What just happened

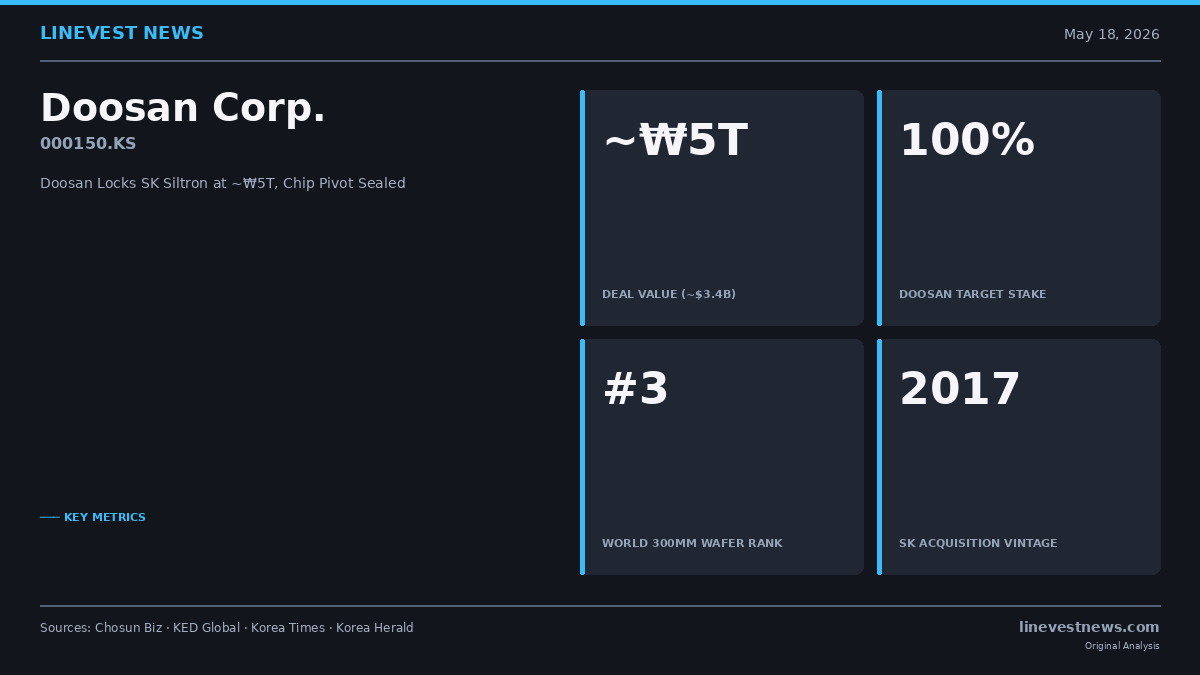

Doosan Corp. (000150.KS), the holding company of Korea's Doosan Group, is set to sign a share purchase agreement (SPA) this week to acquire SK Siltron, the country's only domestic silicon-wafer maker, according to a Chosun Biz report citing investment banking sources (Chosun Biz, May 18, 2026). The first-stage SPA covers the 70.6% block held by SK Inc. — a 51% direct stake plus a 19.6% interest tied to a total return swap (TRS). Doosan is then expected to acquire the remaining 29.4% held personally by SK Group Chairman Chey Tae-won in a separate transaction before year-end, taking it to 100% ownership.

Reported deal value sits at roughly ₩5 trillion ($3.4 billion at ~1,470 KRW/USD), per the same Chosun Biz piece. KED Global has put the full-company valuation slightly higher at ~₩5.5 trillion ($3.7 billion) (KED Global, May 17, 2026).

The question on the buy side: is ~₩5 trillion the right number?

The most useful price anchor is what SK itself paid in 2017, when it bought the same 70.6% block (51% from LG + 19.6% from a financial investor) out of LG Group for about ₩790 billion, while Chey took the other 29.4% personally (Chosun Biz, May 18, 2026). On a like-for-like 70.6% basis, Doosan is paying roughly six times what SK paid nine years ago for the controlling block — a markup that reflects both the post-2020 reset in wafer pricing and SK Siltron's expansion into silicon carbide (SiC).

The equity check, however, is smaller than the headline implies. Negotiators have valued SK Siltron at around ₩5 trillion on an enterprise basis, with net equity at roughly ₩1.5 trillion after about ₩3 trillion of debt is stripped out (KED Global, December 17, 2025). In plain terms, Doosan is buying a balance sheet that already carries the build-out of new SiC and 300mm capacity — which is both why the multiple looks rich on earnings and why the equity bill is more digestible than the ₩5 trillion sticker.

Against current trading: SK Siltron reported ₩2.08 trillion ($1.41 billion) of revenue and ₩407 billion ($277 million) of operating profit in 2025, with the SiC wafer business booking a roughly ₩400 billion impairment loss in the FY2025 annual report released March 31, 2026 (The Korea Times, April 13, 2026). That puts the implied enterprise value at roughly 12 times trailing operating profit — a level that only works if the SiC swing-to-profit lands.

What Doosan actually gets

SK Siltron is described as the world's third-largest player in 300mm (12-inch) silicon wafers across the deal coverage (Chosun Biz, May 18, 2026; The Korea Herald). It employs about 3,600 people, including roughly 2,500 production workers, and draws more than 50% of its sales from Samsung Electronics (005930.KS) and SK hynix (000660.KS) (The Korea Times, April 13, 2026).

That customer base is the strategic prize. Inside SK Group, SK Siltron's natural ceiling has been its perceived alignment with SK hynix; non-SK customers — including foundries that compete with hynix's memory partners — have an obvious reason to diversify suppliers. Removing the SK badge gives the wafer business room to deepen ties with Samsung Foundry and overseas logic customers without intra-group conflicts. The same Korea Times piece quotes an analyst projecting Doosan's electronics unit could see "a 14 percent year-on-year increase in revenue and a 28 percent rise in operating profit this year" once consolidation effects flow through.

The SiC business is the other lever. SK Siltron's US subsidiary secured a $544 million loan from the US Department of Energy to expand silicon-carbide wafer manufacturing in Michigan (KED Global, May 17, 2026). The Michigan ramp, originally aimed at EV power-semiconductor customers, becomes a Doosan asset on day one of closing.

For Doosan, this slots a front-end materials business on top of a portfolio that already includes Doosan Tesna (acquired 2022) in back-end semiconductor testing and the copper clad laminate (CCL) line inside Doosan's electronics business group (Chosun Biz, May 18, 2026). By KED Global's framing, the deal would "recast the South Korean conglomerate around semiconductors" by adding one of the world's largest wafer makers to Doosan's existing chip materials, substrate and testing businesses (KED Global, May 17, 2026).

Why SK is selling

The sale fits a pattern. SK Inc., the group holding company, divested its 85% stake in SK Specialty (industrial gases) to a private equity buyer for ₩2.6 trillion ($1.77 billion) in March 2025 (The Korea Times, April 13, 2026). The proceeds, together with what SK now realizes from SK Siltron, are being funneled into the group's AI and core-semiconductor bets — chiefly SK hynix's HBM expansion. Selling the captive wafer arm also resolves the customer-conflict point flagged above and lets SK redeploy capital out of a capital-intensive materials business that booked a roughly ₩400 billion SiC impairment in its FY2025 results.

The financial-pressure question

A ₩5-trillion deal is meaningful for Doosan Corp. by any measure. Chosun Biz, in the same article that broke the SPA timing, names debt-load management as the central task Doosan will have to solve after signing. Doosan has not disclosed its funding structure for the transaction; how much equity, how much new debt, and what role any partner co-investors take are open variables that will shape the next-12-month credit picture.

What to watch next

- SPA signing this week. The Chosun Biz reporting points to an SPA on SK Inc.'s 70.6% block within days; the precise headline number and financing structure will be the first hard data point (Chosun Biz, May 18, 2026).

- Chairman Chey's 29.4%. The personal stake transfer is described as a separate, later step targeted for completion within 2026; pricing on that tranche will tell investors whether it tracks the SK Inc. block or carries a premium.

- Korea Fair Trade Commission (KFTC) review. Any deal of this scale in the Korean chip supply chain typically draws an antitrust filing; the KFTC's timing has historically run 60–120 days for non-horizontal combinations.

- SiC profitability path. With a roughly ₩400 billion SiC impairment recognized in FY2025, the swing point on the Michigan ramp is the single biggest swing factor in whether Doosan's purchase multiple holds up.

This article is for informational purposes only and does not constitute investment advice. Figures and source attributions reflect reporting available as of May 18, 2026.

Sources

- Chosun Biz — Doosan, SK Siltron SPA timing and Chey personal-stake plan, May 18, 2026

- KED Global — Doosan recast around semiconductors, SiC Michigan loan, May 17, 2026

- KED Global — SK Siltron enterprise vs equity valuation framing, Dec 17, 2025

- Korea Herald — SK Siltron world-#3 300mm wafer ranking

- Korea Times — SK Siltron FY2025 financials, customer mix and SiC impairment, Apr 13, 2026