Korean banks carry the largest single slice of credit risk from the court-rehabilitation filing by JoongAng Group, one of South Korea's biggest media-and-entertainment conglomerates — but brokerage estimates of the resulting hit suggest it is unlikely to dent the sector's record second-quarter earnings.

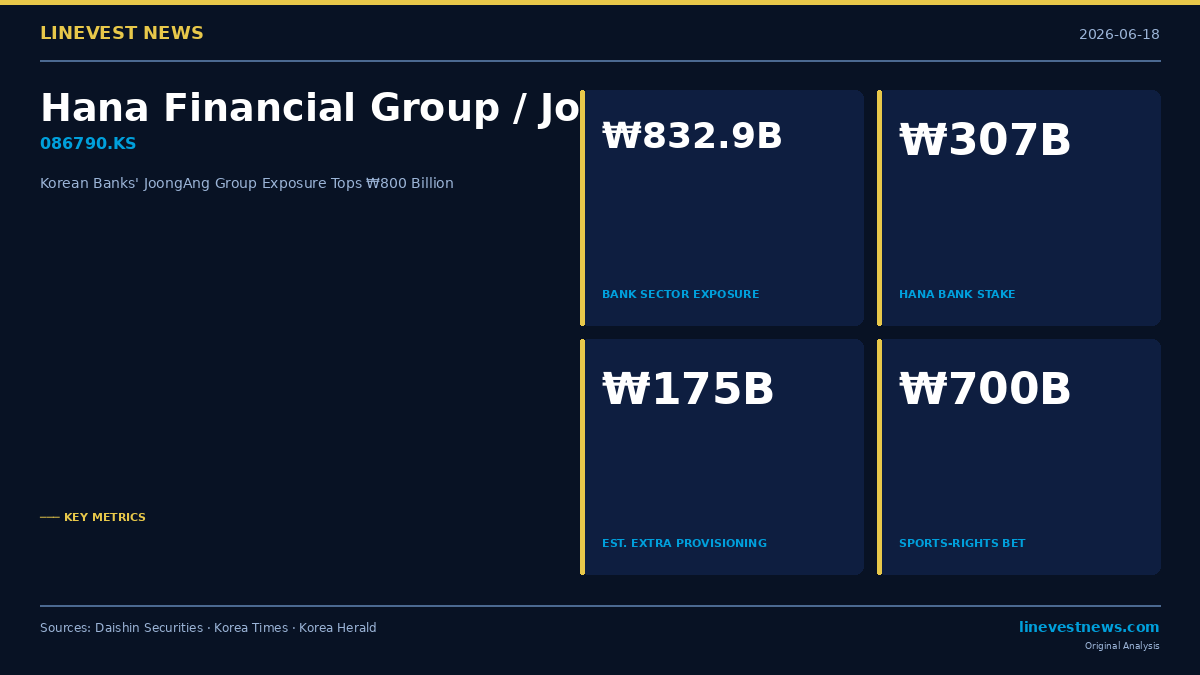

Daishin Securities, a Seoul-based brokerage, tallied the borrowings of JoongAng Group's major affiliates at ₩2.74 trillion ($2.0 billion) as of June 13, split between roughly ₩1.23 trillion ($898 million) in bank and other loan claims and about ₩1.5 trillion ($1.1 billion) in market-raised funds such as corporate bonds. Of that, banks hold the most exposure at ₩832.9 billion ($608 million), ahead of special financial institutions at ₩164.2 billion ($120 million), securities firms at ₩125.1 billion ($91 million) and specialized-credit (capital) firms at ₩79.7 billion ($58 million), according to industry tallies reported by Korean financial media.

What triggered it

The crisis crystallized on June 12, when JTBC — JoongAng's flagship cable broadcaster — failed to repay ₩20.6 billion ($15 million) of maturing securitized borrowings, a default that pushed five group entities into court protection. JoongAng Holdings (the group's holding company), Contentree JoongAng (its content-production arm), Megabox JoongAng (its cinema chain) and JoongAng P&I filed for rehabilitation with the Seoul Bankruptcy Court on June 14, with JTBC following on June 15, while the flagship newspaper JoongAng Ilbo is pursuing a separate creditor-led workout, per the Korea Times, Korea Herald and Daishin.

The Korea Times reported the group's distress stems from roughly $500 million (about ₩700 billion at the time) committed for rights to broadcast the Olympics from 2026 through 2032 and the FIFA World Cup through 2030, after sublicensing talks with terrestrial broadcasters KBS, MBC and SBS deadlocked and television ad revenue declined.

Sizing the hit

Daishin estimates industry-wide provisioning of about ₩175 billion ($128 million). Across the four commercial banks it covers, loans to the group total roughly ₩450 billion ($328 million), with Hana Bank — JoongAng's main transaction bank — carrying the heaviest load at ₩307 billion ($224 million). Affiliate-level disclosures compiled by Insight Korea corroborate Hana's lead, citing ₩140 billion in real-estate-backed loans to JoongAng Holdings and a ₩100 billion loan to Contentree JoongAng maturing in May 2027.

The cushion is collateral. Daishin analyst Park Hye-jin estimated that more than 90% of the bank loans are secured and were classified as normal credit before the default; with credit ratings now cut to "D," she expects banks to reclassify the loans conservatively as "substandard or below" (Korea's 고정이하 category, which forces higher reserves). Even so, Park projected only modest incremental provisions — about ₩30 billion ($22 million) at Hana, ₩10 billion ($7.3 million) at Woori, and roughly ₩5 billion ($3.6 million) each at KB and Shinhan. She also flagged that JoongAng's planned ₩550 billion ($401 million) headquarters sale could allow recovery of the secured loans and a partial reversal of those reserves, since most of the covered banks' lending is collateralized by that building.

A familiar pattern

Korea's financial regulators are reviewing whether retail corporate-bond sales were mis-sold, Daishin noted, though Park argued the impact should be limited because recording and investor sign-offs became mandatory after consumer-protection rules were tightened. The reference point is 2013, when Tongyang Group defaulted on more than ₩100 billion and filed for receivership of three subsidiaries; its sale of ₩156.9 billion in asset-backed commercial paper to tens of thousands of retail investors triggered a mis-selling scandal, compensation claims and the arrest of its chairman in January 2014, according to the Korea Times and public records.

Reporting an observation rather than a recommendation: Daishin maintained a positive stance on bank stocks, noting that lenders are likely to post strong second-quarter results while trading below a price-to-book ratio (a valuation gauge comparing share price to net assets) of 1.0, with Hana Financial Group (086790.KS) at about 0.8 and Shinhan Financial Group (055550.KS) named as preferences.

What to watch

The confirming data point arrives with the banks' second-quarter earnings releases in July, when actual provisioning against JoongAng exposure — and any guidance on the headquarters-sale recovery — will show whether the "limited impact" thesis holds. The pace of the Seoul Bankruptcy Court's rehabilitation process and the financial regulator's mis-selling review are the other near-term swing factors.

This article is for informational purposes only and does not constitute investment advice. Figures are sourced from Daishin Securities, the Korea Times, the Korea Herald, Korean financial media (EBN), Insight Korea and public records as cited; currency conversions use an approximate rate of 1 USD = 1,370 KRW and are indicative only.