SK Square's Q1 Profit Hits Record ₩8.3T, Lifts Holdco to KOSPI No. 3

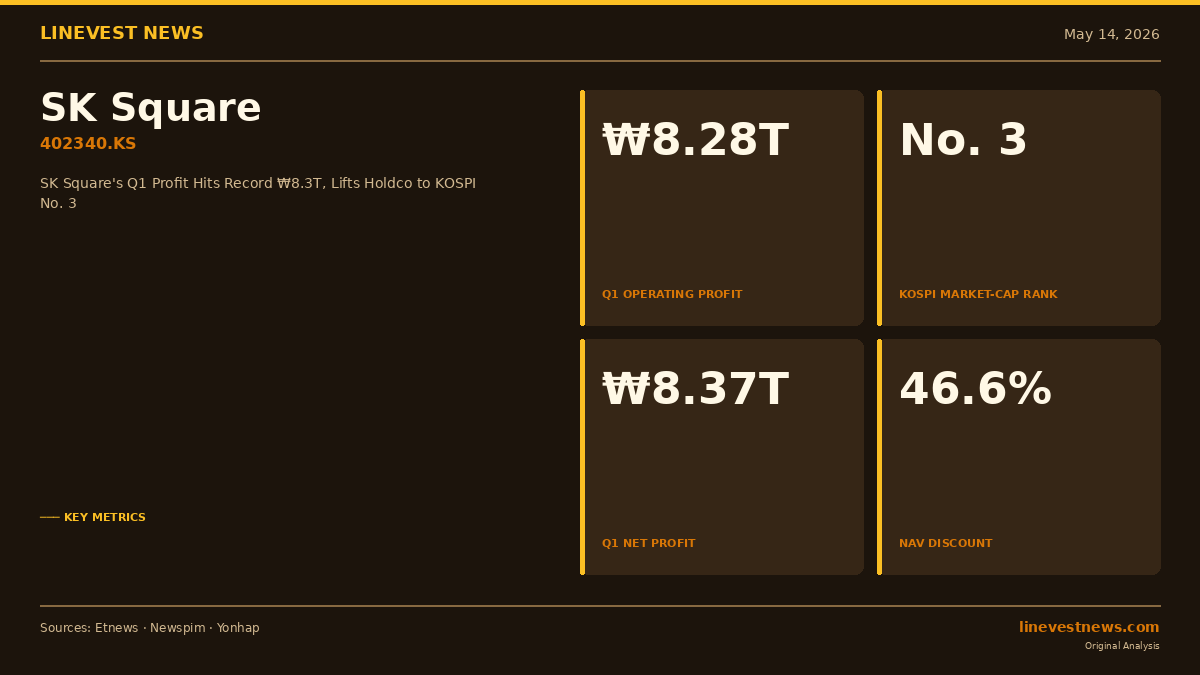

TL;DR - SK Square, the SK Group holdco owning ~20% of SK Hynix, posted record Q1 operating profit of ₩8.28 trillion ($6.04 billion), up 400% YoY. - Market cap reached ~₩157 trillion ($114.6 billion) at the May 13 close, lifting SK Square to KOSPI No. 3 behind Samsung Electronics and SK Hynix. - NAV discount narrowed to 46.6%, from 65.7% at end-2024 — the first concrete signal Korea's chronic holdco discount can compress when the underlying rerates.

Lead

SK Square — the SK Group investment arm spun off from SK Telecom in 2021 and now SK Hynix's largest single shareholder — said on Thursday that its first-quarter operating profit hit a record ₩8.2783 trillion ($6.04 billion), a 400% jump from a year earlier, on the back of equity-method gains from its roughly 20% stake in the memory-chip maker. The print lifted SK Square (402340.KS) into third place by market capitalization on the KOSPI (Korea's main stock exchange), trailing only Samsung Electronics and SK Hynix.

What Happened

In a regulatory filing carried by Etnews and Newspim, SK Square reported Q1 revenue of ₩300.3 billion ($219 million), down 13% year over year, operating profit of ₩8.2783 trillion, and net profit of ₩8.3747 trillion ($6.11 billion), up 419% YoY. The operating-profit line — dominated by SK Hynix equity-method contributions, not fee income — was a quarterly record.

SK Hynix's Q1 2026 results, released in April per PR Newswire, showed revenue of ₩52.58 trillion ($38.4 billion), operating profit of ₩37.61 trillion ($27.5 billion) at a 72% margin, and net profit of ₩40.35 trillion ($29.5 billion). SK Square's share flows through its P&L under Korean equity-method accounting.

Per Newspim, SK Square's market cap stood at ~₩157 trillion ($114.6 billion) at the May 13 close — roughly 15x the ₩10.6 trillion ($7.7 billion) of early January 2025 and triple the early-January 2026 level.

Why It Matters

This is the first concrete signal that Korea's chronic "holdco discount" — the persistent gap between a holding company's market value and the sum of its listed parts — can compress meaningfully when the underlying asset rerates and management commits to capital returns. SK Square's net asset value (NAV) discount, the most-watched metric for Korean holdcos, was 46.6% as of May 13, per company disclosures cited by Newspim, versus 65.7% at end-2024 and 51.5% at end-2025.

That narrowing matters beyond one company. Korea's "value-up" agenda — the Financial Services Commission's (Korea's top financial regulator) push to close the "Korea Discount" — has pressed listed holdcos to lift valuations via buybacks and capital reallocation. SK Square is the cleanest case study yet: a holdco whose discount has nearly halved over 18 months while delivering ROE of 55.1% as of end-March, per the company's filing.

Business Impact

For SK Square, the immediate operating reality is that essentially all reported profit is non-cash equity-method income — useful for headline P&L but not directly available for distribution. Cash returns depend on either SK Hynix dividends flowing up or on monetisation of portfolio holdings.

Etnews reported that SK Square has earmarked ₩310 billion ($226 million) in shareholder returns running through 2026, up from the ₩200 billion ($146 million) in buybacks it executed in 2025. Management framed forward strategy around an "investment–value-up–rebalancing" cycle, with new capital steered toward AI infrastructure and the semiconductor supply chain.

For SK Hynix (000660.KS) minority shareholders, the read-through is indirect: a more highly valued parent is more likely to support — rather than overhang — the chipmaker. SK Hynix's market capitalization crossed ₩1,000 trillion ($730 billion) on May 4 as shares broke ₩1.4 million for the first time, per Seoul Economic Daily.

Industry & Historical Context

SK Square was carved out of SK Telecom in 2021 to unlock the Hynix-stake value trapped inside a regulated telco. The disclosed NAV-discount trajectory — 65.7% at end-2024, 51.5% at end-2025, 46.6% at the May 13 close — tracks the wider rerating of Korean holdcos under the value-up program.

Yonhap and Maeil Business separately reported that 14 single-stock leveraged ETFs and two inverse ETFs tracking Samsung Electronics and SK Hynix are scheduled to list on May 27 on the Korea Exchange (KRX, Korea's main bourse operator). The launch, a first for single Korean equities, channels more retail leverage into the two stocks now anchoring the top of the KOSPI.

What to Watch

- Whether SK Square's NAV discount continues to compress or stalls as the post-print rally cools.

- The May 27 KRX listing of single-stock leveraged ETFs on SK Hynix and Samsung Electronics, which Yonhap and Maeil Business say will intensify ETF fee competition and could amplify volatility in the two names anchoring SK Square's NAV.

- Any capital-allocation moves — additional buybacks beyond the ₩310 billion envelope, special dividends, or portfolio monetisation — that convert paper equity-method income into cash returns.

- SK Hynix Q2 results and HBM (high-bandwidth memory) pricing, which Etnews notes is the single largest swing factor for SK Square's reported earnings.

Sources: - Etnews — https://www.etnews.com/20260514000490 - Newspim — https://www.newspim.com/news/view/20260514001299 - Yonhap News — https://www.yna.co.kr/view/AKR20260514125200008 - Maeil Business Newspaper — https://www.mk.co.kr/news/stock/12047713 - SK hynix Newsroom (1Q26 results) — https://news.skhynix.com/q1-2026-business-results/ - PR Newswire (SK hynix 1Q26) — https://www.prnewswire.com/news-releases/sk-hynix-announces-1q26-financial-results-302750959.html - Seoul Economic Daily — https://en.sedaily.com/markets/2026/05/04/sk-hynix-market-cap-tops-1000-trillion-won-as-stock-surges

By LineVest Markets Desk — 2026-05-14This article is for informational purposes only and does not constitute investment advice.