South Korea's petrochemical producers staged their best quarter in years between January and March, but the recovery rests on a foundation the industry itself expects to crumble in the second half: a war-driven spike in product prices that is now unwinding.

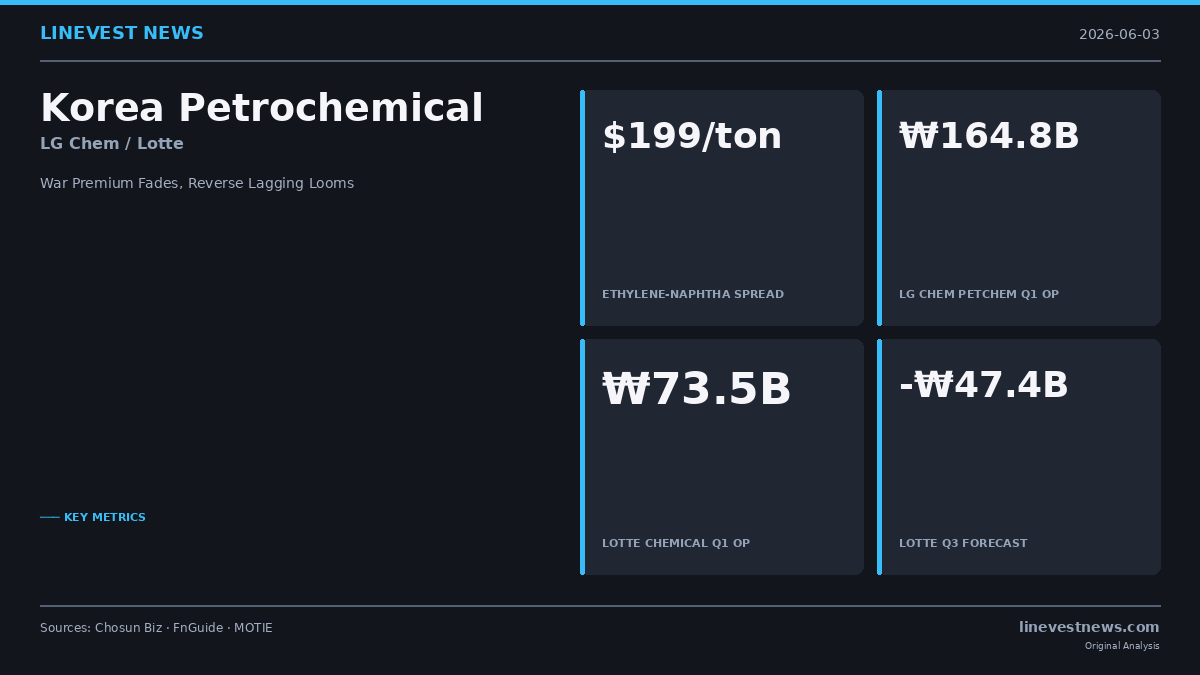

The single most-watched gauge tells the story. The ethylene-to-naphtha spread — the gap between the price of ethylene (the key product) and naphtha (the feedstock), and the standard proxy for Korean cracker profitability — stood at just under $200 per ton in late May — roughly $960 for ethylene against about $761 for naphtha — according to statistics from MOTIE (Korea's Ministry of Trade, Industry and Energy) cited by Chosun Biz. The industry typically pegs breakeven at around $250 per ton for integrated producers and $300 to $350 for non-integrated producers, per S&P Global Platts. That means current margins are sitting well below the level at which producers earn a normal return on their core product.

That is a steep descent from April, when the spread briefly cleared $500 per ton. The surge followed the blockade of the Strait of Hormuz during the U.S.-Iran conflict, which sent crude and downstream petrochemical prices sharply higher. Korean producers, holding naphtha bought earlier at lower prices, captured an outsized 'lagging effect' — the timing gap between buying feedstock and selling finished product — as selling prices ran ahead of input costs.

How good Q1 actually was

The lagging tailwind produced a clean sweep of upside surprises. Lotte Chemical (011170.KS), Korea's largest petrochemical maker by capacity, posted Q1 operating profit of ₩73.5 billion ($54 million) — its first profit in 10 quarters, reversing a loss streak running back to 2023. The result beat a market consensus that had expected a roughly ₩20.3 billion loss, according to ICIS and Seoul Economic Daily. The basic chemicals division alone swung to a ₩45.5 billion profit on feedstock-cost benefits of about ₩250 billion quarter-over-quarter, the company said on its Q1 earnings call.

The pattern repeated across the sector, per Chosun Biz: LG Chem's (051910.KS) petrochemical division earned ₩164.8 billion ($120 million), while the chemical units of Hanwha Solutions and SKC posted ₩34.1 billion ($25 million) and ₩9.6 billion ($7 million) respectively.

Why the second half looks different

The mechanism that lifted Q1 runs in reverse when prices fall — what the industry calls 'reverse lagging.' Producers are now feeding crackers with the relatively expensive naphtha secured during the wartime price spike; if crude and product prices soften from here, those high-cost inputs collide with weaker selling prices and margins compress, Chosun Biz reported.

The sell-side has begun pricing that in. Financial-data provider FnGuide projects Lotte Chemical will swing to an operating loss of ₩47.4 billion ($35 million) in the third quarter and post a further ₩40 billion ($29 million) loss in the fourth, according to figures cited by Chosun Biz. An industry official quoted in the report said the war-driven improvement "is likely to end in the second quarter," with reverse lagging and Chinese oversupply expected to drag results back down in the second half.

That Chinese oversupply is the structural overhang behind the cyclical one. Global ethylene capacity expanded by roughly 45 million tons between 2020 and 2024, of which China accounted for about 25 million tons, per Chosun Biz — figures broadly consistent with industry estimates from Wood Mackenzie and ICIS, which put global additions over 2020-2025 at more than 40 million tons with the bulk built in China — a flood of low-cost supply that has kept Korean producers in the red for several years.

The restructuring that isn't happening fast enough

Korea's policy answer is supply discipline, but it is stalling. The government has called for cutting 18-25% of national NCC (naphtha cracking center) capacity — up to 3.7 million tons, equivalent to roughly a quarter of the country's total, a target confirmed by The Korea Times and KED Global. Yet the improved Q1 numbers have made producers more reluctant to shutter plants, and disputes persist over S-Oil's Shaheen project in the Ulsan industrial complex, a Saudi Aramco-backed facility due to begin commercial operation in the second half of 2026 that will add about 1.8 million tons of annual ethylene capacity — partly offsetting the planned cuts once it comes online.

The data point to watch

The confirming signal is near. Q2 earnings, due in late July, should reveal whether the war premium was a one-quarter event, as the industry itself expects, or whether spreads can hold near breakeven. If the ethylene-naphtha spread stays at or below the $200 line through the summer, the FnGuide loss forecasts for the back half move from projection toward base case. The slower-moving question is whether the restructuring drive can regain momentum once the temporary profits fade — or whether recovery, paradoxically, is what keeps too much capacity online.

This article is for informational purposes only and does not constitute investment advice. Figures are sourced from Chosun Biz, MOTIE statistics, ICIS, S&P Global, Wood Mackenzie, Seoul Economic Daily, The Korea Herald, The Korea Times, and KED Global as cited above. Currency conversions use an approximate rate of 1 USD = 1,370 KRW.

Sources:

- https://biz.chosun.com/industry/company/2026/06/04/LCVAG7T7DVCJ5DYCAJM77GPUL4/

- https://www.icis.com/explore/resources/news/2026/05/12/11206470/s-korea-s-lotte-chemical-returns-to-net-profit-in-q1-on-improved-spreads/

- https://en.sedaily.com/business/2026/05/12/lotte-chemical-returns-to-profit-brokerages-raise-target

- https://www.digitaltoday.co.kr/en/view/54407/lotte-chemical-q1-operating-profit-73-5-billion-won-swing-to-profit

- https://www.koreatimes.co.kr/business/companies/20251222/petrochemical-firms-to-cut-37-mil-tons-in-ncc-capacity-through-restructuring-minister

- https://www.kedglobal.com/corporate-restructuring/newsView/ked202508200005

- https://www.koreaherald.com/article/10598721

- https://www.spglobal.com/energy/en/news-research/latest-news/refined-products/122225-commodities-2026-asian-naphtha-faces-challenges-amid-petrochemical-restructuring-russian-supply-uncertainty