Washington is moving to eliminate the separate regulatory step that for years has held biosimilar drugs below their brand-name counterparts in U.S. pharmacy systems. The bipartisan Biosimilar Red Tape Elimination Act (S.1954) would automatically deem every FDA-approved biosimilar interchangeable with its reference biologic — removing a hurdle that, supporters note, exists nowhere else in the world. For Korea's two global biosimilar leaders, Celltrion and Samsung Bioepis, the shift could cut development costs by as much as 90% and accelerate product launches by years.

What the Regulatory Shift Means

Under current U.S. law, a biosimilar cannot be substituted at the pharmacy counter without a physician's explicit approval unless it has earned a separate FDA "interchangeable" designation — a status that requires additional switching studies beyond the standard biosimilar approval. S.1954, introduced in the Senate in June 2025 by Senators Mike Lee (R-UT), Rand Paul (R-KY), Ben Ray Luján (D-NM), and Margaret Wood Hassan (D-NH), would presume that every FDA-approved biosimilar is automatically interchangeable, aligning U.S. policy with scientific consensus and the regulatory frameworks used by the European Medicines Agency.

The FDA is advancing in parallel. Commissioner Marty Makary pledged to finalize draft guidance in the first half of 2026, merging biosimilarity and interchangeability into a single streamlined review. A March 2026 FDA draft already allows Phase 3 clinical trial requirements to be waived "when scientifically justified." Canada's health regulator followed on May 19, eliminating comparative clinical efficacy study requirements when analytical data suffice. Korea's own Ministry of Food and Drug Safety is cutting its biosimilar review timeline from 420 to 240 days, effective next month.

Korean Companies at the Top of the Stack

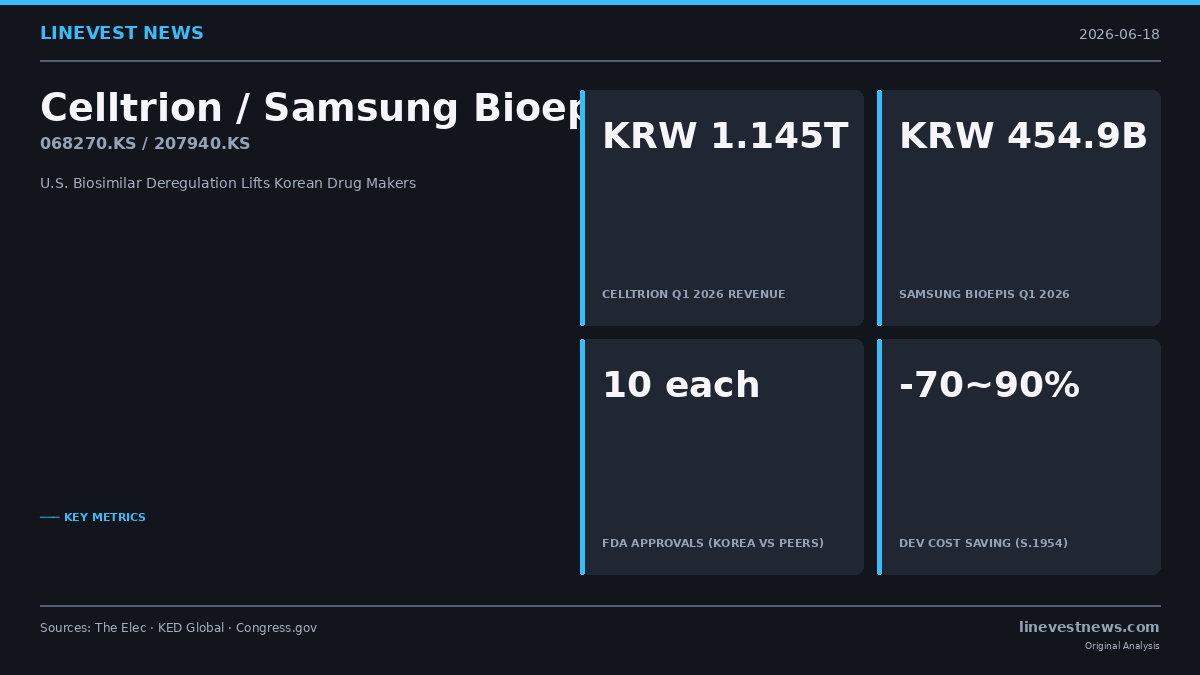

The regulatory wave comes as Celltrion and Samsung Bioepis have quietly accumulated the world's deepest FDA-approved antibody biosimilar portfolios. Each holds 10 FDA-approved antibody biosimilars, surpassing Amgen (8 approvals) and Sandoz (7 approvals), and 11 European approvals apiece — ahead of Sandoz's 8 and Amgen's 5. Since the U.S. and European markets represent roughly 80% of global biosimilar demand, the two Korean companies are better positioned than any rival to exploit interchangeability reform at scale.

Speed is another structural advantage. Both Celltrion and Samsung Bioepis completed Humira biosimilar clinical trials in 17 months, versus 26 months for Sandoz. Under the proposed framework, that execution edge translates directly into more simultaneous product launches.

The Economics of Deregulation

Industry estimates place the cost savings at 70–90% per product. Samsung Bioepis has disclosed that U.S. development expenses for a single program could fall by approximately USD 225 million under the new framework, while clinical timelines compress by one to two years. Multiplied across a pipeline targeting 20 biosimilar products by 2030, the cumulative savings are substantial.

Financial Momentum Already Building

Both companies posted strong first-quarter 2026 results, even before the deregulation finalization. Celltrion reported Q1 revenue of KRW 1.145 trillion (approx. USD 828 million), with operating profit of KRW 321.9 billion. New biosimilar products accounted for KRW 581.2 billion — more than 60% of total product sales — reflecting the company's successful U.S. market penetration.

Samsung Bioepis recorded Q1 revenue of KRW 454.9 billion (approx. USD 329 million), with an operating profit of KRW 144 billion and an operating margin above 30%. The company has announced plans to add six new biosimilars to its pipeline and reach 20 total products by 2030.

Celltrion is also set for a major U.S. launch: following a patent settlement with Regeneron, the company plans to bring its aflibercept biosimilar (targeting blockbuster eye drug Eylea) to the U.S. market in December 2026.

Competitive Pressure From India

The global biosimilar market is projected at approximately USD 320 billion over the next decade, drawing aggressive M&A from rivals. Indian generic giant Sun Pharma's USD 11.75 billion acquisition of Organon's biosimilar division illustrates the pace of consolidation. For Celltrion and Samsung Bioepis, the deregulation tailwind provides a window to entrench their U.S. and European positions ahead of an intensifying competitive wave.

Sources: The Elec (thelec.net), KED Global, Biosimilars Research & Reports, Congress.gov (S.1954 text), FiercePharma (Celltrion-Regeneron settlement), Pearce IP (Samsung Bioepis pipeline), ETNews