China's two largest memory-chip makers are advancing toward public listings just as a global, AI-driven memory upcycle fattens their balance sheets — putting fresh competitive pressure on Samsung Electronics (005930.KS), the world's largest memory-chip maker, and SK hynix (000660.KS), the world's second-largest.

For a portfolio manager watching the DRAM and NAND complex, the question is not whether China is entering memory — it already has — but how close it is to contesting Korea's lead, and in which segments.

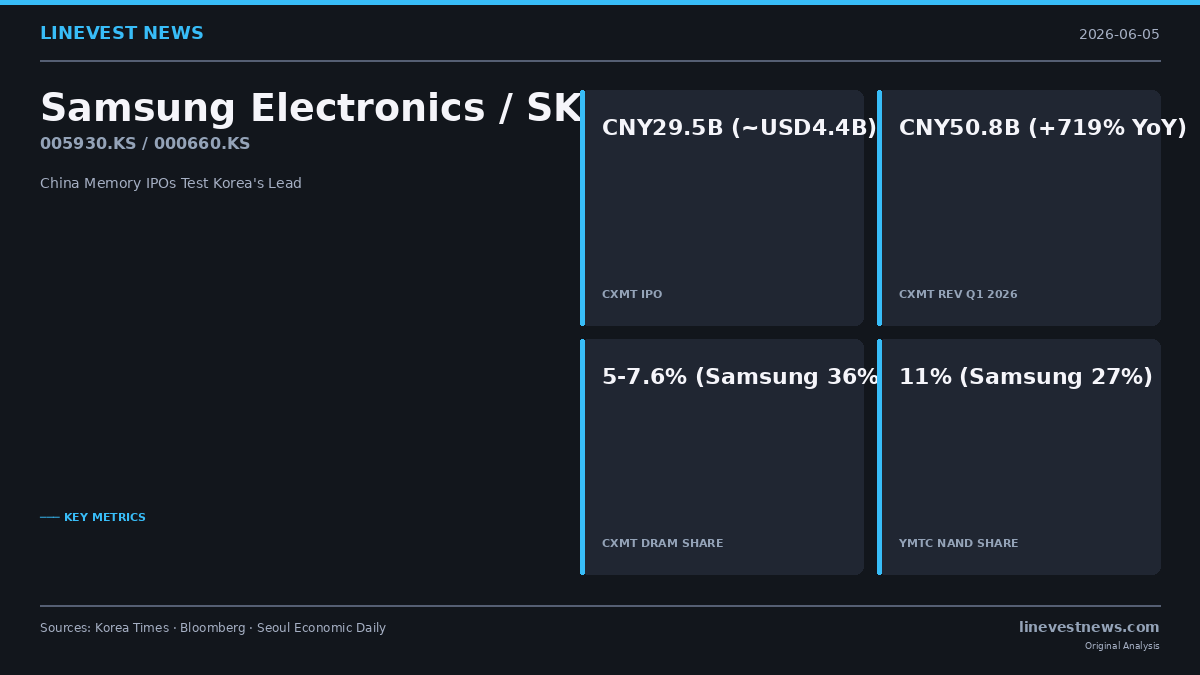

What just happened

ChangXin Memory Technologies (CXMT), China's leading producer of dynamic random-access memory (DRAM), won approval last week for an initial public offering of nearly 30 billion yuan ($4.4 billion) on the Shanghai STAR Market, China's Nasdaq-style board for technology firms, according to The Korea Times. Bloomberg reports the deal — sized at about 29.5 billion yuan — is on track to be mainland China's largest IPO since 2022, and could exceed $5 billion with an over-allotment option.

Separately, Yangtze Memory Technologies Corp. (YMTC), China's top maker of NAND flash storage, has begun IPO preparations and could formally file as early as June, with proceeds earmarked for equipment and research and development, The Korea Times reported. YMTC is bringing a new Wuhan production line online in the second half of 2026.

The cash is arriving as both firms ride a memory boom: CXMT posted first-quarter 2026 revenue of 50.8 billion yuan (about $7 billion), up roughly 719% year-on-year, per The Korea Times.

Sizing the gap

The IPOs fund expansion, but the market-share distance remains wide. In DRAM, CXMT held about 5% of the global market in the fourth quarter of 2025, up from 4% a year earlier, against Samsung's 36% and SK hynix's 32%, according to figures cited by The Korea Times. (Seoul Economic Daily, citing the IPO review, puts CXMT's DRAM share higher at roughly 7.6% (up from 3.9% two quarters earlier) — a discrepancy that reflects differing measurement windows and methodologies.) Combined, the two Korean firms still command more than two-thirds of the DRAM market.

The NAND picture shows faster Chinese gains. YMTC's share rose to 11% in the fourth quarter of 2025 from 8% in the first quarter of the same year, narrowing the distance to Samsung's 27% and SK hynix's 22%, per The Korea Times.

The timeline question

Market share understates the remaining technology gap. Chinese memory makers are "still a few years behind," analyst Ray Wang told The Korea Times, estimating YMTC is roughly two years behind in NAND, CXMT around three years behind in commodity DRAM, and roughly four years behind in high-bandwidth memory (HBM) — the segment that drives AI-server demand and commands the richest margins for Samsung and SK hynix.

That lead is where the Korean incumbents have concentrated, and it is the buffer the China challenge is testing.

A precedent worth remembering

Korea has watched a Chinese catch-up curve flatten its lead before. In display panels, BOE Technology, China's largest panel maker, overtook LG Display in 2018 to become the world's largest supplier of LCD TV and monitor panels, according to shipment data from Sigmaintell reported by DigiTimes and GSMArena — ending more than a decade of Korean leadership in the segment. Samsung Display and LG Display subsequently wound down commodity LCD output and retreated to higher-value OLED. Memory is a more capital- and IP-intensive business than LCDs, and the analogy is imperfect, but the pattern — Chinese state-backed scale eroding a commodity tier first — is the one Korean executives know well.

What to watch next

The near-term confirming data points are concrete: whether YMTC files its listing application in June as flagged; CXMT's eventual Shanghai trading debut and final raise; and the next quarterly DRAM and NAND share readings, which will show whether China's gains are accelerating or plateauing. On the Korean side, Samsung is pressing ahead with capacity of its own — construction has resumed on its fifth Pyeongtaek plant (P5), with mass production targeted for 2028, according to Newsis. Whether that capacity lands in advanced AI memory or commodity tiers will shape how directly it meets the Chinese build-out.

This article is for informational purposes only and does not constitute investment advice. Figures are sourced from the publications cited inline and were accurate as of publication; readers should verify current data before making any decision.

Sources: www.koreatimes.co.kr, www.bloomberg.com, en.sedaily.com, www.digitimes.com, www.gsmarena.com, www.newsis.com