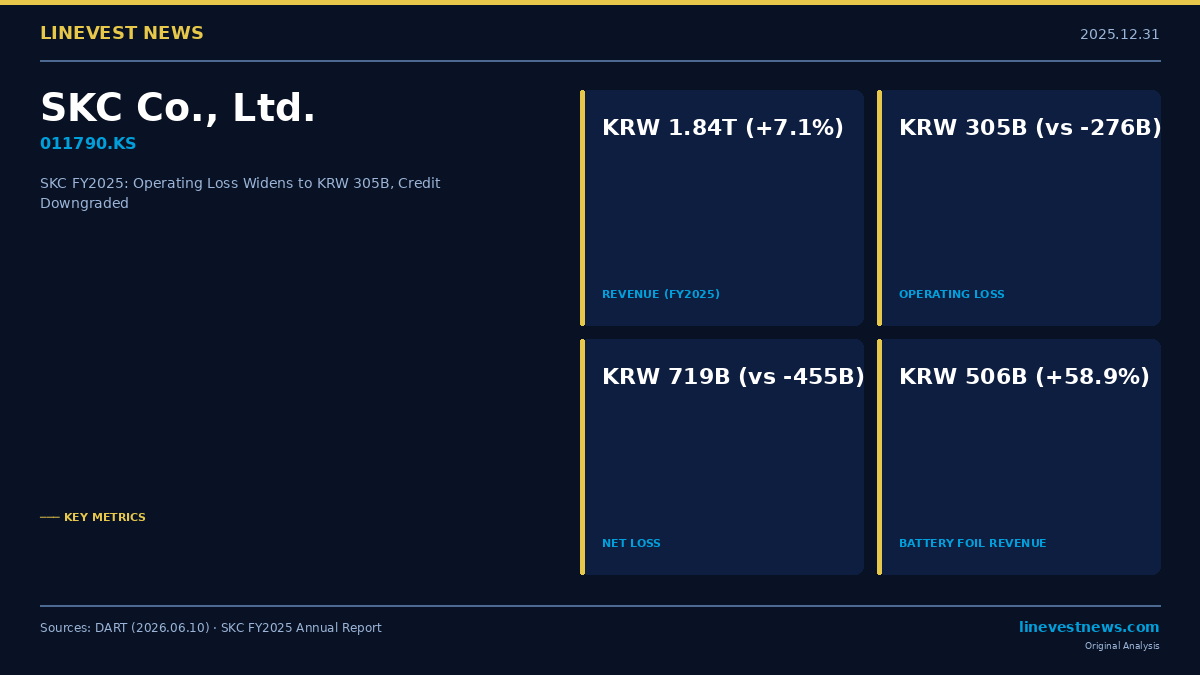

SKC Co., Ltd. (011790.KS) reported a consolidated operating loss of KRW 305.0 billion (USD ~219 million) for fiscal year 2025, widening from a KRW 275.8 billion operating loss in FY2024, even as group revenue climbed 7.1% year-over-year to KRW 1.84 trillion (USD ~1.32 billion). The battery-materials (copper foil) segment surged 58.9%, yet mounting financing costs and large asset write-downs pushed net losses attributable to controlling shareholders to KRW 734.4 billion—nearly double the KRW 443.5 billion recorded in 2024. Two domestic rating agencies downgraded SKC's corporate bonds from A+ to A0 by year-end, reflecting sustained balance-sheet pressure.

Revenue and Segment Performance

SKC's consolidated net revenue rose to KRW 1.840 trillion in FY2025 from KRW 1.718 trillion in FY2024 (+7.1%), driven entirely by the battery-materials segment. The copper-foil (전지박) unit—which supplies lithium-ion battery manufacturers—saw revenue jump to KRW 505.9 billion from KRW 318.3 billion (+58.9%), benefiting from capacity ramp-ups at overseas plants.

In contrast, the core chemicals segment (PO/PG/SM products) slipped to KRW 1.091 trillion from KRW 1.191 trillion (−8.4%), weighed down by weaker polyol and propylene-oxide spreads across Asia. The semiconductor materials segment grew modestly to KRW 220.4 billion from KRW 206.0 billion (+7.0%), supported by demand for silicon rubber sockets and probe cards.

| Segment | FY2025 Revenue | FY2024 Revenue | Change |

|---|---|---|---|

| Chemicals | KRW 1,091B | KRW 1,191B | −8.4% |

| Battery Materials (Copper Foil) | KRW 506B | KRW 318B | +58.9% |

| Semiconductor Materials | KRW 220B | KRW 206B | +7.0% |

| Total | KRW 1,840B | KRW 1,718B | +7.1% |

Operating and Net Losses

Despite higher revenues, the gross margin remained negative for the third consecutive year. Cost of goods sold of KRW 1.859 trillion exceeded revenues, producing a gross deficit of KRW 19.1 billion. Combined with KRW 285.9 billion in selling, general and administrative expenses, the group posted an operating loss of KRW 305.0 billion in FY2025—wider than KRW 275.8 billion in FY2024 and KRW 213.0 billion in FY2023, a three-year trend of compounding operating deficits.

Below the operating line, financing costs totaled KRW 267.5 billion against KRW 87.2 billion in interest income—a net funding drain of KRW 180.3 billion. Additional impairments and other non-operating charges of KRW 396.0 billion (vs. KRW 117.1 billion in 2024) drove pre-tax losses to KRW 899.0 billion. After a KRW 136.0 billion profit from discontinued operations—primarily proceeds from subsidiary disposals—the net loss reached KRW 719.4 billion (vs. KRW 455.1 billion in 2024).

The retained-earnings balance flipped to a deficit of KRW 50.6 billion from a positive KRW 685.9 billion in the prior year, erasing accumulated profit and marking a significant deterioration in book equity.

Balance Sheet Pressure

Total consolidated assets stood at KRW 6.740 trillion as of December 31, 2025, broadly flat versus KRW 6.749 trillion a year earlier. However, total liabilities expanded to KRW 4.715 trillion from KRW 4.456 trillion, pushing the implied debt-to-equity ratio to approximately 233%, up from roughly 194% at end-2024. Equity attributable to controlling shareholders shrank to KRW 832.1 billion from KRW 1.172 trillion.

SKC completed several subsidiary disposals during FY2025, reducing its consolidated entity count from 22 to 16, aiming to improve liquidity and focus the portfolio. Cash and cash equivalents nearly doubled to KRW 783.3 billion from KRW 403.6 billion, partly reflecting asset-disposal proceeds.

Credit-Rating Downgrades

Rating pressure materialized in the second half of 2025. Korea Ratings downgraded SKC's corporate bond to A0 from A+ in June 2025, while also cutting commercial paper from A2+ to A2. NICE Ratings and KIS Ratings followed with downgrades to A2 on commercial paper by December 2025. At year-end, two of three major domestic agencies held SKC bonds at A0, reflecting the three-year streak of operating losses and a sharply diminished equity base.

Dividends and Capital Management

No dividends were paid for the third consecutive year (FY2023, FY2024, FY2025). The company did not issue new equity during FY2025. Management has flagged asset rationalization and portfolio restructuring as the primary levers for financial recovery.

Outlook

SKC's recovery path depends heavily on whether the copper-foil segment can reach profitability as volumes scale. Global battery-industry dynamics—including EV demand normalization and sustained pricing pressure from Chinese competitors—remain headwinds for copper-foil economics. The chemicals segment faces persistent petrochemical spread compression in Asia. Without a return to operating profitability, further credit-rating pressure or potential equity dilution remains a risk.

Sources: SKC Annual Report FY2025 (DART, filed 2026.06.10), SKC FY2025 Consolidated Financial Statements.