Part A — What Happened

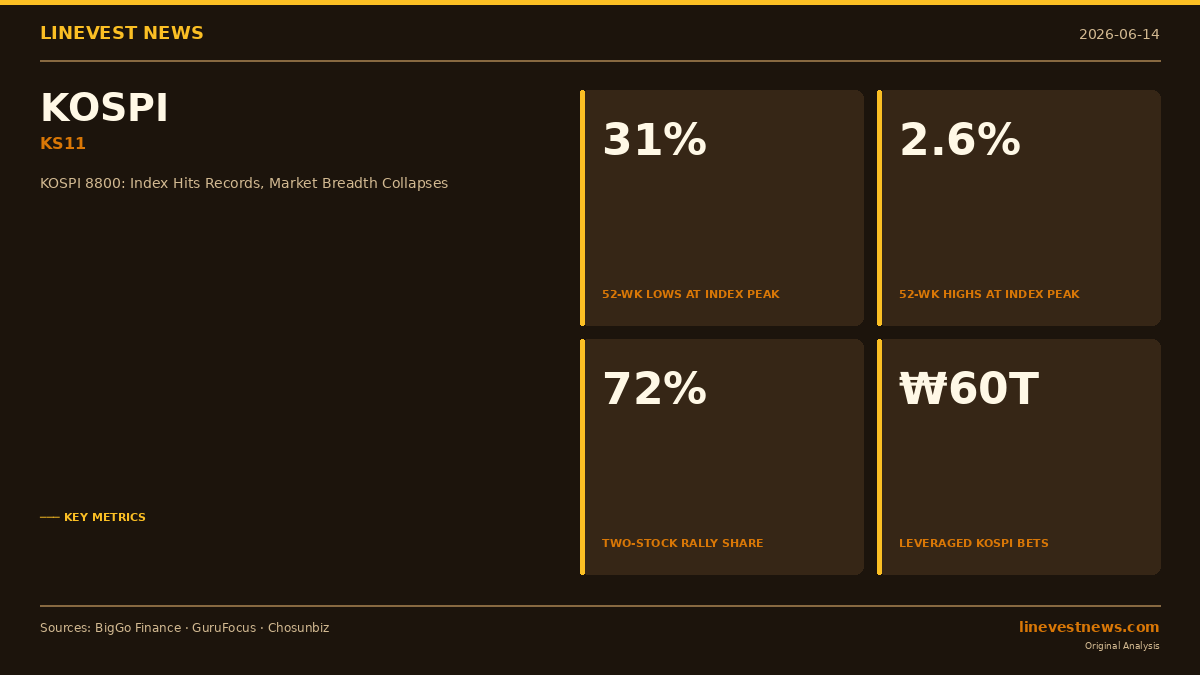

South Korea's benchmark KOSPI index has climbed roughly 109% over the past six months, breaching the 8,000 mark for the first time on May 15 before reaching 8,801 in June 2026. Yet beneath this headline euphoria, a stark structural crack has opened: when the index hit its peak, only 2.6% of listed stocks reached 52-week highs, while 31% fell to 52-week lows — a breadth divergence that market participants in Seoul now call the "K-shaped market."

The rally is almost entirely the story of two companies. Samsung Electronics (005930.KS) and SK Hynix (000660.KS) together account for 72% of the KOSPI's year-to-date gains and 54% of total market capitalisation, according to data compiled by BigGo Finance. On any given day during the six-session surge that lifted the index 12.15%, at least 70% of constituent stocks declined.

A June 5 circuit breaker — triggered when the index dropped 6.4% in a single session — offered a brief preview of what happens when the two-stock engine stalls. The moment amplified the structural fragility that breadth indicators had been flagging for weeks.

Part B — Why It Matters

Leverage is the accelerant. Outstanding leveraged stock investments in South Korea reached ₩60 trillion (~USD 39.3 billion) at end-May, with more than 350,000 retail accounts enrolled in double-leveraged ETFs tracking Samsung and SK Hynix. Margin growth in Korea expanded 72.5% in 2025. The concentration of borrowed money in two securities creates a reflexive dynamic: a chip rally forces leveraged buyers to add exposure, which further concentrates the market; a chip sell-off forces margin calls that amplify the decline with no diversified cushion.

"Cash buffers are shrinking while active leverage refuses to unwind. This means leverage pressure is intensifying," said Shawn Oh, a strategist at NH Investment Securities. Kenny Kim of Meridian One Asset Management added that "negative gamma effects dominate within leveraged ETFs, forcing aggressive buying in rallies but dumping stocks during falls."

Foreign capital has been a net seller. Despite the index gains, foreign investors sold a net ₩130 trillion (~USD 85.2 billion) since November, according to BigGo Finance data. The recent rebound in foreign buying — ₩111 trillion (~USD 72.7 billion) in new inflows from January to May 2026 — remains concentrated in the same two chip leaders, leaving the breadth problem unresolved.

A rate-hike test looms. The Bank of Korea is expected to raise its policy rate in July, which could compress the earnings multiples that make the current concentration tenable. Ha Seok-keun of Eugene Asset Management warned: "I expect a period of heightened volatility and correction over the next one to two months." Goldman Sachs raised its KOSPI target to 12,000 — implying roughly 37% upside from current levels — but even that bullish call is predicated on sustained AI-driven semiconductor demand rather than a broadening of the rally to mid- and small-cap stocks.

For investors tracking the KOSPI as a gauge of Korean corporate health broadly, the index number tells only half the story. The other half — 31% of stocks at new lows, daily breadth negative while the headline number soars — is the half that tends to matter when the chips run hot and cold at the same time.

Sources: BigGo Finance, GuruFocus (KOSPI Historical Data), en.sedaily.com, Chosunbiz