Delivery Hero is moving to offload Baemin — Korea's dominant food delivery app — at an asking price that has reached ₩8 trillion. Three names are already deep in due diligence: Uber, Naver, and Alibaba. The question every institutional investor should be asking is not who buys it, but whether the price makes sense for a food delivery platform operating in a market that has already peaked.

DH's Math vs. the Market's Reality

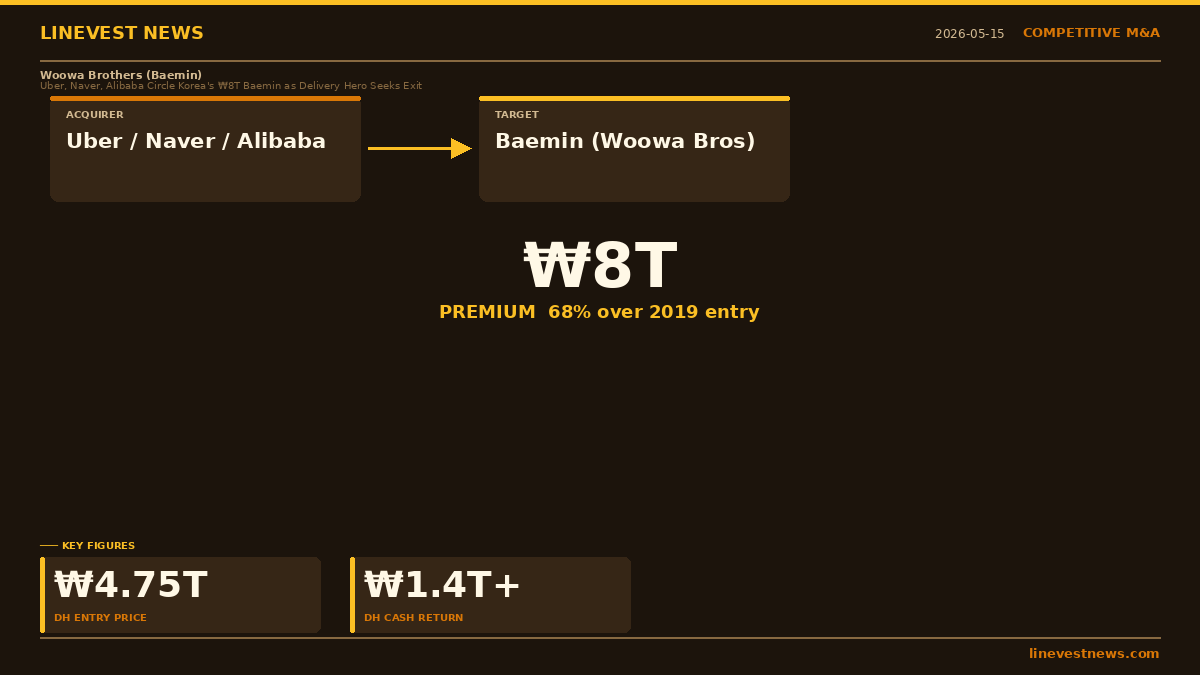

Delivery Hero paid ₩4.75 trillion ($3.4B) for an 87% stake in Woowa Brothers in 2019. In the seven years since, Baemin has functioned as DH's most reliable cash machine — returning over ₩1.4 trillion to the parent through dividends and share buybacks. At ₩8 trillion, DH would walk away with a 68% markup on its original entry. That sounds attractive. The problem is the denominator.

Korea's food delivery market grew at double-digit rates through the pandemic. That era is over. Growth has decelerated sharply, and Baemin has faced sustained political pressure over its delivery commission rates — a structural regulatory risk that is explicitly unresolved. At ₩8 trillion, a buyer is pricing in a return to strong growth that the current regulatory environment does not easily permit.

DH's own motivation here is worth noting. The company announced a strategic portfolio review via shareholder letter in late 2025, appointed JP Morgan as Baemin's sell-side advisor in early 2026, and is now running a restricted competitive bidding process rather than an open auction. That sequence — portfolio review, then a quiet sale process — reads more like a balance sheet-driven exit than a seller confident in timing the market peak.

Uber's Korea Problem — and Why Baemin Solves It

Uber's interest is structurally coherent in a way the others' are not. The company pulled Uber Eats from Korea in 2019, failed to make meaningful inroads against Kakao Mobility's 90%-plus market share in ride-hailing, and has since been in a strategic holding pattern in what is, by consumer spend, one of the highest-value urban mobility markets in Asia.

Buying Baemin would give Uber an immediate #1 position in food delivery. The simultaneous reports that Uber is also exploring a stake in Kakao Mobility — whose primary shareholder TPG is reviewing all exit options including a full sale or a US IPO — suggest Uber is considering a compressed version of the same strategy that drove its global expansion: acquire the market leader, inherit the data, integrate the subscription layer. Korea would become an Uber-adjacent super-app geography rather than a market it competes from a standing start.

The data angle reinforces this. Baemin holds granular order and merchant data for Korea's most urbanized districts. Kakao Mobility holds point-to-point mobility data. Together, they would give Uber an unmatched behavioral dataset for the Korean market.

Uber is also in talks about a consortium with Naver at an estimated 70:30 equity split. Naver's Maps and Commerce products offer complementary distribution, and the consortium structure would reduce the regulatory surface area — a Korean co-investor partially neutralizes the "foreign capital taking over a domestic platform" narrative.

The Regulatory Ceiling

The biggest constraint on any deal is the Korea Fair Trade Commission. KFTC has been tightening its platform and rental-sector merger review standards, and a transaction of this scale — where a foreign entity would acquire effective control of a company with commanding market share in a core consumer service — will face intensive scrutiny regardless of the buyer identity. The Uber-Naver 70:30 split does not necessarily resolve this: KFTC will look at de facto operational control, and a 70% Uber stake makes that reading straightforward.

KFTC review risk is the primary reason the bidder pool is narrow. Alibaba faces an additional layer of political complexity given the current geopolitical climate around Chinese capital in Korean strategic assets. Naver acting alone lacks the financial capacity to comfortably absorb ₩8 trillion without impairing its own balance sheet.

What to Watch

The near-term signal to track is whether a formal data room opens and on what timeline. A restricted process with three named bidders doing active due diligence — some reportedly for the past two months — suggests DH wants to move before any macro or regulatory window closes. The critical test will be whether Uber can build an antitrust clearance strategy credible enough for DH to accept deal-risk in the purchase agreement.

If Uber and Naver reach binding terms, the post-signing regulatory clock in Korea can stretch six to twelve months. DH needs liquidity. That tension — between DH's timeline and KFTC's pace — is likely the real negotiation.

Sources: Chosunbiz (MoneyMove), ETNews, AsiaE (May 15, 2026). This article is for informational purposes only and does not constitute investment advice.