KB Financial Group (105560.KS), Korea's largest banking holding company by assets, said on May 17 that it has completed an end-to-end technical verification of a Korean won stablecoin covering offline payment, settlement and cross-border remittance, working with payment processor KG Inicis, the Kaia Layer-1 blockchain, and digital-asset infrastructure firm OpenAsset (News1; Newdaily).

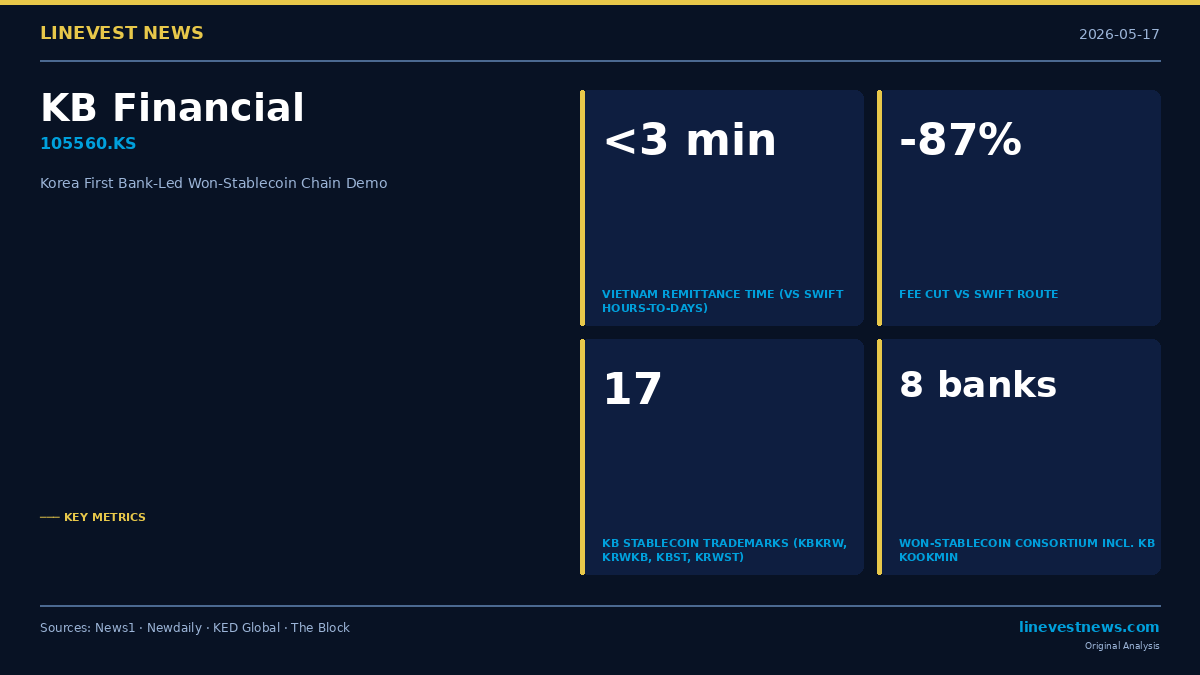

The proof-of-concept tied two scenarios into a single flow. At a Hollys Coffee kiosk — the offline test bed run on the franchise operated by KG-affiliated Hollys F&B — a customer paid by scanning a QR code, with smart contracts handling settlement automatically and no separate digital wallet required (News1). The merchant-side won stablecoin was then converted to a dollar stablecoin using Kaia's on-chain liquidity and pushed through a Vietnamese partner into a recipient bank account, with the full chain completing in under three minutes versus the hours-to-days typical of SWIFT, and at fees roughly 87% lower than the SWIFT route (Newdaily; News1).

The question that matters

For a global investor, the obvious question is whether this is a launch in waiting or a lab exercise that cannot ship. KB's own framing is unambiguous on that point: a company representative said the bank wants to "combine verified stability and trust-based financial infrastructure with blockchain technology to deliver user-centric digital financial services" once virtual-asset rules are formalized, and the group plans to commercialize only after Korea's digital-asset legislation is enacted (News1; Newdaily). In other words, the technology stack is now demonstrated; the gating item is statute, not engineering.

How the demo differs from prior pilots

What sets the May 17 verification apart from earlier domestic experiments is the integration. Korean banks have run isolated stablecoin demos before — KB itself completed a separate proof-of-concept in April with blockchain-infrastructure firm Suho IO that tested stablecoin-to-dollar foreign-exchange settlement and automatic execution of transaction conditions (Seoul Economic Daily) — and a regional-bank consortium led by iM Bank with fintech Finger and post-quantum-security vendor BTQ ran a separate KRW stablecoin proof-of-concept on Kaia's mainnet (Crypto Times). The KB-led test announced on May 17 is the first by a major Korean banking group to chain merchant payment, settlement and overseas remittance into one user journey, according to the two Korean reports describing the verification (News1; Newdaily).

The Vietnam corridor was not chosen at random. A separate Korea-Vietnam stablecoin remittance pilot run earlier in 2026 by the Kaia DLT Foundation with a domestic financial institution cut the cost of sending 100,000 won by 87% versus conventional channels while compressing transfer time to under three minutes — the same headline figures KB is now reporting under its own brand, suggesting the underlying rail is shared (Seoulz).

KB's wider stablecoin posture

The pilot lands inside a broader push that has been visible in trademark and consortium filings for months. KB Kookmin is one of eight Korean banks preparing a joint won-stablecoin issuance vehicle (Seoulz), and the bank has filed 17 stablecoin-related trademark applications with KIPRIS including KBKRW, KRWKB, KBST and KRWST (The Block). KB has separately deepened ties with Circle, the U.S. issuer of USDC, in an arrangement aimed at exploring USDC adoption and won-stablecoin development (CryptoNews). Read together, the May 17 announcement is less a one-off demo than the visible surface of a multi-track strategy spanning domestic issuance, dollar-stablecoin interoperability and remittance-corridor monetization.

The partners chosen reinforce that read. Kaia, an EVM-compatible Layer-1, has positioned itself as the "default chain" for a won stablecoin and earlier announced a strategic partnership with OpenAsset to develop a KRW-pegged stablecoin ecosystem (Ainvest). KG Inicis, one of Korea's leading payment-gateway operators and the parent of Hollys F&B since its 2020 acquisition through a special-purpose vehicle (Crown F&B) (Wikipedia: KG Group), supplies both the checkout rail and a captive offline merchant network through the coffee chain.

What an investor should watch next

Because commercial launch is explicitly contingent on legislation, the binding catalyst is the Digital Asset Basic Act and any subsidiary rules on bank ownership of won-stablecoin issuers — an area where Korean policymakers have already signaled an intent to ease ownership limits to allow banks more latitude over issuance vehicles (KED Global). Until that framework lands, the May 17 verification gives KB a working stack it can switch on, but no booked revenue. The narrow data points to track from here are the Korean National Assembly's progress on the digital-asset statute and any disclosure by KB or its consortium peers of a launch date or fee schedule for the won-stablecoin service.

This article is for informational purposes only and does not constitute investment advice. All figures and quotations are attributed to the sources cited inline. Readers should consult primary disclosures and qualified advisers before making any investment decision.