Samsung Electro-Mechanics, LG Innotek Pivot From Apple Suppliers to AI Infrastructure Partners

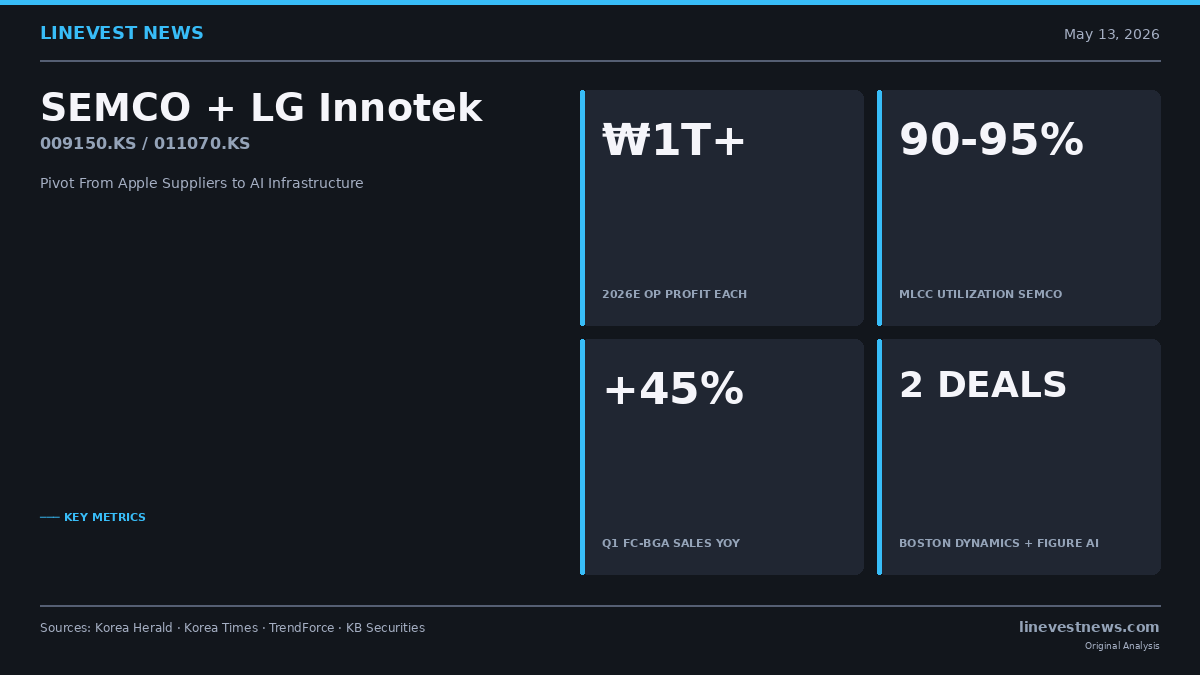

TL;DR - Brokerage models published this week have both Korean component majors crossing the ₩1 trillion ($730 million) operating-profit line in 2026, driven by AI-server substrates, high-end MLCCs, and humanoid-robot vision modules. - Samsung Electro-Mechanics' MLCC plants are running at 90–95% utilization, per Chosun Biz, while its Q1 FC-BGA sales jumped 45% year-on-year to ₩725 billion ($529 million). - The pivot reframes both names from cyclical Apple/Samsung Electronics suppliers into structural beneficiaries of the AI capex cycle — watch H2 MLCC pricing and Figure AI / Boston Dynamics ramp signals.

Lead — Two of Korea's largest electronic-component makers, Samsung Electro-Mechanics (Korea's leading multi-layer ceramic capacitor maker) and LG Innotek (Apple's main camera-module supplier), are on track for record 2026 results as their revenue mix tilts decisively toward AI servers and humanoid robotics, according to brokerage forecasts collated by Chosun Biz on May 14. The shift is changing how the Seoul sell-side frames both names — less "set-maker downstream cyclical," more "AI infrastructure partner."

What Happened

In a May 14 industry note, Daishin Securities (a mid-tier Korean brokerage) forecast Samsung Electro-Mechanics' 2026 operating profit at ₩1.143 trillion ($834 million), up 26.1% year-on-year, while Meritz Securities pegged LG Innotek's 2026 operating profit at ₩1.0849 trillion ($792 million), as reported by Chosun Biz. If realized, LG Innotek would re-enter Korea's so-called "₩1 trillion club" of operating profit for the first time since 2022, per the same report.

The forecasts sit on top of strong Q1 prints. Samsung Electro-Mechanics' Q1 2026 revenue was ₩3.21 trillion and operating profit ₩280.6 billion ($189 million), up 40% year-on-year, with the component (MLCC) division revenue at ₩1.41 trillion (up 16%) and the package solutions (FC-BGA) division at ₩725 billion (up 45%), according to The Korea Herald. LG Innotek's Q1 2026 revenue reached a record ₩5.53 trillion with operating profit of ₩295.3 billion ($201 million), more than doubling year-on-year; its substrate unit grew 16% to ₩437.1 billion ($319 million), per the same outlet.

Why It Matters

This is the first concrete signal that Korea's two flagship component houses are graduating from being earnings hostages of a single anchor customer to structural picks on the AI build-out. The thesis shift matters because both stocks have historically traded on iPhone unit cycles or Samsung Electronics' DRAM swings — discounted relative to global AI-substrate peers as a result. KB Securities Research Head Kim Dong-won, quoted by Chosun Biz, argued that LG Innotek is "significantly undervalued versus the average AI substrate peer" and that both names are likely to be "re-rated as core AI infrastructure partners, not simple component suppliers."

The inflection has three legs: AI-server FC-BGA going into structural undersupply, high-voltage industrial/automotive MLCCs taking a larger share of the mix, and a brand-new humanoid-robot vision/sensor product line that did not exist on the revenue line a year ago.

Business Impact

For Samsung Electro-Mechanics, Daishin Securities projects 2026 FC-BGA revenue of ₩1.43 trillion ($1.04 billion), up 25.5% year-on-year, with the company already running a new FC-BGA facility in Vietnam to absorb AI-accelerator and server-CPU demand, per Chosun Biz. MLCC utilization at 90–95% leaves little volume lever, so pricing becomes the swing factor; Japan's Murata (the global MLCC leader) has signaled price increases, which Chosun Biz reports could prompt Samsung Electro-Mechanics to follow. The company is also entering the glass-substrate market and is expected to begin substrate shipments to four new AI-server customers in H2 2026, according to Chosun Biz, with components for Tesla's humanoid-robot program — MLCCs, camera modules, and packaging substrates — flagged as a future revenue pillar by the same report.

For LG Innotek, Apple-bound camera modules historically accounted for roughly 80% of group revenue, per Chosun Biz. The package solutions unit's share of group operating profit rose from 10% in 2024 to 19.4% in 2025 and is expected to clear the low 20%s in 2026, with some Seoul analysts modeling close to 30% by 2027, again per Chosun Biz. CEO Moon Hyuk-soo has publicly stated a five-year goal of bringing substrate-segment profit to parity with optical solutions, a target Chosun Biz attributed to him in May. In a separate October 2025 initiation note, KB Securities analyst Jeff Kim projected LG Innotek's total AI-related business — spanning humanoid-robot cameras, autonomous-driving sensors, and AI semiconductor substrates — to grow from roughly ₩400 billion ($292 million) in 2025 to ₩7 trillion ($5.1 billion) by 2030, lifting AI's share of group revenue from about 2% to 22%, with humanoid-robot camera revenue alone projected to rise roughly tenfold year-on-year in 2026. LG Innotek's own May 12, 2025 press release confirms a partnership with Boston Dynamics to develop a vision-sensing system for the Atlas humanoid; trade press including TrendForce reported in June 2025 that LG Innotek had agreed to supply camera modules to U.S. humanoid startup Figure AI. Chosun Biz adds Tesla as a third humanoid customer, though that piece is not corroborated by the English-language press releases above.

Industry & Historical Context

LG Innotek last cleared ₩1 trillion in operating profit in 2022, when iPhone Pro camera-module loadings spiked; the subsequent two years saw the figure compress as Apple smartphone demand cooled. Samsung Electro-Mechanics' last comparable boom cycle was driven by smartphone-MLCC content growth in 2017–2018. What's different this time, on the evidence available, is that the demand pull is coming from AI accelerator packaging, hyperscaler server CPUs, and a nascent humanoid market — categories that did not move the needle in either prior cycle. Samsung Electro-Mechanics itself noted in Q1 earnings commentary that "demand is far exceeding production capacity" for both MLCCs and FC-BGAs, as cited by The Korea Times.

The macro backdrop also helps: US–China AI-supply-chain decoupling is steering hyperscaler substrate and sensor sourcing toward non-China Asian suppliers, a dynamic Chosun Biz flagged as a "reflexive benefit" for LG Innotek.

What to Watch

- Whether Samsung Electro-Mechanics formally announces MLCC price increases following Murata's signal, and whether those flow into H2 2026 numbers — per Chosun Biz, that is the single largest swing factor for the upgrade cycle.

- LG Innotek's quarterly disclosure of substrate-segment operating-profit share — the 20%+ 2026 target is the near-term milestone, the ~30% 2027 figure is the bull case.

- Volume disclosures around Figure AI and Boston Dynamics ramp; CES 2026 commentary from CEO Moon Hyuk-soo, reported by The Korea Times, already pegged humanoid-robot sensing revenue at "tens of billions of won."

- Samsung Electro-Mechanics' Vietnam FC-BGA plant ramp and the start of substrate shipments to the four new AI-server customers flagged for H2 2026.

Sources: - Chosun Biz — https://biz.chosun.com/it-science/ict/2026/05/14/AKZP4M6MMRGETALCVUIAV6FRQM/ - The Korea Herald (Samsung Electro-Mechanics Q1 2026) — https://www.koreaherald.com/article/10729376 - The Korea Herald (LG Innotek Q1 2026) — https://www.koreaherald.com/article/10726451 - The Korea Times (electronic parts firms AI supercycle outlook) — https://www.koreatimes.co.kr/business/tech-science/20260504/electronic-parts-firms-enjoy-rosy-outlook-on-ai-supercycle - The Korea Times (LG Innotek humanoid robots) — https://www.koreatimes.co.kr/business/tech-science/20260210/lg-innotek-accelerates-camera-sensor-biz-for-humanoid-robots - LG Innotek–Boston Dynamics press release (May 12, 2025) — https://www.prnewswire.com/news-releases/lg-innotek-and-boston-dynamics-to-create-the-next-generation-robot-vision-system-302452249.html - TrendForce (LG Innotek–Figure AI camera-module supply, June 2025) — https://www.trendforce.com/news/2025/06/19/news-lg-innotek-reportedly-deepens-robotics-push-with-camera-module-supply-to-figure-ai/ - KB Securities (LG Innotek initiation, October 2025, analyst Jeff Kim) — https://en.kbsec.com/go.able?linkcd=m0401006&sDocumentid=20251028193104140E&sUrlLink=aHR0cHM6Ly9yZGF0YS5rYnNlYy5jb20vcGRmX2RhdGEvMjAyNTEwMjgxOTMxMDQxNDBFLnBkZg%3D%3D

By LineVest Markets Desk — May 13, 2026This article is for informational purposes only and does not constitute investment advice.