Why Apple's balance sheet looks nothing like what you'd expect from a $4 trillion company

Why This Series Exists

In our last series, we read income statements line by line. By the end, you could look at the four key lines of any company's income statement and tell a story. But there are questions an income statement just can't answer:

- How much wealth has this company accumulated?

- How much debt is it carrying?

- Is there any near-term solvency risk?

- Cumulatively, how much belongs to shareholders?

These questions live on the Balance Sheet — the second of the three core financial statements. And today, we're going to read it through one of the most famous (and quietly weirdest) balance sheets in the world: Apple's.

A quick note for first-time readers of US filings: Apple uses a fiscal year ending in late September. The data we'll be looking at — "FY2025" — actually covers October 2024 through September 27, 2025. So it's offset from a Korean company's calendar year by about nine months. Worth keeping in mind for cross-border comparisons.

1. The Balance Sheet Is a "Photo," Not a "Movie"

Here's the analogy that unlocks everything.

Income Statement = a movie (records what happened over a year) Balance Sheet = a photograph (captures the company at a single moment in time)

An income statement covers a span — "from October 1, 2024 to September 27, 2025." Money flowed in. Money flowed out. Profit emerged. It's footage.

A balance sheet, by contrast, says: "On September 27, 2025, here is exactly what Apple looked like." That much cash in the bank. That much debt outstanding. That many factories, that many warehouses, that much inventory. It's a snapshot.

Why does this distinction matter? An income statement tells you whether the harvest was good. A balance sheet tells you how much grain is sitting in the silo. You need both views to understand a company.

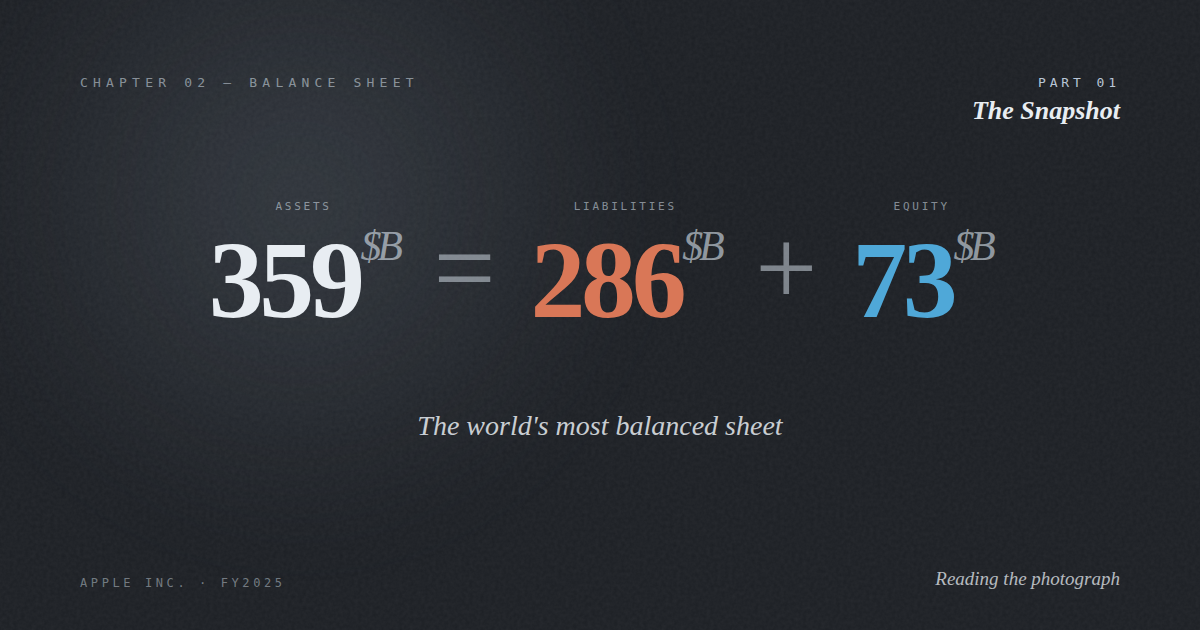

2. The Balance Sheet's Master Equation

The first thing you encounter when you open any balance sheet is one equation. It's the most important line in all of accounting:

Assets = Liabilities + Equity

In plain English: "Everything the company owns (assets) was paid for either with someone else's money (liabilities) or with the owners' money (equity)."

Imagine you bought a $500,000 house. $300,000 came from a mortgage; $200,000 came out of your savings. Your personal balance sheet looks like this:

| What I Own (Assets) | Whose Money It Is (Liabilities + Equity) |

|---|---|

| House $500,000 | Mortgage $300,000 (Liability) |

| My Money $200,000 (Equity) | |

| Total $500,000 | Total $500,000 |

A simple personal balance sheet

The left side and right side always equal each other. That's where the name comes from — the sheet must "balance."

Apple is no different. On September 27, 2025, Apple held $359B in assets. Of that, $286B was owed to creditors and $73B belonged to shareholders. The two sides add up perfectly.

By the way, that shareholder figure ($73B) is also called "book value" — it's what you'd theoretically get if Apple liquidated everything at carrying values. Book value is the denominator in the Price-to-Book (P/B) ratio.

3. Two Big Splits: Current vs Non-Current

Beyond the three-part split (Assets / Liabilities / Equity), both the asset and liability sides split again — this time by time horizon.

Assets → Current vs Non-Current

- Current Assets: Will turn into cash within 12 months. Cash, receivables, inventory.

- Non-Current Assets: Held for longer than 12 months. Buildings, equipment, patents, goodwill.

Liabilities → Current vs Non-Current

- Current Liabilities: Must be paid off within 12 months. Trade payables, short-term debt.

- Non-Current Liabilities: Due beyond 12 months. Long-term bonds, notes.

Why the 12-month line? Because solvency hinges on it. A company stays alive as long as the cash it can raise quickly exceeds the bills coming due quickly. That 12-month window is the analytical knife that lets us measure short-term solvency at a glance.

Current Assets ÷ Current Liabilities = Current Ratio If this is below 1.0, the company has more bills coming due than cash to pay them. 1.5 to 2.0 is generally considered safe — though norms vary by industry.

4. Apple's FY2025 Balance Sheet — At a Glance

Here's the actual balance sheet from Apple's FY2025 10-K, the same document you'd pull off SEC EDGAR. We're going to spend the next four parts unpacking what's inside:

| Category | FY2025 ($B) | FY2024 ($B) |

|---|---|---|

| Assets | ||

| Current assets | 148.0 | 153.0 |

| Non-current assets | 211.3 | 212.0 |

| Total assets | 359.2 | 365.0 |

| Liabilities | ||

| Current liabilities | 165.6 | 176.4 |

| Non-current liabilities | 119.9 | 131.6 |

| Total liabilities | 285.5 | 308.0 |

| Equity | ||

| Total shareholders' equity | 73.7 | 57.0 |

| Liabilities + Equity | 359.2 | 365.0 |

Source: Apple Inc. 10-K, FY2025 (as of September 27, 2025; in billions of USD)

Three things should jump out immediately. Let's walk through each.

Observation 1: Total assets shrank in a year

From FY2024 to FY2025, Apple's total assets dropped from $365B to $359B — about $6B less. That's strange. Companies that are growing should usually have growing balance sheets. Something is offsetting that growth.

This is Apple's first big mystery. The answer is share buybacks. Apple is spending massive amounts of cash every year buying back its own stock and retiring it. We'll devote Part 5 to this story.

Observation 2: Equity is only 20% of assets

$73.7B equity ÷ $359.2B total assets = about 20.5%. Flip it: liabilities are roughly 80% of the asset base. For most companies, an 80% debt-to-assets ratio is a red flag. Apple, though? One of the most financially solid companies on earth. The contradiction is intentional — Apple has engineered this structure on purpose. Part 5 again.

Observation 3: Equity grew sharply this year

Even as assets shrank, equity grew from $57B to $73.7B — about $17B added. That signals "slightly fewer buybacks, more retained earnings" — and shows how the income statement's $112B in net income flowed back into the balance sheet.

5. Drilling Into Current Assets

Now we go inside. What does Apple's $148B in current assets actually consist of?

| Item | FY2025 ($B) | Share |

|---|---|---|

| Cash and cash equivalents | 35.9 | 24% |

| Marketable securities (short-term) | 18.8 | 13% |

| Accounts receivable | 39.8 | 27% |

| Vendor non-trade receivables | 33.2 | 22% |

| Inventories | 5.7 | 4% |

| Other current assets | 14.6 | 10% |

| Total current assets | 148.0 | 100% |

Source: Apple 10-K (in billions of USD)

Three quick observations from this single table.

Observation A: An enormous cash position

Cash $35.9B + Short-term marketable securities $18.8B = $54.7B. That's how much Apple could put on the table tomorrow morning. And remarkably, this is the smaller version of Apple's cash hoard.

A few years ago, between short-term and long-term marketable securities, Apple held over $250B. Where did the rest go? Buybacks again — that's Part 5 territory.

Observation B: Inventory is shockingly small

Apple's inventory: $5.7B. To grasp how small that is, look at the comparison:

| Company | Inventory ($B) | Revenue ($B) | Inv. / Rev. |

|---|---|---|---|

| Apple | 5.7 | 391 | 1.5% |

| Samsung Electronics | ~51 | ~243 | ~21% |

| Walmart (for context) | ~56 | ~681 | ~8% |

Inventory-to-revenue comparison (approximate)

Apple holds inventory equal to just 1.5% of revenue. That's about one-fourteenth of Samsung's ratio (21%) and one-fifth of Walmart's (8%). This is the legacy of Tim Cook, who joined Apple in 1998 and rebuilt its supply chain into something close to a "zero inventory" operation: components arrive, they're assembled almost immediately, and finished products ship out. We'll dig into the mechanics in Part 2.

Observation C: "Vendor non-trade receivables" — $33B of what?

This line is rare in non-Apple balance sheets. It's money Apple's component suppliers are holding inventory for, on Apple's behalf. Apple says, in effect, "go buy and stock these chips, screens, and parts. We'll pay for them when we take delivery."

So the suppliers tie up their own working capital sitting on those parts. Apple, meanwhile, runs almost inventory-free. This entry on the balance sheet is one quiet reflection of Apple's negotiating power over its supply chain.

6. Non-Current Assets — Held Beyond a Year

| Item | FY2025 ($B) | Share |

|---|---|---|

| Marketable securities (long-term) | 77.7 | 37% |

| Property, plant and equipment, net | 49.8 | 24% |

| Other non-current assets | 83.7 | 40% |

| Total non-current assets | 211.3 | 100% |

Apple's non-current assets, FY2025

Another stunner here. Apple's PP&E is $49.8B — about ₩70 trillion in Korean won terms. That's the total carrying value of every Apple Store, every data center, every office, every piece of internal-use software. Samsung Electronics, for comparison, carries roughly ₩200 trillion of PP&E — nearly 3× Apple's.

Now consider that Apple's revenue is 1.6× larger than Samsung's. Yet Samsung has 3× the fixed assets. PP&E per dollar of revenue:

- Apple: $50B / $391B = about 13%

- Samsung: ~$146B / $243B = about 60%

Apple is, structurally, a manufacturer with almost no factories of its own. It outsources production to contract manufacturers — Foxconn, Pegatron, Luxshare, mostly in China and Vietnam. Samsung, by contrast, must own its memory fabs to compete. The same "IT manufacturing" sector hides two completely different business models. That contrast lives on the balance sheet.

What's in "other non-current assets" ($83.7B)? Per the footnotes: deferred tax assets ($20.8B), Apple Store lease right-of-use assets, intangibles, and goodwill. Goodwill is the premium Apple paid above net book value when acquiring other companies. Notably, Apple's goodwill is small — Apple tends to do small technology tuck-ins, not big M&A.

7. What We Found in Part 1

Closing out Part 1, here's the takeaway:

- The balance sheet is a snapshot — the assets, liabilities, and equity at a single moment

- The master equation: Assets = Liabilities + Equity (always balances)

- The 12-month line divides current and non-current

- Apple's $359B asset base looks rich in cash but only 20% is shareholder equity

- Apple is a manufacturer without factories — PP&E is just 13% of revenue

- 1.5% inventory-to-revenue — the SCM marvel that Tim Cook built

Coming in Part 2

Part 1 was the forest. Part 2 zooms into the trees of the current assets section:

- Cash isn't always "cash" — what hides inside Apple's $35.9B

- The mechanics of Apple's $5.7B inventory — how Tim Cook actually runs the supply chain

- $40B in receivables — and the accounting estimate Apple makes about uncollectibles

- Vendor non-trade receivables, demystified — Apple's most unusual balance-sheet entry

The deeper you go into a balance sheet, the more the company you thought you knew starts to look like something else entirely.

Frequently Asked Questions

What's the difference between a balance sheet and an income statement?

An income statement reports flows over a period (typically a quarter or a year): revenue, costs, profit. A balance sheet shows the company's position at a single point in time: what it owns, what it owes, and the residual value belonging to shareholders. Both are needed for a complete picture.

Why does Apple's fiscal year end in September?

Companies in the US can choose any fiscal year-end. Apple's late-September close lines up neatly after the fall iPhone launch, when older-model inventory has been cleared and the new product cycle begins fresh. It produces cleaner accounting at year-end. Most Korean companies, by contrast, use a December fiscal year-end.

Is Apple's 80% liabilities-to-assets ratio dangerous?

In isolation, it would be a red flag for most companies. For Apple, it isn't — for two reasons. First, the "liabilities" include large operational items like deferred revenue and accounts payable that aren't true financing debt. Second, Apple has deliberately reduced equity through massive share buybacks. We unpack both points in later parts.

What is book value, and why does it matter for valuation?

Book value is total shareholders' equity. It represents what would theoretically belong to common shareholders if the company were liquidated at carrying values. Investors compare it to market capitalization to compute the Price-to-Book (P/B) ratio, a classic valuation metric — particularly useful for asset-heavy businesses like banks and industrials.

Next: Part 2 — Reading Current Assets: Cash, Receivables, and the Apple Inventory Mystery.