Hanwha Stakes Out a Second-Largest Seat at KAI's Table

Hanwha Group has crossed a threshold that no Korean conglomerate has managed before: becoming the second-largest shareholder in Korea Aerospace Industries (KAI, 047810.KS), positioning its aerospace flagship as the country's closest answer to the vertically integrated space giants now reshaping global defense markets.

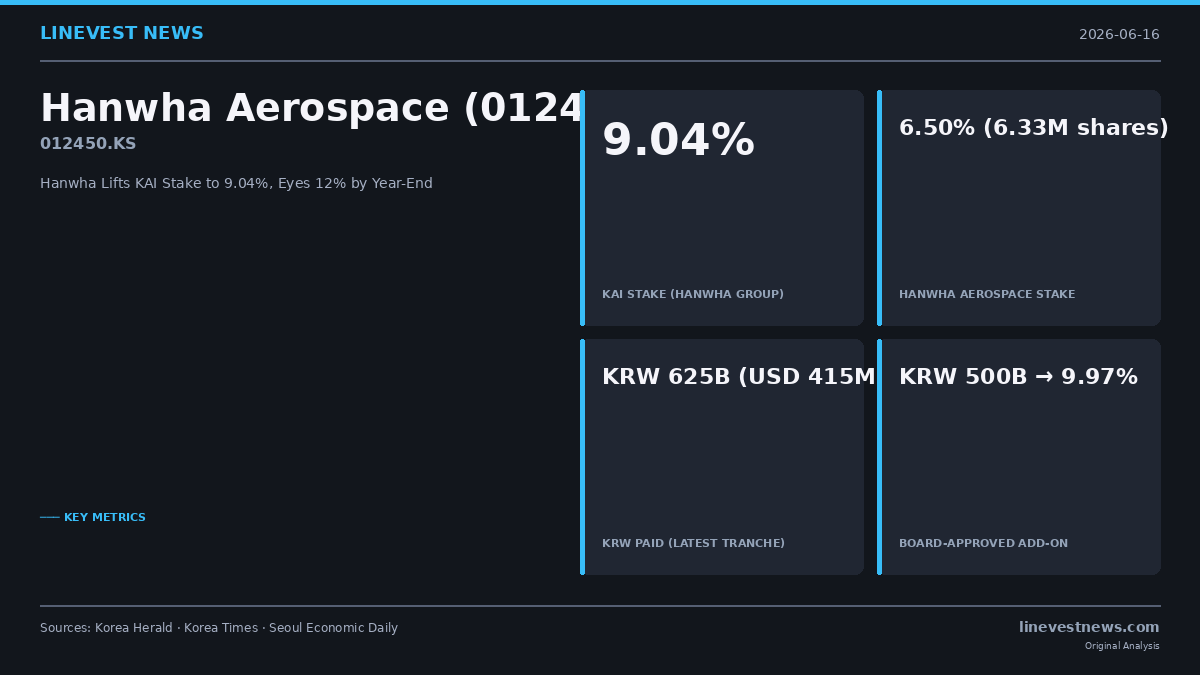

Through a three-entity structure, Hanwha Group now controls 9.04 percent of KAI. Hanwha Aerospace (012450.KS) spent KRW 499.9 billion (approximately USD 332 million) to buy 3.02 million shares, lifting its individual stake to 6.50 percent, or 6.33 million shares. Hanwha Systems (272210.KS) separately deployed KRW 125 billion to raise its holding to 1.53 percent. Hanwha Aerospace USA contributes the remaining 1.01 percent. The Export-Import Bank of Korea retains the top spot at 26.41 percent.

The June 16 closing also came with a mandate for more. Hanwha Aerospace's board has approved a further KRW 500 billion investment designed to carry the company's individual stake to 9.97 percent. With affiliates, the group is targeting more than 12 percent ownership before December 31.

From "Simple Investment" to Management Participation

The shift from passive holding to strategic control is underscored by a regulatory reclassification Hanwha made in May: it moved its KAI position from "simple investment" to "management participation," the designation that allows board representation and strategic coordination. That single filing was the clearest signal yet that Hanwha is no longer treating KAI as a portfolio asset.

Management is explicit about the endgame. "The combination of Hanwha and KAI would enable the creation of the largest domestic space industry value chain, connecting everything from launch vehicles to satellites, ground systems, and space services," the company said. The language mirrors the integration playbook that SpaceX has written in the United States—an observation that Hanwha has leaned into publicly.

The industrial rationale has weight. Hanwha Aerospace brings more than 30 years of experience in aircraft engines, space propulsion, satellites, and radar systems. KAI contributes the airframe, fighter-jet development rights, and the licensed manufacturing relationships with global original equipment manufacturers. Neither company alone can offer what global customers increasingly expect: a single-vendor package spanning munitions, platforms, propulsion, and surveillance.

A Costly Conviction

What unsettles equity investors is the pace and scale of Hanwha's capital deployment. The KAI tranches alone total roughly KRW 625 billion in the most recent round, with another KRW 500 billion queued up. That follows Hanwha Aerospace's KRW 1.3 trillion purchase of a stake in Hanwha Ocean last year—a figure that consumed approximately 94.5 percent of the company's cash reserves at the time—and the KRW 2.3 trillion rights offering launched in 2025 to help recapitalize the balance sheet.

The market's response to the June 16 announcement has been unambiguous. Hanwha Aerospace stock fell 6.48 percent on June 21, extending a decline that has now erased roughly 8 percent from the share price since the deal was disclosed. The stock had reached an intraday peak near KRW 1,224,000 on June 17 before selling resumed. KAI itself has underperformed: the stock traded near KRW 145,100–155,600 in mid-June against a month-to-date loss of 9.34 percent, as KAI shareholders worry about the terms of any eventual tender offer.

Analyst coverage, however, remains constructive. Hyundai Motor Securities set a KRW 1.78 million target for Hanwha Aerospace, citing Poland, the United States, and broader NATO-linked order momentum. The current correction is framed as technical profit-taking rather than a fundamental reassessment of the defense thesis.

The Privatization Question

With Hanwha approaching 10 percent individually and the group converging on 12 percent, a formal privatization scenario edges into range. The EXIM Bank's 26.41 percent creates a natural ceiling for the moment—any attempt to dislodge the state lender would require government consent and potentially a public tender. But the reclassification to "management participation" means Hanwha already has standing to propose board seats and strategic initiatives without waiting for a majority stake.

Korea's government space budget stands at roughly KRW 1.12 trillion annually—modest relative to the ambitions of the industry Hanwha is trying to build. Private capital filling that gap has historically been scarce. If Hanwha succeeds in integrating KAI's platform capabilities with its own propulsion and satellite assets, the resulting entity would have a claim to being the region's most complete aerospace company, and a credible export partner for the growing number of countries that want the entire stack rather than individual components.

Whether the market re-rates that story before the next tranche closes is the more immediate question for Hanwha Aerospace shareholders.

Sources: Korea Herald, Korea Times, Seoul Economic Daily, Asia Business Daily, AJU Press