Hanwha Engine's Q1 2026 results reflect operating cash flow of ₩48.4 billion, free cash flow of ₩23.5 billion, and a ₩5.17 trillion order backlog providing two to three years of production visibility at current run rates; the 14.9% operating margin and positive free cash flow should be treated as the baseline assumptions in near-term financial models.

Cash Flow

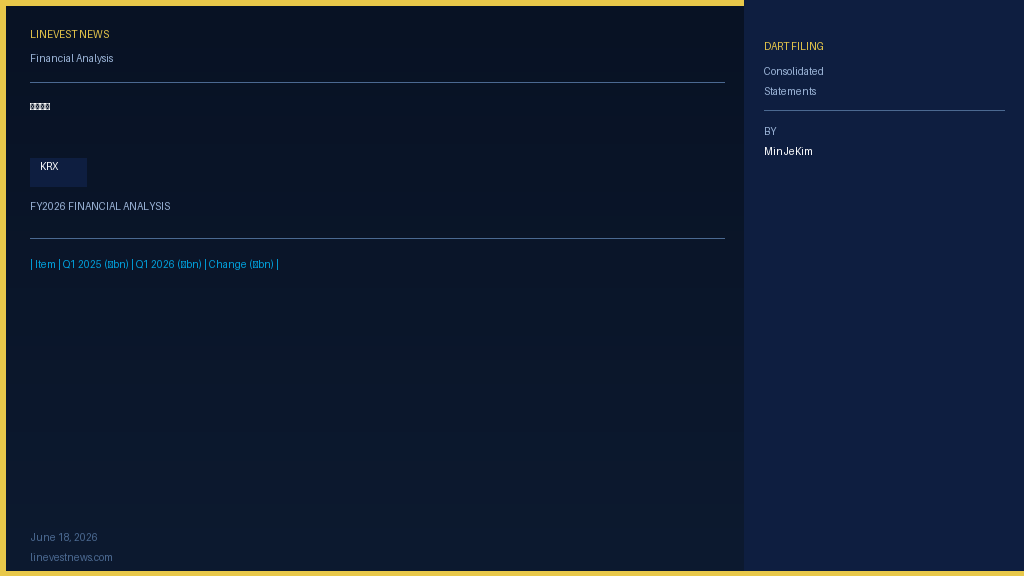

| Item | Q1 2025 (₩bn) | Q1 2026 (₩bn) | Change (₩bn) |

|---|---|---|---|

| Operating cash flow | 46.1 | 48.4 | +2.3 |

| Investing cash flow | -65.6 | -265.4 | -199.8 |

| Financing cash flow | +9.4 | -1.0 | -10.4 |

| Net change in cash | — | -218.0 | — |

| Ending cash balance | 123.2 | 50.0 | — |

Earnings quality and working capital

Operating cash flow of ₩48.4 billion against net income of ₩52.9 billion yields a cash conversion ratio of 0.91, indicating high earnings quality with minimal accruals-based inflation of profits. Working capital consumed ₩21.0 billion in cash (versus a ₩17.4 billion source in Q1 2025), as rising inventories and receivables absorbed cash. This reversal is the expected pattern for a capital goods manufacturer accelerating production throughput in an upturn — more steel and components arriving ahead of delivery, more billings outstanding on work nearing completion.