AI Server Boom Pushes Samsung Electro-Mechanics to Uncharted Price Territory

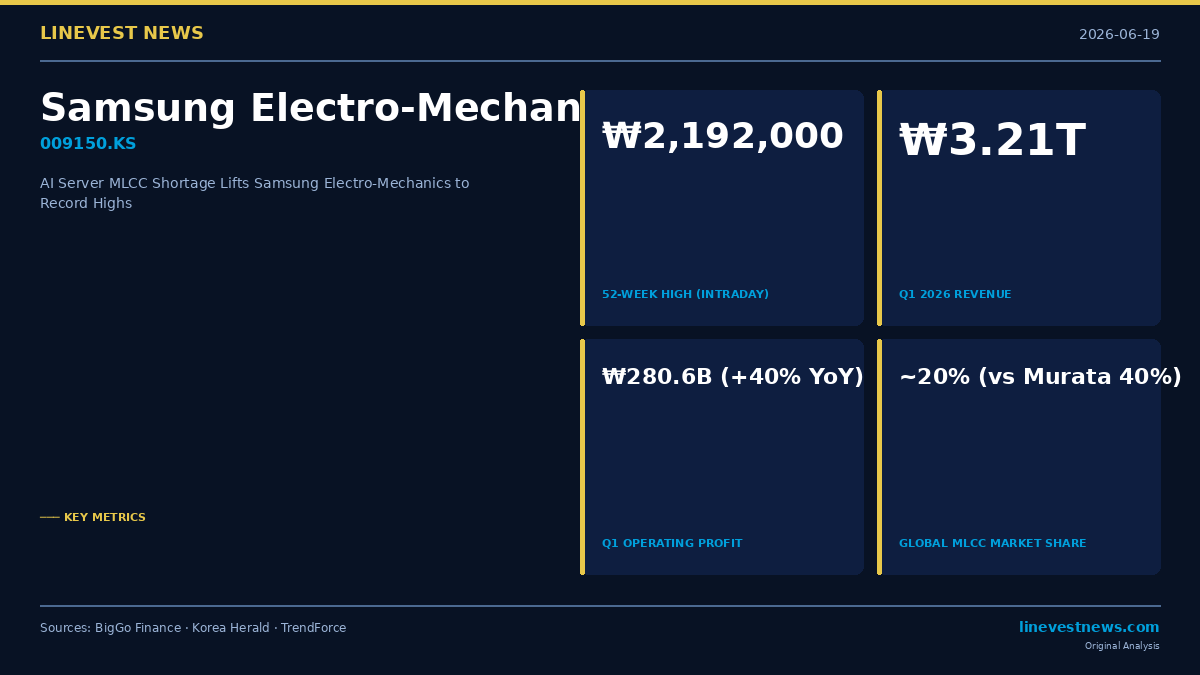

Samsung Electro-Mechanics (009150.KS) pushed to a new 52-week intraday high of ₩2,192,000 on Thursday, extending a historic rally that has seen the KOSPI-listed component maker surge more than 15-fold from the bottom of its annual range as a single structural shift — the explosive MLCC appetite of AI servers — rewrites the economics of the passive-components industry.

Part A — Key Numbers

| Metric | Value |

|---|---|

| 52-Week Intraday High | ₩2,192,000 |

| Q1 2026 Revenue | ₩3.21 trillion (~USD 2.1B) |

| Q1 2026 Operating Profit | ₩280.6 billion (+40% YoY) |

| Global MLCC Market Share | ~20% (vs Murata ~40%) |

| Silicon Capacitor Contract | ₩1.6 trillion (undisclosed global client) |

Why AI Servers Change Everything for MLCC Makers

A general-purpose server deployed five years ago consumed roughly 2,200 multilayer ceramic capacitors (MLCCs). A rack-level AI accelerator built around NVIDIA's latest GB300 platform demands approximately 28,000 MLCCs — nearly 13 times more per unit. Expressed as a ratio to smartphones, the gap runs 10–20 times wider once power-delivery requirements are factored in, according to Korea Herald analysis.

The numbers matter because only two companies in the world can today manufacture the high-capacitance, ultra-thin-dielectric MLCCs that AI infrastructure requires at scale: Japan's Murata Manufacturing, with roughly 40% of the global market, and Samsung Electro-Mechanics, at approximately 20%. Chinese capacitor producers that have undercut pricing in consumer-grade MLCCs remain years away from meeting AI-grade specifications — estimates from analysts range from five to eight years — leaving Samsung as the sole credible second source for hyperscalers hedging concentration risk on Murata.

The Price-Hike Cycle Widens the Profit Pool

That supply concentration is now translating directly into margins. Murata announced price increases of 15–35% effective April 1, 2026, on AI server components, citing rising silver costs and tightening capacity. Samsung Electro-Mechanics has moved in tandem: NH Investment & Securities estimates Samsung's MLCC average selling price will rise roughly 5.4% in 2026 and a further 9.6% in 2027, with AI-grade components commanding two to three times the average selling price of standard IT-grade MLCCs.

The company's component division is forecast to reach a 14.8% operating margin in 2026 and 16.7% in 2027, according to NH Investment (March 2026). Q1 2026 already showed the trajectory: operating profit of ₩280.6 billion grew 40% year-on-year, even as Murata's Q1 operating profit grew 73% — a gap analysts attribute to Murata's larger installed AI-customer base rather than any Samsung quality differential.

A ₩1.6 Trillion Wild Card

Alongside MLCC momentum, Samsung Electro-Mechanics disclosed — without naming the counterparty — a ₩1.6 trillion silicon capacitor contract with a major global technology company. Silicon capacitors occupy a smaller niche than MLCCs but carry higher gross margins and target the same AI-server power-delivery circuits. The contract is seen by analysts as evidence that Samsung is expanding its passive-component addressable market beyond ceramics as AI infrastructure spending scales through 2027.

Murata Rises in Parallel, Narrowing the Valuation Gap

The competitive dynamic is unusual: Samsung's rally has been so steep that it now commands a forward price-to-earnings ratio of roughly 90x, compared with Murata's approximately 60x, and a price-to-book ratio of 14.8x against Murata's 6.4x. Rather than dragging on sentiment, Murata's own surge of 12.73% on May 29 — briefly topping ¥10,000 intraday — was read by the market as confirmation that AI-server MLCC demand is structural, lifting both players simultaneously.

Consensus target prices for Samsung Electro-Mechanics span ₩1.79–2.3 million, with Hyundai Motor Securities and Daol Investment & Securities both citing ₩2.3 million.

Manufacturing Constraints Entrench the Duopoly

Production of high-end MLCCs requires barium titanate powder as a dielectric material; Samsung manufactures it in-house, a vertical-integration advantage that competitors relying on outside suppliers cannot easily replicate. New production lines start at efficiency rates of 40–60% of standard MLCC lines, and yield rates on leading-edge specifications can open below 10%, with mature lines struggling to sustain 60–70%. These constraints mean that even if demand softens cyclically, capacity additions will remain controlled — a dynamic that supports elevated pricing through at least 2027.

*Sources: BigGo Finance (May 29, 2026 rally data), Korea Herald (AI server bottleneck analysis), TrendForce (Samsung MLCC price hike, Feb 2026), NH Investment & Securities research (March 2026).*