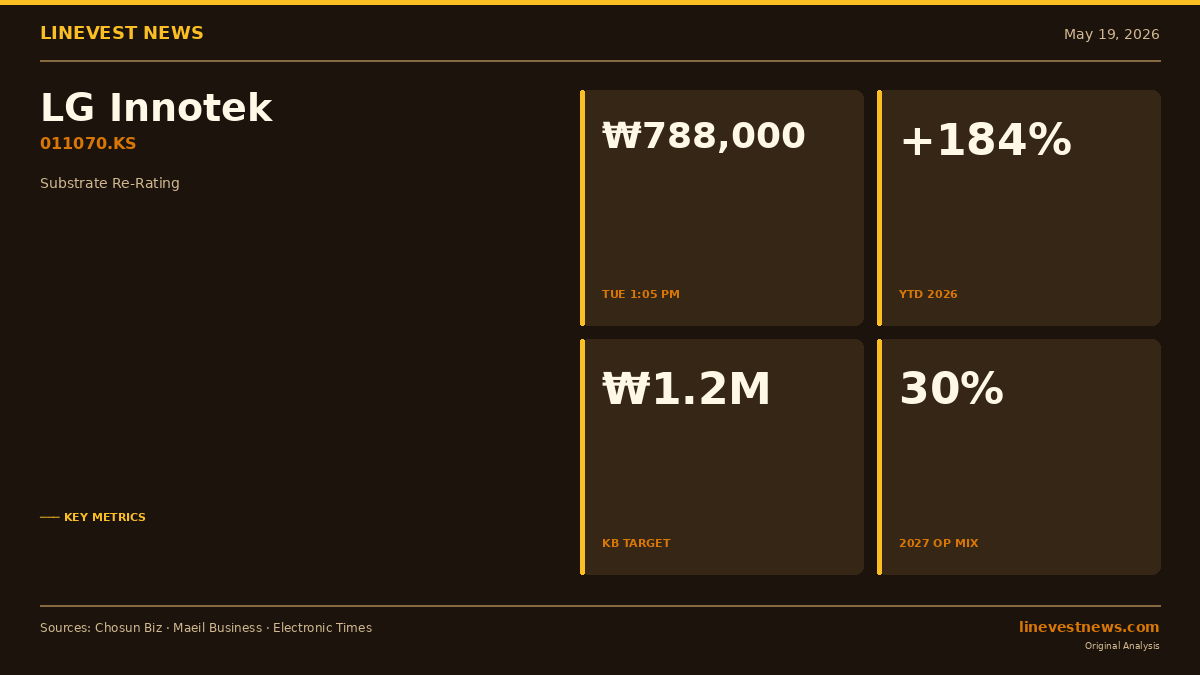

SEOUL, May 19, 2026 — Shares of LG Innotek (011070.KS), the LG Group electronic-components affiliate that supplies camera modules and package substrates, jumped as much as 6.71% to ₩811,000 ($592) in early Tuesday trading on the KOSPI (Korea's main equity index) before paring gains to ₩788,000 ($575), up 3.68%, by 1:05 p.m. local time, according to Chosun Biz (a Korean financial news outlet) and Electronic Times (a Korean tech and industry daily). The move came after KB Securities (a Korean brokerage house) lifted its target price to ₩1,200,000 ($876) from ₩950,000 ($693), and NH Investment & Securities (the brokerage arm of Korea's NongHyup financial group) raised its target the prior day to ₩1,000,000 ($730) from ₩700,000 ($511).

The analyst actions matter because the stock is already up 184% year-to-date in 2026, per Maeil Business Newspaper (a Korean financial daily) — the obvious question is whether the substrate-business earnings math actually supports another re-rating from here, or whether brokers are chasing the tape.

The substrate math behind the upgrade

Kim Dong-won, head of research at KB Securities, framed the call around a sharp divergence between revenue mix and profit mix. The substrate business accounts for just 8% of LG Innotek's total revenue, but its contribution to consolidated operating profit is projected to climb from 11% in 2024 to 19% in 2025, 21% in 2026, and 30% in 2027, according to KB's note cited by Chosun Biz and Electronic Times.

The driver is product mix. Kim said large-area, high-multilayer substrates aimed at AI data center customers carry average selling prices more than 50% above the company's existing substrate products — a category that, until recently, was a much smaller share of orders. KB's argument is essentially that substrates are becoming LG Innotek's second growth engine after optical (camera) solutions.

For a senior portfolio manager, the testable element is the 2025 step from 11% to 19% operating-profit contribution. That is the data point that has to land in upcoming quarterly results for the 2026 and 2027 path to remain credible.

Why the long-term-contract signal is unusual

NH Investment & Securities analyst Hwang Ji-hyun argued in a separate note, cited by Chosun Biz, that a substrate shortage is now spreading across the industry, with customers offering capex support and pushing for long-term supply agreements with manufacturers. Maeil Business Newspaper described this as substrates entering a "long-term contract era" similar to the one memory chips moved into earlier — a reference to multi-year supply pacts that have become common in high-bandwidth memory.

That structural read-across is what is pushing brokers off historical mid-cycle multiples. If buyers are willing to pre-fund capacity, suppliers can extend the revenue visibility window beyond the usual one- to two-quarter book-to-bill horizon, which typically warrants a higher multiple — though whether LG Innotek itself has signed such a contract has not been disclosed in the cited reports.

What to watch next

The immediate checkpoint is LG Innotek's next quarterly disclosure on Korea's DART (the electronic disclosure system run by the Financial Supervisory Service), where the substrate segment's contribution to consolidated operating profit will be visible. KB's 2025 contribution forecast of 19%, up from 11% in 2024, is the figure that either validates or undercuts the broader 30%-by-2027 path.

A second checkpoint is whether either LG Innotek or peers disclose specific long-term substrate supply agreements with named AI accelerator or hyperscaler customers — the kind of contract Hwang and Maeil Business Newspaper flagged as the emerging industry norm. Without a disclosed contract, the "long-term era" thesis remains an industry directional view rather than a name-specific catalyst.

KB's new ₩1,200,000 ($876) target implies further upside versus Tuesday afternoon's ₩788,000 ($575), but the run that has already happened — 184% year-to-date per Maeil Business Newspaper — means subsequent quarters need to physically deliver the profit-mix shift KB is modeling.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. Figures cited are sourced from Korean-language press reports referenced above; readers should consult primary disclosures and qualified advisors before making any investment decision. USD conversions use an approximate rate of 1 USD = 1,370 KRW.